Implementing effective transfer pricing strategies is essential for regulatory compliance and optimizing your tax position in the U.S.

Transfer pricing helps intercompany transactions align with the arm’s length principle, preventing double taxation and mitigating tax risks.

Meticulous documentation and regularly updated policies are key to maintaining compliance with transfer pricing regulations.

~

As a multinational enterprise setting up operations in the United States, it is imperative for you to understand the complexities of transfer pricing and intercompany transactions. Effective transfer pricing strategies will help you meet regulatory compliance and improve your tax position.

Fundamentals of Transfer Pricing

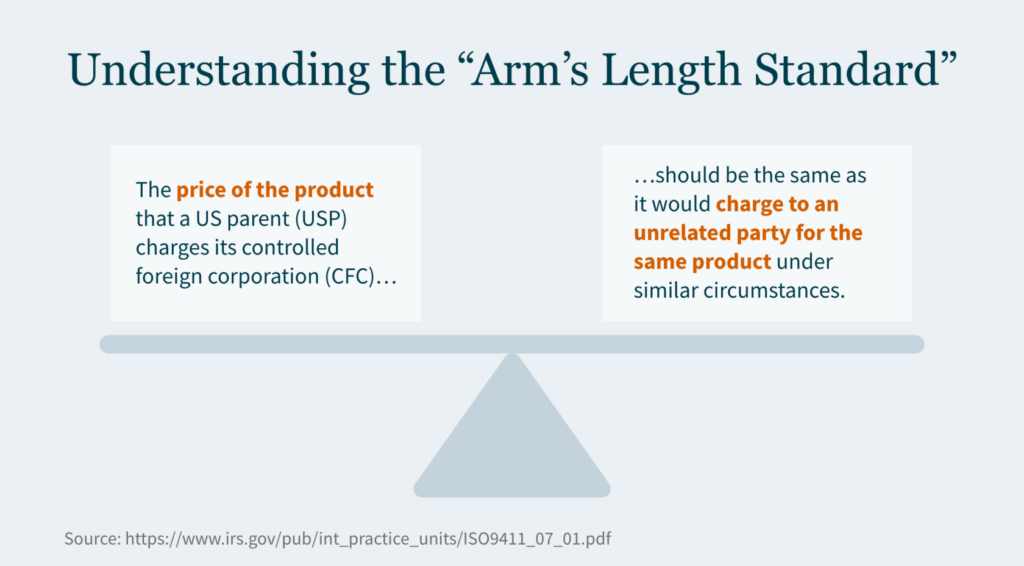

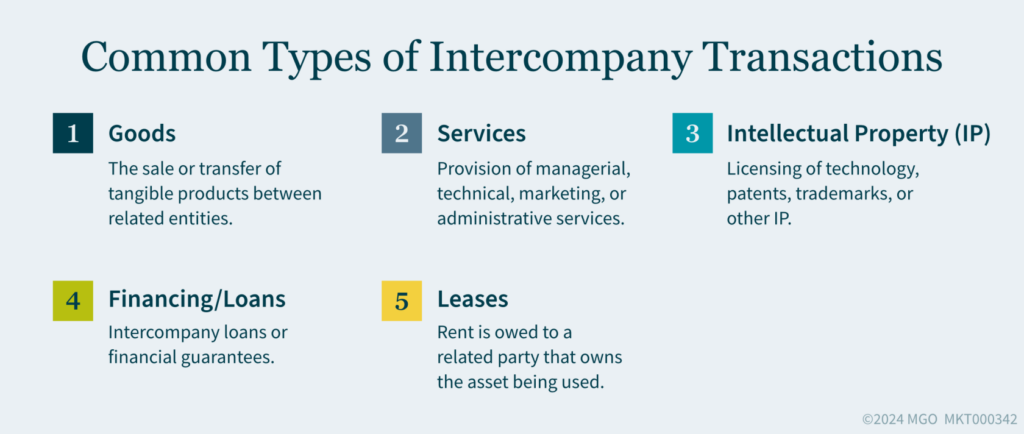

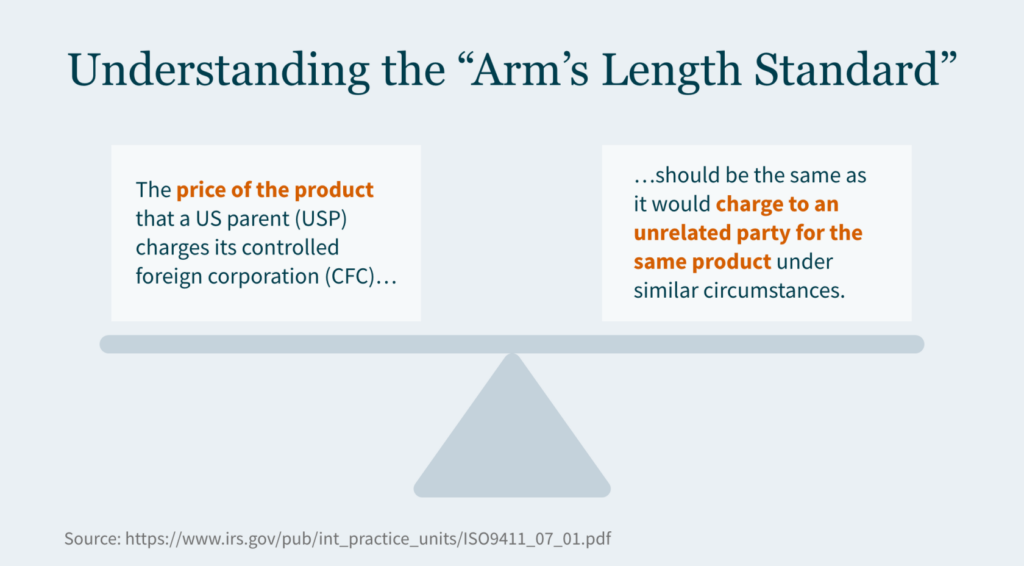

Transfer pricing involves setting prices between related entities for transactions — such as the purchase or sale of goods, provision of services, performance of manufacturing activities, cost allocation, or use of intellectual property. This practice of “negotiating” prices between related entities ensures transactions are conducted at “arm’s length”, meaning the prices are consistent with those charged between independent parties. Proper transfer pricing can help you avoid double taxation, mitigate tax risks, and follow U.S. laws.

It is important to note that “related entities” for these purposes involve the concepts of both common ownership and common control. Many taxpayers who fail to understand these concepts also fail to properly address transfer pricing rules and regulations for various transactions.

Regulatory Requirements

IRS Guidelines on Transfer Pricing

The Internal Revenue Service (IRS) provides detailed guidelines on transfer pricing to promote fair pricing practices. These guidelines require businesses to apply the arm’s length principle and provide adequate documentation to justify pricing methods.

