The energy tax credit has application for all businesses, nonprofits, and governments, contrary to the belief that only taxable entities benefit.

Even without tax liabilities, organizations investing in renewable energy, energy efficiency, or renewable energy equipment can access substantial incentives, potentially covering 6% to 70% of their investment costs.

MGO Tax Credits and Incentives Director Danielle Bradley details how state and local governments can benefit from federal energy tax credits:

Some credits and incentives have time limitations, such as hiring-based credits eligible only through 2025. If you’re planning to increase your workforce in the next six months, it’s crucial to prioritize this to avoid missing potential opportunities.

MGO Tax Credits and Incentives Director Danielle Bradley offers insights about tax credit and incentive filing requirements:

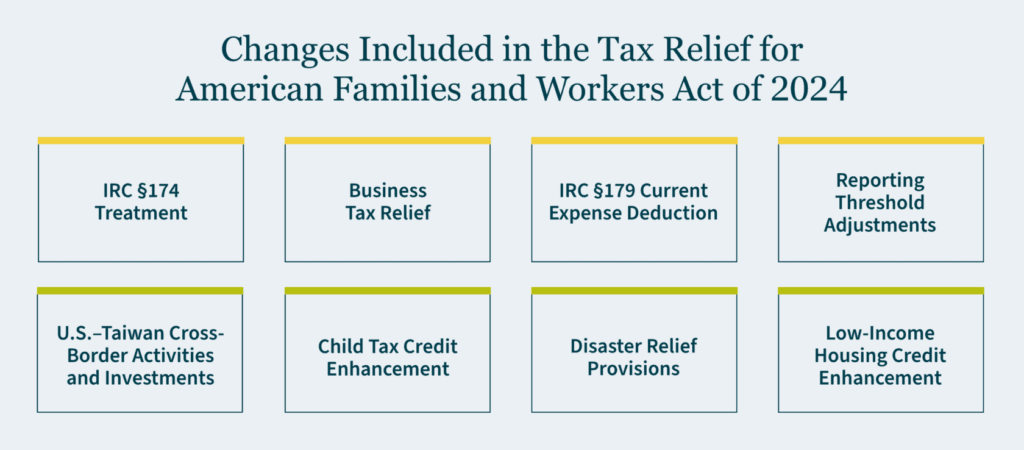

House Ways and Means Committee Chairman Jason Smith and Senate Finance Committee Chairman Ron Wyden announced agreement on a bipartisan tax framework to help families and main street businesses that is anticipated to be introduced as The Tax Relief for American Families and Workers Act of 2024. MGO will continue to monitor the development of the anticipated bill and proposals and provide related updates and information to our clients and network.

Here is a sneak peek into some of the expected goals of the tax framework:

IRC §174 Treatment

Boost innovation and competitiveness by allowing U.S. R&D expenses to be deducted in the year incurred — in comparison to the current 174 mandatory capitalization over five years, that has been in effect since the 2022 tax year. This change is anticipated to be retroactive to the beginning of 2022 and go through 2025. This should create an opportunity to decrease taxable income on an amended 2022 income tax return.

174 capitalization would still be required for foreign expenditures over 15 years.

Business Tax Relief

Retroactive deferral until 2026 of the reduction in the 100% bonus depreciation deduction.

Removal of depreciation, amortization, and depletion deductions from the calculation of adjusted taxable income for the IRC 163(j) business interest expense limitation. This change is also anticipated to be retroactive to the beginning of 2022 and be effective through 2025. This may create an opportunity to decrease taxable income and/or increase tax attributes for the 2022 tax year through an amended 2022 income tax return.

IRC §179 Current Expense Deduction

Increase in the maximum amount to $1.29 million and the investment limitation cap to $3.22 million for property placed in service in 2024, with inflation adjustments for post-2023 tax years.

Reporting Threshold Adjustments

Increase in the reporting threshold for filing Form 1099-NEC and 1099-MISC from $600 to $1,000, applicable to payments made after 2023, with inflation adjustments from 2024.

U.S.–Taiwan Cross-Border Activities and Investments

The bill creates a new section 894A of the Internal Revenue Code (“IRC”), providing substantial benefits to Taiwan residents (“qualified residents of Taiwan”), similar to those that are provided in the 2016 United States Model Income Tax Convention (“U.S. Model Tax Treaty”). Since the legislation requires full reciprocal benefits, it does not come into full effect until Taiwan provides the same set of benefits to U.S. persons with income subject to tax in Taiwan, similar to the reciprocal operation of a tax treaty.

Child Tax Credit Enhancement

Increase in the maximum refundable Child Tax Credit from $1,600 to $1,800 in 2023, $1,900 in 2024, and $2,000 in 2025.

Revision of the refundable portion, calculated on a per-child basis.

Disaster Relief Provisions

Retroactive exclusion of qualified wildfire relief payments from gross income.