Documentation and Compliance

Compliance with U.S. transfer pricing regulations involves meticulous documentation. Companies must prepare and keep detailed records of intercompany transactions — including the rationale for pricing decisions, application of the best method, and evidence that prices meet arm’s length standards. Non-compliance can lead to substantial penalties and adjustments imposed by the IRS.

Setting Up Transfer Pricing Policies

Establishing effective transfer pricing policies requires a thorough understanding of the business model, industry standards, and regulatory requirements. Your company should develop policies that align with the arm’s length principle and keep consistency across all intercompany transactions. Additionally, you should continuously check and update these policies to adapt to any changes in business operations and tax regulations.

Examining real-world examples can offer valuable insights into effective transfer pricing strategies.

Example 1: Goods Transfer

A multinational company based in the United Kingdom sets up a U.S. subsidiary to handle distribution. To follow transfer pricing regulations, the company conducts a thorough analysis to decide proper prices for goods transferred to the U.S. entity, verifying the profitability of the U.S. entity is appropriate.

Example 2: Service Provision

A Japanese company provides technical support services to its U.S. subsidiary. By documenting the cost-plus method, where a markup is added to the costs incurred in providing the services, the company shows compliance with the arm’s length principle.

Example 3: Intellectual Property Licensing

A German firm licenses its proprietary software to a U.S. branch. The firm conducts a detailed analysis to decide the right royalty rate, confirming the transaction meets IRS guidelines and minimizes tax liabilities.

Optimizing Your Transfer Pricing Approach

For multinational businesses moving into the U.S. market, it is vital to understand and implement effective transfer pricing strategies to assist with regulatory compliance, improve tax positions, and support seamless intercompany transactions.

Even if your business is familiar with Organization for Economic Co-operation and Development (OECD) transfer pricing guidelines or currently operates in a country that mirrors them, you need to know the subtleties that may occur should the IRS review your related-party transactions. The IRS will generally abide by U.S. transfer pricing principles without consideration of OECD guidelines. Understanding the differences may help you avoid headaches and create a consistent approach throughout your organization worldwide.

If your business is navigating the complexities of transfer pricing, professional advice and tailored strategies are recommended. For detailed guidance and personalized support, reach out to our International Tax team today.

Setting up a business in the U.S. requires thorough planning and an understanding of various regulatory and operational challenges. This series will delve into specific aspects of this process, providing detailed guidance and practical tips. Our next article will discuss operational strategies for a successful expansion.

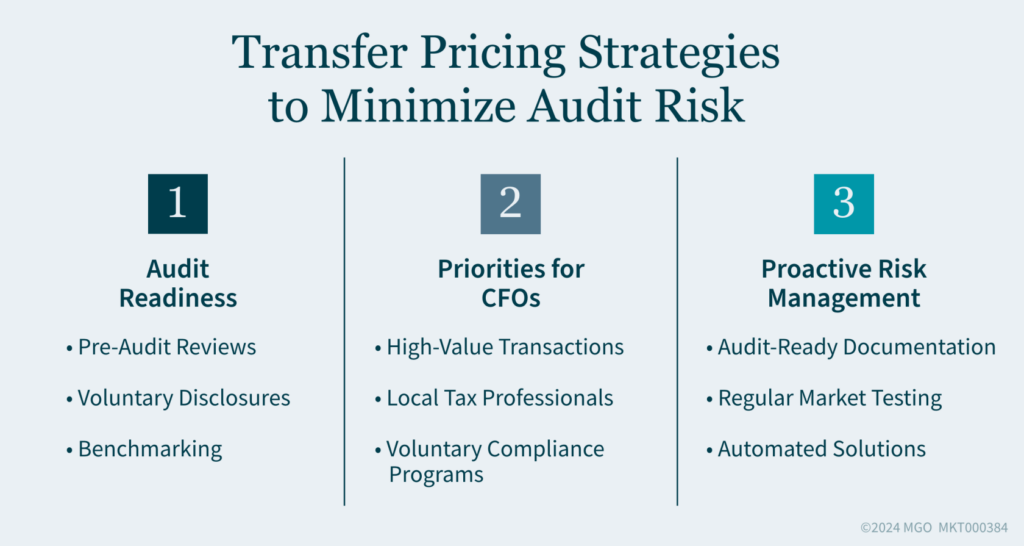

Transfer pricing is an increasing area of focus for tax authorities, requiring CFOs to adopt more strategic audit preparation.

Proactive measures like pre-audit reviews, voluntary disclosures, and benchmarking are crucial for companies to defend transfer pricing policies and minimize risks.

Prioritizing high-value transactions, collaborating with tax professionals, and leveraging technology are essential to stay ahead of evolving transfer pricing regulations and potential audits.

~

In today’s global tax environment, transfer pricing has become a critical focus for tax authorities. With multinational companies operating across multiple jurisdictions, tax authorities are intensifying their efforts to scrutinize transfer pricing practices and confirm that profits are appropriately distributed and taxed in their jurisdictions. This growing focus requires chief financial officers (CFOs) and tax executives to shift from compliance alone to comprehensive audit preparation and strategic risk management.

From Compliance to Audit Readiness

While transfer pricing compliance has always been important, the increasing focus on audit enforcement is changing the landscape. It is no longer enough to simply have policies in place; your company needs to be prepared to defend them under rigorous examination. This shift highlights the importance of proactively managing transfer pricing risk and preparing for potential audits.

Risk management and audit preparation efforts include:

Pre-audit reviews — Conducting periodic pre-audit reviews is essential. These reviews offer an opportunity to examine your transfer pricing documentation and policies to confirm the pricing of all intercompany transactions is supported by clear agreements. It is important the documentation reflects an arm’s length standard and is presented in a way that would stand up to an audit. Showing gaps, inconsistencies, or potential weaknesses early on allows your company to address them before tax authorities intervene.

Voluntary disclosures — In cases where pre-audit reviews reveal potential issues, voluntary disclosures can be a valuable tool. If discrepancies are found, making voluntary disclosures to tax authorities can sometimes lead to more favorable outcomes as it shows good faith and a proactive approach to compliance. It also demonstrates your company has a level of sophistication in overall global financial hygiene. This strategy can help you avoid more severe penalties that may arise from issues discovered during an Internal Revenue Service (IRS) or foreign jurisdiction audit.

Benchmarking — Benchmarking and testing are also key components of audit preparedness. Your company should consistently review its transfer pricing policies and test them against current market conditions. This is particularly important when there are economic shifts or significant changes in business operations — such as the introduction of new products, services, or intangible assets. By regularly benchmarking intercompany pricing, your company can support alignment with the arm’s length principle and minimize risk during an audit.

The Role of CFOs in Managing Transfer Pricing Risk

For CFOs, transfer pricing audits are a significant financial risk. These audits can result in tax adjustments and penalties. They can also lead to reputational damage if issues are not handled properly and with sufficient expeditiousness. CFOs together with their tax advisors play a significant role in mitigating this risk by taking a strategic approach to audit readiness and documentation.

Key areas of focus for CFOs include:

High-value transactions — A top priority for CFOs should be focusing on high-value transactions. Not all intercompany transactions carry the same level of risk, and those involving intangible assets, intellectual property, or complex financial arrangements tend to receive the most scrutiny from tax authorities. It is important to thoroughly document and benchmark these transactions to avoid potential challenges during an audit.

Tax professionals — Another critical element of risk management is collaborating with tax professionals. Transfer pricing rules can vary significantly across jurisdictions, and tax advisors are well-versed in the specific requirements and regulations in various countries. Working closely with these advisors enables your company to adapt its transfer pricing policies to standards and minimize exposure to risk.

Voluntary compliance programs — In some cases, companies may receive help by entering voluntary compliance programs — such as advance pricing agreements (APAs). These agreements allow your company to gain certainty over transfer pricing arrangements by agreeing to terms with tax authorities in advance. For high-risk transactions or operations in high-risk jurisdictions, APAs can provide a level of protection from future audits and disputes.

Proactive Risk Management in Transfer Pricing

The global tax landscape continues to evolve as regulatory authorities refine their approaches to transfer pricing audits and enforcement. For mid-market companies with limited resources, it is particularly important to strike the right balance between compliance and cost-efficiency. This requires a proactive approach to transfer pricing risk management that combines audit readiness with strategic planning.

Steps for proactive risk management include:

Audit-ready documentation — The first step in proactive risk management is building audit-ready documentation. This includes keeping detailed records of all intercompany transactions, agreements, and financial data that support the arm’s length nature of pricing decisions. Regularly reviewing and updating this documentation helps your company stay prepared for potential audits.

Regular market testing — Beyond documentation, CFOs should incorporate benchmarking and market testing into risk management strategies. By continuously checking how your pricing compares to the market, your company can stay aligned with the arm’s length principle and minimize exposure to tax adjustments. Regular testing can also help you find potential discrepancies before they become audit issues.

Automated solutions — Finally, using technology to enhance efficiency and accuracy in transfer pricing documentation and analysis is essential. Automated solutions and data analytics offer the ability to quickly find risks, prioritize compliance efforts, and streamline the process of audit preparation.

Keeping Your Company Ahead of the Transfer Pricing Curve

In an era of increased scrutiny and regulatory pressure, transfer pricing compliance is a priority for multinational companies. For CFOs and tax executives, the challenge lies not just in keeping compliant but in preparing for audits and managing the associated risks. Proactive risk management, strategic audit readiness, and a careful focus on high-value transactions are critical components in navigating this complex landscape.

By focusing on audit preparedness, keeping documentation up-to-date, and collaborating with local tax professionals, you can position your company to minimize tax adjustments, penalties, and disputes. As transfer pricing rules continue to evolve, staying ahead of the curve with a forward-thinking strategy is essential for supporting compliance and reducing financial risks.

How MGO Can Help

Our International Tax team is here to help you navigate the new transfer pricing landscape. We can assist you in both broad and focused areas, providing guidance to meet your specific transfer pricing needs. Our services include:

IRS Pre CheckUP — We help you identify and rectify potential weaknesses in transfer pricing and international tax documentation and practices before facing an actual IRS audit.

Review of:

Cross-border agreements for U.S. tax updates

Benchmark data sets

Transfer pricing documentation

U.S. tax returns to confirm consistency with transfer pricing documentation and policies, as well as withholding practices

This article is part of an ongoing series, “Navigating the Complexities of Setting Up a Business in the USA”.

Key Takeaways:

Expand into the U.S. market to access a large and diverse customer base.

Navigate the multi-layered U.S. tax system and adapt to cultural differences.

Choose the right business entity and plan for compliance with U.S. regulations.

~

Expanding your business into the United States can significantly increase your market share and open the door to new opportunities. However, the process involves navigating a complex landscape of regulations, tax considerations, and operational challenges. This series provides an overview to help you understand how to successfully set up your business in the U.S.

Why Expand to the U.S.?

Expanding into the U.S. market allows you to:

Access a large and diverse customer base.

Leverage the economic scale of the U.S. market.

Explore opportunities for growth and innovation that may not be available in other countries.

Have access to what may be a significant amount of capital (whether this may be equity or debt or other arrangements).

Moving into the U.S. market can help you drive more sales and reach new types of customers. You may also launch new products here that might not succeed in your home market.

5 Key Considerations for Foreign Businesses

When setting up a business in the U.S., you must navigate a range of unique challenges — including:

1. Multi-Layered Tax System

In many countries, businesses deal with a single national tax system where their provinces or states mimic or have congruent rules with federal rules. In contrast, the U.S. has a multi-layered tax system involving federal, state, and local taxes that at many times are not congruent.

When you start a business in the United States you are dealing with 50 states (and the District of Columbia), multiple localities, and certain territories. Each state has its own set of rules and regulations applicable to income taxes, which can be quite different from a single national system (and often at odds with the federal rules).

In addition, state and local jurisdictions impose taxes unique to the state and local level — including sales tax, property tax, and gross receipt tax. Finally, not all states honor the provisions of U.S. tax treaties with foreign countries.

2. Cultural and Business Practice Differences

Understanding and adapting to cultural and business practice differences is crucial. For instance, business practices that are common in Europe or Asia might not be as effective in the U.S. Additionally, legal agreements and formalities that might be less stringent abroad are often necessary in the U.S. to protect business interests.

3. Legal Structure and Entity Choice

Choosing the right business entity is vital as it affects tax obligations, legal liability, and operational flexibility. Options include C corporations (or C corps), limited liability companies (LLCs), foreign corporations with or without U.S. branches, partnerships or joint ventures, or franchising or direct importing. An S corporation (S corp) is not an option for foreign businesses due to ownership restrictions.

Each structure has its own set of advantages and legal implications, which should be carefully considered.

4. Regulatory Compliance

The Corporate Transparency Act is one newly created obligation for all businesses operating in the U.S. Failure to comply can result in significant penalties. It is important to understand the reporting requirements and file all necessary documentation on time.

In addition, you should consult a lawyer to ensure the entity form is respected — including prompt organizational filings with the Secretary of State and obtaining necessary business licenses.

These are just a few of the myriad of regulations your business must navigate. That’s why it’s critical to hire the right professionals to build your team, as missing any of these requirements may place your business in peril.

5. Operational Challenges

Operational planning is essential for a successful U.S. expansion. Key operational considerations include:

Employee benefits and regulations: U.S. regulations on health insurance, retirement plans, and other employee benefits can be significantly different from those in other countries. For example, in Europe, many employee benefits are government-run, while in the U.S., they are often the responsibility of the employer.