Introduction of disaster-related personal casualty loss provisions and treatment of disaster relief payments for victims of the East Palestine, Ohio, train derailment.

Low-Income Housing Credit Enhancement

Enhancing the Low-Income Housing Tax Credit, by restoring the 12.5% LIHTC ceiling for taxable years beginning after December 31, 2022.

What should your business do in the meantime?

R&D/174 Proposed Changes – There likely is no immediate timeline sensitivity for the 174 capitalization requirement currently, unless you are a fiscal year filer or have an upcoming tax provision. In the event you have a return being filed in Q1, we recommend connecting with your tax credits service provider to discuss timeline for a formal analysis and processes. Please note that the anticipated changes are only to U.S. expenditures and therefore any foreign-based expenditures would still require capitalization over 15 years. A formal 174 analysis is recommended to support the research expenditures and to be able to apply the most favorable treatment of either immediately deducting or deferring, in the event of a bill passing and depending on whether the expense is a domestic or international expense.

It is also recommended to assess how the modification of the research and experimentation expense treatment would affect an amended 2022 return and forecasts for the 2023 tax year, especially for businesses that had material domestic research and experimentation expenditures. If all research and experimentation expenditures in the 2022 tax year were foreign, there will be no related change.

Other Business Tax Reliefs and Proposed Modifications – Please connect with your specialty tax service provider to discuss the timeline for your return filings and address forecasts and changes that may be created from these proposed changes. We have summarized a few recommendations and examples:

International

All U.S. citizens and U.S. resident taxpayers with activities within Taiwan should review their activities in light of these provisions to determine if reduced withholding taxes or minimization of creating a taxable presence is possible. All Taiwan residents with activities in the U.S. should review U.S. activities for similar issues.

Private Client Services

Assess how the proposed enhancements of the Child Tax Credit and Assistance for Disaster-Impacted Communities affect your personal deductions and 2023 tax liability.

State and Local Taxation

Evaluate variances in state conformity for the various changes. While some states have rolling conformity and will match changes at the federal level, others have fixed conformity and will not necessarily adopt these changes without further legislation.

Corporate Taxation

Evaluate the need to file an amended return to “unwind” the 2022 Sec. 174 research and development amortization to deduct those costs in full for 2022. This could provide significant refund opportunities.

Assess how the removal of depreciation, amortization, and depletion deductions from the calculation of adjusted taxable income for the IRC 163(j) business interest expense limitation affects taxable income and liability.

It is essential to note that despite this bipartisan breakthrough, the absence of an actual bill and the uncertainties surrounding the enactment of these provisions in a divided Congress should remain critical considerations.

Our perspective

As experienced advisors, MGO can help model the best position for you through the 2023 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors into not only the direct effects of the current legislation (i.e., the proposed tax framework summarized in this article), but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state and local tax) and what potential savings you can obtain by claiming credits and incentives. Please feel free to reach out to any of our MGO professionals below to get the experienced insight that you deserve.

Contact our leaders in the following areas for their specialty or to further address proposals in the tax framework discussed.

Despite bipartisan support, there have been no revisions to the Internal Revenue Code (IRC) Section 174 rules requiring that research and experimentation (R&E) expenditures be capitalized and amortized. Although a policy change that would have postponed this requirement to the 2026 tax year was proposed in last year’s Build Back Better Act (BBBA), that change was never enacted due to the BBBA stalling in the Senate. Subsequent to the BBBA, no other bills – including the Consolidated Appropriations Act (CAA), the final large legislation of 2022 – has been successful in incorporating Section 174 changes into their final versions.

What is the policy now? Well, the Tax Cuts and Jobs Act (TCJA) of 2017 changed the treatment of R&E costs so that taxpayers must capitalize all R&E costs incurred after December 31, 2021, and amortize them over either a five-year period (domestic costs) or a 15-year period (foreign costs). Previously, taxpayers could either (1) immediately deduct R&E expenditures, or (2) elect to amortize those costs over a period of five or more years, which gave the taxpayer the ability to choose the option that would be the most beneficial for them.

While it is still possible for the legislative process to postpone or repeal mandatory capitalization of Section 174 costs (including retroactively applying any changes to the 2022 tax year), such legislation would need to have bipartisan support due to the currently divided Congress.

In this article, we review what it would mean for your business if the much-anticipated revisions to Section 174 do not occur, and what kind of planning you should do to prepare on the front end. A number of these recommendations will be further refined once additional IRS guidance is provided.