Logistics and supply chain management: Choosing the right location for operations includes considerations such as proximity to logistics centers and understanding regional operational costs.

Insurance and banking: Obtaining necessary insurance coverage and opening bank accounts can be challenging for foreign businesses. Some U.S. banks may not provide accounts to foreign-owned companies, and those that do might have stringent requirements. Certain banks may refuse to conduct business with certain entities in industries such as cannabis and cryptocurrency, to name a couple.

Establishing a U.S. Presence for Your Business

Setting up a business in the U.S. requires thorough planning and an understanding of various regulatory and operational challenges. From navigating the multi-layered tax system to selecting the right business entity and following U.S. regulations, each step is crucial for a successful expansion. By addressing these key considerations and seeking professional guidance, you can effectively establish your presence in the U.S. market.

For more detailed insights and personalized help, connect with our International Tax team and start your journey towards successful U.S. market entry today.

Setting up a business in the U.S., requires thorough planning and an understanding of various regulatory and operational challenges. This series will delve into various aspects of this process, providing guidance and practical tips. Our next article will discuss navi

Businesses operating internationally should regularly review transfer pricing practices — including documentation, benchmarking, and IRS reporting requirements.

Understanding the classification of inter-company transactions, learning from past audits, and considering Advance Pricing Agreements can improve tax compliance and strategy.

Regular assessment of transfer pricing practices can help maintain compliance, mitigate risks, and potentially reveal cost-saving opportunities.

~

For today’s global businesses, understanding and managing the complexities of international tax and transfer pricing can be a challenge. That’s why it is important to regularly review your practices against critical standards to maintain compliance and improve tax strategies.

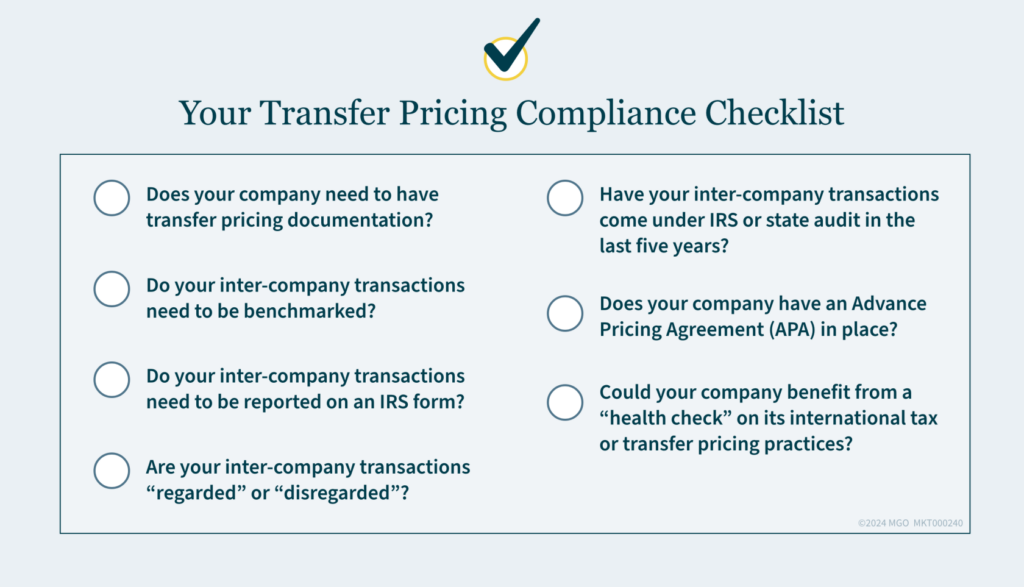

To help you determine if your company is compliant or if consultation may be needed, use this straightforward checklist based on key questions about your operations:

Does your company need transfer pricing documentation? Transfer pricing documentation is essential to show your company’s pricing policies follow local and international arm’s length standards. This documentation should include detailed analyses of inter-company transactions, the methods used to set prices, and how these follow applicable tax laws. Having robust documentation can help you prevent disputes with tax authorities, avoid potential tax penalties, and make audits run smoother.

Do your inter-company transactions need to be benchmarked? Benchmarking is the process of comparing your inter-company transactions with those of similar transactions by unrelated parties to confirm the inter-company pricing is at arm’s length. This process involves gathering data from uncontrolled comparable companies and transactions to justify your pricing strategies. Effective benchmarking helps maintain compliance and supports your transfer pricing documentation.

Do your inter-company transactions need to be reported on an IRS form? Certain inter-company transactions must be reported to the IRS to follow regulations and avoid penalties. For instance, transactions with foreign affiliates often require filling out Form 5472. Regularly reviewing which forms are applicable and accurately reporting transactions can help you stay compliant and avoid fines. In addition, your company may have offshore investments that may require reporting on IRS Forms 5471 and/or 8621.

Are your inter-company transactions “regarded” or “disregarded”? (Consider if some are regarded and others are disregarded.) The tax treatment of inter-company transactions can vary, with some being regarded and others disregarded. Understanding which transactions fall into each category is vital for proper tax planning and compliance as it affects income allocations and taxable earnings calculations.

Have your inter-company transactions come under IRS or state audit in the last five years? If your transactions have been audited, it’s important to review the outcomes and learn from them. An audit history can show potential areas of risk in your transfer pricing practices. Reviewing and adjusting practices based on past audits can help reduce the likelihood of future audits and potential penalties.

Does your company have an Advance Pricing Agreement (APA) in place? An APA is an agreement between a taxpayer and tax authorities that pre-approves transfer pricing methods the taxpayer will apply for future inter-company transactions. Having an APA can reduce uncertainty in tax matters, prevent disputes, and provide clarity on how transactions will be treated. If you don’t have an APA, it might be time to consider whether it could help your operations.

Could your company benefit from a “health check” on its international tax or transfer pricing practices? A tax “health check” involves a comprehensive review of your company’s tax and transfer pricing practices to find areas for improvement and potential risks. This proactive approach can help your company improve its tax strategies, verify compliance, and potentially uncover cost-saving opportunities.

Is Your Business Meeting Transfer Pricing Compliance Standards?

By answering the questions above, you can identify areas where your company may need to improve its transfer pricing and international tax practices. Addressing these key areas will help you develop more effective strategies to mitigate your risks.

How MGO Can Help

We are committed to helping you navigate the complex world of international tax and transfer pricing. With our comprehensive approach, we address each area of potential concern — from correct documentation and effective benchmarking to navigating IRS reporting requirements and understanding the tax implications of every transaction.

Whether you are looking to set up an APA or simply need a thorough “health check” of your current practices, our team is here to provide the support and insights necessary to improve your tax strategies and enhance your operational efficiency. Reach out to our team today.

The Amount B framework aims to simplify the arm’s length principle for pricing marketing and distribution activities, applicable to all taxpayers.

On June 17, 2024, supplementary guidance was released to finalize the administrative aspects of Amount B.

“Covered jurisdictions” are low-and middle-income countries, including some OECD and G20 members like Argentina and Mexico; “qualifying jurisdictions” are determined by income level and credit rating and have fewer than five local comparables.

~

Background

The Amount B framework for pricing baseline marketing and distribution activities is a new approach that seeks to streamline and simplify the application of the arm’s length principle. This approach applies to all taxpayers regardless of size and profitability. A report on Amount B was approved and published by the Inclusive Framework on February 19, 2024, and incorporated as an annex to Chapter IV of the Organisation for Economic Co-operation and Development (OECD) Transfer Pricing Guidelines.

The February 2024 report was published pending completion of work on some outstanding administrative aspects of the guidance. The supplementary guidance released on June 17 completes the work on those sections of the report. It consists of two documents, one of which defines and identifies “covered jurisdictions” within the scope of the political commitment regarding Amount B. These jurisdictions are those for which jurisdictions have agreed that an Amount B determination of returns in a covered distribution transaction will be respected regardless of whether the counterparty to the transaction has adopted Amount B.

A separate document addresses the definition and listing of jurisdictions determined to be “qualifying jurisdictions.” Qualifying jurisdictions are identified for two purposes: (1) a checking mechanism on the profit determined through the primary Amount B mechanism (Section 5.2 of the Amount B report), and (2) an adjustment to the profit determined through the primary Amount B mechanism for distributors in jurisdictions in which the global dataset of distributors does not provide sufficient coverage (Section 5.3 of the Amount B report).

Covered Jurisdictions

Under the agreement reached by the Inclusive Framework, jurisdictions can choose to apply the simplified and streamlined approach to the qualifying transactions of their in-scope tested parties; however, the outcome determined under that approach by a jurisdiction that has chosen to apply it would not be binding on the counterparty jurisdiction if that counterparty has not adopted the approach. To address this, members of the Inclusive Framework committed to respect the outcome determined under the simplified and streamlined approach when the approach is applied by what was initially called a “low-capacity jurisdiction.”

The Inclusive Framework originally said it would agree on the list of low-capacity jurisdictions by March 31, 2024; however, that deadline was not met. The first supplementary guidance document released on June 17 now addresses this. The term “low-capacity jurisdiction” has been replaced by “covered jurisdiction,” and includes certain low- and middle-income OECD and G-20 members.

The definition of covered jurisdictions is as follows:

Low- and middle-income Inclusive Framework jurisdictions as determined using the World Bank Group country classifications by income level, excluding EU, OECD, and G20 member countries.

Inclusive Framework jurisdictions that are OECD and G20 member states that otherwise meet the World Bank Group country determination as low- and middle-income, and that have expressed to the Inclusive Framework a willingness to apply Amount B. Argentina, Brazil, Costa Rica, Mexico, and South Africa fall in this category.

Any non-Inclusive Framework jurisdiction that meets the first criterion and expresses to the Inclusive Framework a willingness to apply Amount B will be added to the list of covered jurisdictions.

Qualifying Jurisdictions

The simplified and streamlined approach applies an operating expense cross-check as a guardrail for the primary return on sales net profit indicator. As part of this guardrail, a maximum or cap operating return-on-operating-expense (EBIT/Operating Expenses) ratio is specified, and if the actual ratio (as a result of the application of Amount B) exceeds that cap, the Amount B profit margin will be adjusted downward until the resulting return on operating expenses falls to the cap. This cross-check provides for both a default cap rate and an alternative higher cap rate, with the latter being applicable when the tested party is located in a “qualifying jurisdiction.”

The second supplementary guidance document released June 17 identifies the qualified jurisdictions for purposes of this operating expense cross-check cap and clarifies that Inclusive Framework members agreed that the term “qualifying jurisdiction” is not defined by reference to low-capacity. Rather, qualifying jurisdictions for purposes of the operating expense cross-check refers to jurisdictions that are classified by the World Bank Group as low income, lower-middle income, and upper-middle income based on the latest available World Bank Group country classifications.

This guidance document also provides a separate definition and enumeration of qualifying jurisdictions for an adjustment mechanism to the profit determined through the primary Amount B mechanism. Specifically, the return on sales specified in the pricing matrix will be adjusted for distributors in jurisdictions for which the global dataset of distributors does not provide sufficient coverage (the “data availability mechanism” described in Section 5.3 of the Amount B report).

In this context, the new guidance provides that a qualifying jurisdiction refers to jurisdictions with a publicly available long term sovereign credit rating of BBB+ (or equivalent) or lower from a recognized independent credit rating agency, and fewer than five local-country comparables in the global dataset.

The lists of covered jurisdictions and the two types of qualified jurisdictions will be updated every five years and published on the OECD website.

How MGO Can Help

In the evolving landscape of international taxation — where compliance and strategic adaptation are crucial to your success — MGO is uniquely positioned to guide your business through the complexities of the new Amount B framework. By understanding the intricate interplay between global tax regulations and your business operations, MGO can provide tailored guidance to align your transfer pricing strategies with the OECD’s latest guidelines.

Our international tax team excels at helping you identify the right pricing mechanisms and manage the necessary adjustments to optimize your business’s financial outcomes. For inquiries or support in navigating the Amount B framework, reach out to our team today.

MGO navigates stringent OECD guidelines to foster client confidence and deliver an industry advantage.

Background:

In the highly competitive semiconductor manufacturing sector, a global leader with annual revenues exceeding $400 million teamed with MGO for an exhaustive global transfer pricing (TP) study. Our task extended beyond the U.S., covering Asia Pacific (APAC) and Europe, Middle East, and Africa (EMEA) countries, thus providing a comprehensive TP analysis that aligns with both domestic and international standards.

The creation of a global TP study — including master file, local file, and country-by-country-reports — essential under Organization for Economic Co-operation and Development (OECD) guidelines, was pivotal for our client. This document is not merely a formality but a strategic tool that outlines a company’s business operations, supply chain, and global transfer pricing policies. Given the global scrutiny of TP studies, our client required a firm not only to meet the standard but to advocate on their behalf, ensuring the study contained the substantial and relevant information necessary to withstand regulatory examination and protect against penalties.

Approach:

At MGO, we pride ourselves on a bespoke approach to client engagement. We delve deep into understanding our clients’ unique business landscapes, enabling us to manage quality control proactively throughout the project lifecycle. For this semiconductor client, our team crafted a master file that exemplified our commitment to excellence, surpassing OECD’s stringent requirements. The result was a rich, descriptive narrative of the client’s global operations, devoid of numerical data but full of insights that present the company’s practices in the best possible light.