Background on 174 R&E expenditures

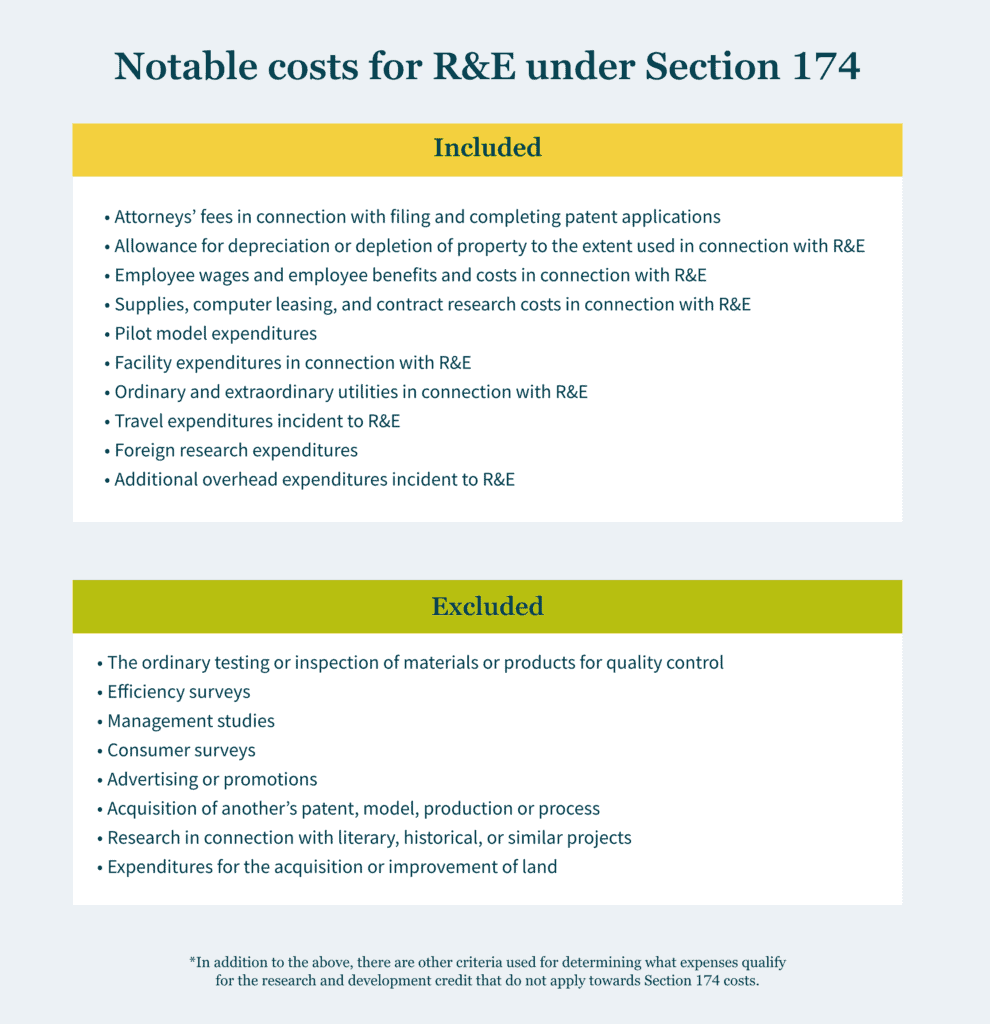

R&E expenses for income tax purposes are defined under Section 174 and its regulations. In Treasury Regulation Section 1.174-2(a), R&E expenditures are described as expenditures incurred by the taxpayer in connection with the taxpayer’s trade or business in the experimental or laboratory sense. Section 174(c)(3) – added by the TCJA – also notes that any amount paid or incurred in connection with the development of any software shall also be an R&E expenditure subject to capitalization. Generally, when determining R&E expenses, not only are direct costs of R&E factored in, but also the indirect costs incident to the development or improvement of a product.

Common expenses included in R&E costs under Section 174 are the following. Many of these expenses are considered for Section 174 specifically and are not qualified research expenses for purposes of the R&D credit.

Attorneys’ fees in connection with filing and completing patent applications.

Allowance for depreciation or depletion of property to the extent used in connection with R&E.

Employee wages and employee benefits and costs in connection with R&E.

Supplies, computer leasing, and contract research costs in connection with R&E.

Pilot model expenditures.

Facility expenditures in connection with R&E.

Ordinary and extraordinary utilities in connection with R&E.

Travel expenditures incident to R&E.

Foreign research expenditures.

Additional overhead expenditures incident to R&E.

*In addition to the above, there are other criteria used for determining what expenses qualify for the R&D credit that do not apply towards determining Section 174 costs.

In contrast, the following are common expenses that are excluded from the expansive definition of R&E costs under Section 174:

the ordinary testing or inspection of materials or products for quality control;

efficiency surveys;

management studies;

consumer surveys;

advertising or promotions;

acquisition of another’s patent, model, production or process;

research in connection with literary, historical, or similar projects; and

expenditures for the acquisition or improvement of land.