Value to Client:

The ability to provide comprehensive global transfer pricing services traditionally expected from larger firms is a distinctive advantage. This approach effectively combines personalized service with global knowledge and experience. The continuation of our collaboration in a second year and the establishment of a two-year commitment underscores the client’s confidence in receiving high-quality deliverables.

Your Trusted Global Transfer Pricing Provider

MGO is here to help you navigate the complexities of international transfer pricing. Our track record across industries demonstrates our ability to tailor our solutions to meet your needs — helping you maintain compliance, and get more from your global tax strategy. Leverage our experience for your advantage.

MGO brings strategic advantages, cost savings, and efficiency to Silicon Valley’s software giants.

Background:

In the fast-paced environment of Silicon Valley, a publicsoftware company faced a significant challenge: a shortage of skilled staff for its crucial daily transfer pricing (TP) operations. In response to this critical need, the company sought a reliable firm to provide not only services but a flexible staffing solution.

The client needed an immediate and effective solution to maintain their transfer pricing operations without the overhead associated with full-time hires. They wanted quality, efficiency, and a team that could seamlessly integrate into their existing operations under the supervision of their director.

Approach:

MGO crafted a bespoke staffing solution, dedicating a highly skilled professional to work exclusively on this engagement. This strategic move allowed the client to leverage MGO’s experience as if it were an in-house resource — but without the financial and administrative burdens of employment (such as payroll taxes and benefits). The arrangement highlighted MGO’s flexibility and commitment to providing value, offering the client a substantial cost benefit through competitive pricing.

Value to Client:

Over the course of a year, this arrangement not only met but exceeded the client’s expectations, demonstrating MGO’s capability to deliver specialized staffing solutions that align with the unique needs of high-tech companies in Silicon Valley. The engagement underscored the potential for cost savings and operational efficiencies through outsourcing, setting a precedent for how companies can address staffing shortages in specialized areas like transfer pricing. This solution also highlighted MGO’s adeptness in managing and executing transfer pricing tasks for large enterprises with offshore operations.

Transfer Pricing and MGO

MGO approaches outsourcing in a strategic way, emphasizing our team’s readiness to provide tailored solutions to meet the evolving needs of businesses in Silicon Valley and beyond. As companies navigate the complexities of transfer pricing and seek operational efficiencies, MGO remains a trusted advisor, offering flexible staffing solutions to help you achieve your goals.

The IRS has intensified enforcement of transfer pricing regulations, significantly increasing potential penalties.

Organizations can reduce exposure to transfer pricing penalties by ensuring adequate documentation and applying global transfer pricing policies consistently.

In cases where penalties are imposed, businesses can seek penalty abatement by demonstrating reasonable cause and good faith, substantial compliance with transfer pricing rules, and leveraging effective representation from knowledgeable tax advisors.

~

The Internal Revenue Service (IRS) implemented transfer pricing penalties to ensure the intercompany pricing reported on your income tax return is determined in a manner consistent with the arm’s length standard.

Until recently, penalty assessments were rare — not because improper transfer pricing between related parties was rare, but because IRS examiners tended to accept inadequate documentation. That leniency appears to be a thing of the past.

The IRS has indicated it will focus on applying Internal Revenue Code (IRC) Section 6662 penalties where proper documentation is lacking. This trend warrants serious attention if your company engages in cross-border transactions.

Imposing Transfer Pricing Penalties

The IRS can impose penalties when allocations under Section 482 result in substantial or gross increases in taxable income or where there are substantial or gross valuation misstatements concerning the transfer prices themselves.

These penalties can be severe, ranging from 20% to 40% of the tax underpayment, depending on the degree of non-compliance and the taxpayer’s disclosure of relevant information.

Historically, you could avoid these penalties by demonstrating you had reasonably used a transfer pricing method outlined in Section 482 or another method to more reliably determine transfer prices. Taxpayers must also provide contemporaneous documentation within 30 days of a request from the IRS.

The IRS’s Shift Toward Increased Penalty Assertion

The IRS Advisory Council’s 2018 Report noted that, although some transfer pricing documentation quality possibly fell short of the Section 6662 requirements, the IRS had not consistently asserted the penalty. Since then, the IRS has produced guidance addressing common flaws in transfer pricing documentation and best practices, and the agency is now expressing a renewed commitment to applying penalties more frequently and vigorously.

Holly Paz, commissioner of the IRS Large Business and International Division, spoke at several tax practitioner events in late 2022 — including the AICPA’s National Tax Conference, the American Bar Association Section of Taxation’s Philadelphia Tax Conference, and a Bloomberg Tax event. During these events, Paz noted the IRS has had success in litigating transfer pricing cases and is taking a closer look at economic substance and sham transactions — even in cases with transfer pricing documentation — to determine where it is appropriate to assert penalties.

Incorporating these features into your documentation may help reduce your risks:

Sensitivity analysis – Assess the impact of removing a comparable company from the dataset and determine if such removal alters your position relative to the arm’s-length range. Evaluate how different profit-level indicators might change the results.

Segmented financial data analysis – Examine if the segmented financial data accurately reflects the arm’s-length nature of the intercompany transaction. Detail the methodology used in constructing this data.

Profit allocation in intercompany transactions – Analyze profit distribution among entities in the transaction. Ensure equitable economic outcomes for all parties, not just the tested party.

Description of risks and related-party allocations – Describe associated risks in each intercompany transaction. Explain how profits and losses are allocated among related parties.

Atypical business circumstances – Identify any unusual business conditions affecting the intercompany transaction. Discuss challenges in the economic analysis due to specific business results for the year.

To navigate this heightened scrutiny, taxpayers must take a proactive approach to document pricing transfer decisions. Steps you can take to avoid commonly seen inadequacies include:

Providing a detailed description of your business and industry to help IRS agents understand operations and the larger marketplace in which you operate.

Avoid using a checklist format. Instead, opt for a comprehensive analysis linking facts to the analysis. Base the analysis on well-supported facts, avoiding broad assumptions about the business.

Ensure consistency in risk allocation with intercompany agreements. Align risk allocation with the comparable companies used in the economic analysis, and clearly explain any adjustments made to comparable companies for risk considerations.

Prepare a best method selection analysis that justifies rejecting alternative methods for analyzing the intercompany transaction and provides a rationale for the chosen method.

Clearly outline any adjustments to comparable data, such as working capital or location savings adjustments.

If you believe you have valuation misstatements or understated income tax in previously filed returns, it’s not too late to correct them. Filing a qualified amended return before the IRS contacts you about a transfer pricing audit is a defense against penalties. However, you must pay all taxes associated with the amended returns.

Seeking Penalty Abatement

In instances where penalties are assessed, it may be possible for taxpayers to seek abatement by demonstrating high-quality transfer pricing documentation. You may have a reasonable chance of having penalties abated if you:

Demonstrate reasonable cause and good faith. Establish that the underpayment was due to reasonable cause, and you acted in good faith.

Substantial compliance. Show that, despite any errors, you substantially followed the transfer pricing rules.

How We Can Help

The resurgence of transfer pricing penalties is an opportunity to reassess your transfer pricing strategies and compliance mechanisms.

For personalized guidance and assistance navigating these complexities, contact MGO today. Our team of professionals is equipped to help you mitigate risks, confirm compliance, and effectively manage any disputes with tax authorities. Act now to safeguard your business against the pitfalls of transfer pricing penalties.

State tax authorities are escalating audits of intercompany transactions, as transfer pricing crackdowns in several states are generating millions in tax revenue.

These state initiatives indicate growing regulatory emphasis on transfer pricing, which may encourage more aggressive audits (especially if budgets tighten).

Companies operating across state borders should take proactive steps, like conducting transfer pricing studies to validate policies and strengthen defenses before audits strike.

~

A recent Bloomberg article affirms state tax authorities are ramping up audits of intercompany transactions at multistate corporations. The report points to an increase in audits in three “separate-reporting” states following transfer pricing settlement initiatives as a beacon of audit activity to come across other states that take this approach.

While not ideal for multistate operators, this development may not come as a surprise to companies with international operations who have dealt with a myriad of cross-border tax issues in recent years. Close observers of state and local tax (SALT) developments have been predicting for many years the potential that states will be adopting similar positions with respect to transfer pricing. In a 2022 article focused on SALT transfer pricing enforcement, we highlighted several key indicators that more state transfer pricing audits could be on the horizon – including state budget deficits, a surge in auditor and consultant hirings, and renewed interest among states in collaborating on multistate audits.

With confirmation that state-driven transfer pricing audits are on the rise, it is imperative for corporations operating across state borders to assess your transfer pricing risks and fortify your documentation and audit defense strategies.

Surge of Transfer Pricing Audits in Separate-Reporting States

According to the Bloomberg Tax report, the recent spike in transfer pricing audit activity has predominantly affected Southeastern states categorized as separate-reporting states. Currently, there are 17 separate-reporting states in the United States. With the exception of a handful of states like Indiana, Pennsylvania, Iowa, and Delaware, most separate-reporting states are located in the Southeast region.

How separate-reporting states differ from other states in their taxation approach to corporations:

In separate-reporting states, each corporation within an affiliated group is required to file its individual tax return. This treatment considers them as separate entities with independent income, recognizing intercompany transactions, and allowing for varying tax liabilities.

In contrast, combined-reporting states require or allow affiliated corporations within a corporate group to file a single tax return, treating them as a unitary business with shared income, often eliminating intercompany transactions.

Notably, two Southeastern states, Louisiana and North Carolina, have recently concluded audit resolution programs that significantly boosted their state revenues. Louisiana’s program generated nearly $38 million, while North Carolina’s efforts resulted in more than $124 million. Meanwhile, New Jersey, a Mid-Atlantic state that abandoned separate reporting in favor of combined reporting in 2019, is in the midst of a transfer pricing resolution program that has already collected almost $30 million. The success of these programs in collecting tax revenue is likely to motivate other states to explore similar initiatives.

The success and subsequent expansion of these programs signify a growing emphasis on transfer pricing at the state tax authority level. State tax agencies are enhancing their knowledge and enforcement activities in this domain, giving auditors more confidence to adjust returns in transfer pricing disputes. This increasing competency may be viewed as a valuable tool by states – both those requiring separate and combined reporting – that are seeking ways to augment revenue streams.

Strengthen Your Transfer Pricing Defenses Before State Audits Strike

To preemptively safeguard your business from a state transfer pricing audit, a proactive approach to validating pricing policies is essential – and a comprehensive transfer pricing study is your primary defense.

Here are three key advantages of conducting a transfer pricing study:

Document Your Transfer Pricing Policy: A transfer pricing study provides robust documentation that can counter inflated tax assessments by identifying key intercompany transactions, referencing benchmark data, and highlighting any deviations that necessitate policy adjustments. Even if your company has undertaken prior studies, annual updates are indispensable to align with evolving business landscapes and provide tax penalty protection.

Mitigate Your Risk: Beyond reducing audit risks and potential liabilities, these studies also play a pivotal role in supporting major corporate events like mergers and acquisitions (M&A). By demonstrating pricing compliance, they ensure that domestic affiliates have robust documentation and effective cost allocation analysis, thus preventing over-taxation or under-taxation.

Ensure Consistency: Minimize uncertainty by achieving uniform entity-specific compensation across state agencies and affiliated entities. Swift collaboration with advisors when audits arise enhances dispute resolution capabilities.

As states continue to gain confidence in challenging transfer pricing, multistate corporations must take proactive measures to ensure the resilience of their intercompany transactions under intensified scrutiny.

Get Ahead of the Game with a Transfer Pricing Study

If your company engages in substantial intercompany transactions across state lines, initiating a review of your current pricing policies, preparing your transfer pricing policies, and ensuring compliance with U.S. transfer pricing rules should be a top priority. Proactive measures can help you stay ahead of potential issues before state auditors come knocking. We have a robust transfer pricing team that works closely with our State and Local (SALT) Tax and Tax Controversy practices. Through a combined effort we can support you through every stage of managing a transfer pricing audit. Talk to our transfer pricing professionals today to find out how we can help you minimize your exposure to transfer pricing audits.

Recent global events have emphasized the need for reviewing and strengthening the supply chain for manufacturers from both an operational and cost savings perspective.

A “China Plus One” strategy is a good start but may prove inadequate depending on the nature of a disruption.

Supply chain backup plans need to be agile, flexible, and built with contingencies for undetermined issues.

Raising prices may address some concerns but also causes customer issues and is not a long-term solution.

During the COVID-19 pandemic, organizations across different trades and industries faced a number of operational obstacles caused by supply chain disruptions. From economic uncertainty, to labor shortages, to rising costs, leaders had to find alternatives to create an agile and adaptable framework for this ever-changing market. With the global tax overhaul where juristidictions are racing for the middle and not the bottom, companies are faced with continuous change.

Our International Tax and Transfer Pricing leaders have developed methods and problem-solving techniques for local and global networks. These approaches help businesses address their supply chain challenges, as well as give guidance on how to continually evaluate and adjust their strategic initiatives while considering tax and transfer pricing risks in their supply chain decisions. The proverbial tax tail should not wag the dog but it should not be ignored either. Companies should consider performing transfer pricing analyses to determine how to allocate the financial impact of the changes to the supply chain among related entities and ensure appropriate remuneration to those entities involved in supply chain initiatives for their respective functions performed and risk incurred in the process.

In this article, we will answer three of our most-asked questions and provide the necessary steps to transform and optimize supply chains amid constant uncertainty — now and in the future.

#1: Can adopting the “China Plus One” strategy diversify my supply chain?

In recent years, most U.S.-based businesses and consumers have learned that global supply chains have become too dependent on China. Prior to 2020, business leaders had already begun shifting away from China in the wake of the previous administration’s tariff challenges, intangible property (IP) disputes, and the ensuing trade war. Factory and port shutdowns in China in the early days of the pandemic and the issues that have followed were wakeup calls for those that hadn’t implemented alternative sources of supply. An enduring lesson of the past few years is that sole sourcing from any vendor or vendors in one location comes with a high-risk level. In renewing the supply chain, companies must consider the economic climate, the political environment, the ease of doing business, and personnel availability. Tax and transfer pricing is generally not in the forefront nor should it be. But giving it some thought after consider the already mentioned items may pay significant dividends.

Building redundancy into the supply chain at different tiers and maintaining inventory levels have become necessary steps for international manufacturers.The China Plus One strategy has been on the radar of companies that operate in China for several years, but the need to diversify supply chains is now a priority, with many manufacturers actively pursuing supplementary sourcing from another country in Southeast Asia. However, the supply chain crisis of the past two years shows this strategy may also be failing. As long as the goods produced are an ocean away from the markets that consume them, uncertainty from various disruptive factors can lead to shortages, higher costs, lower revenues, and customer dissatisfaction.

Actions moving forward:

Along with decoupling from China, truly de-risking the supply chain comes down to three factors:

Optionality

Redundancy

Market proximity

While fully onshoring production and supply sources may not be operationally, economically, or logistically feasible, the supply network is less risky when it is closer to the market where it is widely consumed.

Consider engaging or contracting new stateside suppliers and local manufacturers to better serve the U.S. market. You should also review your supply base for any overreliance on a single source or geography. After that, you can research the best options to decrease the distance between where your products are produced and purchased. Insourcing, onshoring, nearshoring and acquisitions are all viable options. The approach that makes sense for your business must consider cost, capacity, quality, control, and reputation. Regardless of your approach, the goal should be to improve supply chain resilience and flexibility so you can better manage disruptions.

#2: Does having a back-up plan reduce supply chain disruptions?

Preparation and readiness may help with how your company fares during industry interruptions. A back-up plan should have built-in agility so it can be adapted and activated quickly based on a variety of external factors.

In recent years, manufacturers learned static backup plans were not adequate to address rapidly changing global conditions. These backup strategies were not agile enough to be effective amid complex disruption. Consequently, manufacturers were challenged to get the level of service they needed from existing suppliers or quickly identify new suppliers, resulting in processes that simply were not feasible from an implementation or sustainable cost standpoint.

Backup plans are a necessity, but they’re generally based on known risks. As global supply chains grow more intertwined and the universe of uncertainty expands, new risks and variables come into play. You can’t just plan for one contingency; you need to weigh the possible outcomes for multiple options across different scenarios. Changes in manufacturing locations and sourcing strategies aren’t the only scenarios worth evaluating, nor is resilience to disruption the only outcome worth measuring. For example, if you’re considering expanding into a new market or adding to your product mix, those strategic adjustments should be factored into your supply chain model and assessed for plausibility. Tax liabilities, trade compliance risks, and total cost to serve are no less critical considerations than deliverability or lead times.

The reality is you cannot prepare for every contingency, so scenario planning needs to evolve to detect signals of disruption earlier and enable greater agility in supply chain decision-making when the unexpected occurs. For example, if your company is planning on vertical integration thath will be the cause of significant in-country hiring, you must assess the benefits of employment credits and incentives that can help reduce overhead costs.

Actions moving forward:

Review your supply chain model to:

reflect current constraints;

incorporate points of vulnerability; and

conduct a scenario planning exercise to address a specific problem or inform your next strategic move.

Ideally, you should simulate multiple scenarios to pressure test the supply chain, anticipate issues, and chart the best path forward when disruption hits. Scenario planning should become a regular business practice so you can quickly respond to unforeseen events.

#3: Will raising prices offset the increasing costs of materials and logistics?

Although raising prices is not the only way to successfully reduce costs, there are some tradeoffs that will have to be considered. Higher costs are an unfortunate reality for most manufacturers in the current supply chain environment. Because cost reductions are not easy to accomplish, many companies are shifting their focus to cost containment within areas of their supply chains that they can control. Higher costs are a sure way of reducing taxable income and where possible, selectively deciding where the spend will occur in the supply chain may not reduce the impact of inflation or costs being spent – however it may impact the amount of tax dollars being spent. Tax, like all other costs, is an expense that should be viewed and considered for cost reduction measures.

For example, intercompany movements are often rife with inefficiency or seldom get the level of scrutiny they deserve. If parts and finished goods are shipped intercompany, ask why: Is there a value add, is it because your business has always done it that way, or is it an enabling factor to hedge against process inefficiencies? If your global supply chain is failing to consistently meet the needs of local markets, does the original rationale for keeping production and sources of supply at a distance still stand? Or would it be beneficial to establish a near or local market capability? Using models like a contract manufacturer can be a quicker way to further evaluate whether it makes sense to establish an in-house capability.

It’s also a good time to revisit lean initiatives that you may have previously dismissed or deprioritized—though be cautious of prioritizing efficiency at the expense of resilience. And beyond your own four walls, there are a few foundational measures of good supply chain hygiene that may help with cost takeout:

Shift from transportation spot rates to contract rates to stabilize pricing.

Ensure you have contracts with alternate suppliers; don’t rely on a single source.

Encourage your customers to optimize order volume for full truck or container loads through more rigorous enforcement of transactional service standards.

These measures may help manage costs to some degree but are unlikely to completely offset them. By raising prices, you will more than likely create frustration and confusion among your customers. However, if you find yourself absolutely needing to raise prices, it’s better to be upfront and honest rather than taking a below-the-radar approach.

Another way to address rising costs, rather than passing additional costs onto all your customers, is to consider segmenting them and developing pricing strategies based on level of priority.

Actions moving forward:

Perform an in-depth analysis of your customer base and product suite to understand the most and least profitable segments. Consider implementing a price segmentation strategy that shifts the heaviest burden of cost increases to your least profitable customers. Also, take a close look at your least profitable product segments and how they line up with cost distribution. Do you have slow-moving SKUs driving a disproportionate amount of costs? It may make sense to rationalize them.

We can help strengthen your supply chain

Now is the perfect time for manufacturers to gain competitive advantage by optimizing production and delivery processes and prioritizing long-term spending goals. Our International Tax and Transfer Pricing and Management Advisory practice leaders are ready to assess your current supply chain, identify potential points of weakness, adjusting transfer pricing policies, and assist you in implementing strengthening procedures. Reach out to our team to learn how we can reduce your risk and power production.