The current R&E amortization rule explained

The ability to deduct R&E costs changed for all tax years beginning after December 31, 2021. As previously mentioned, these costs can no longer be deducted in full and must be capitalized and then amortized over five years for domestic costs and over 15 years for foreign costs. This amortization starts at the midpoint of the first year that the expenses were incurred, which results in only 10% of domestic costs (1/2 of 20%) being able to be deducted in their first year.

Per IRS guidance, this mandatory change can be implemented as an automatic accounting method change through attaching a statement to a taxpayer’s first income tax return with a year beginning after 2021, in lieu of filing the much more intricate Form 3115. This change should not have an effect on prior tax years, since the automatic method change is implemented on a “cut-off basis.”

Macro effect of mandatory capitalization

As mentioned above, before the prior rule was changed, every R&E expense could be deducted in full in the year they were incurred. While it is expected that the Section 174 expensing rules will revert to this — to some extent — through pressure from persistent lobbyists, this change has not been incorporated into a bill yet.

Some believe the mandatory R&E capitalization and amortization will adversely affect U.S. innovation, potentially resulting in a detrimental impact on our global competitiveness and jobs. For more than 60 years, businesses were able to immediately deduct their R&D expenses in the year those expenses were incurred (or choose to defer based on what worked for them). Now, the amortization of new R&E costs could cost businesses billions in cash taxes.

Significant considerations

Estimated Tax Payments: For taxpayers making estimated tax payments utilizing current year taxable income, consideration should be given to R&E expenditures and how the capitalization of those expenditures may impact taxable income and timing of cash tax payments. A closer look at refining the various accounts in a taxpayer’s books may be needed for this.

Tax Accounting / ASC 740: Taxpayers should be mindful of whether a new deferred tax asset is created, if any adjustment of existing deferred taxes may be necessary, or if a full or partial valuation allowance may be needed.

Other Areas Affected: The amortization requirement also affects other areas of taxable income, including the following:

increases the deductibility of business interest under Section 163(j),

increases the deductibility of the QBI (Qualified Business Income) deduction,

increases the amount of GILTI (global intangible low-taxed income) for controlled foreign corporations,

potentially adjusts the amount of FDII (foreign derived intangible income) deduction that can be taken,

changes the amount of R&E expenses allocable for purposes of the foreign tax credit, and

impacts state taxable income for the few states that do not conform to the capitalization requirement (e.g., California).

R&D credit considerations

The Section 174 capitalization requirements should not directly impact the amount of expenses that can be used for the R&D Tax Credit under Section 41, since the research credit is calculated using a much smaller subset of R&E expenditures than Section 174 and is not limited by the capitalization requirement. As Section 174 is much broader in scope, it applies to expenditures both eligible and ineligible for the research credit.

Another consideration for tax planning is that the research credit will be even more important to assist with reducing the additional tax liability that will be generated by the R&E treatment change, since the credit can help offset some of the tax liability increase. Moreover, the analysis & processes used to determine the R&D credit can be leveraged to identify Section 174 R&E expenses, which helps create some efficiencies in quantifying the overall effect of the mandatory capitalization and amortization requirement.

Extend impacted returns where possible

Tax return extensions are highly recommended for tax returns that have their due dates coming up. Not only is there the pending IRS guidance that may significantly change R&E expense calculations, but also the act of extending tax returns should allow more time for tax returns to be superseded (rather than amended) and should allow for R&D credit claims to be made on originally filed returns.

This is echoed by a September 2021 Chief Counsel Memorandum issued by the IRS, which made the process for claiming a refund under the R&D credit far more stringent. The memorandum relayed that taxpayers must provide more information on business components, identify the research activities performed, and name the individuals who performed each research activity. Given the additional amount of detail needed, taxpayers making R&D credit claims on amended returns — especially small businesses — have a heavier burden than those who make the claim on an originally filed returns.

How will it affect you?

If the mandatory R&E capitalization requirement is not changed, you should consider how the 174 capitalization rules will affect your business and how claiming the R&D credit will help offset the increase in tax liability. If you currently have an R&D credit analysis and/or an ASC 730 financial statement analysis, those studies can be used as starting points to determine the overall effect of Section 174 — keeping in mind that neither analysis includes all the costs included in Section 174.

If the requirement is changed, there are several ways that the R&E expense landscape could turn out for taxpayers. Ideally, Congress will revert to the prior rule regarding R&D expenses. In that situation, you should be able to choose what is best for you — immediately deducting or deferring.

Our perspective

As experienced advisors, MGO can help model the best R&E position for you, through the 2022 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors not only the direct effects of the R&E capitalization requirement, but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state, and local tax) and what potential savings you can obtain by claiming the R&D credit. Please feel free to reach out to any of our R&E costing professionals below to get the experienced insight that you deserve.

About the author

Danielle Bradley is a senior manager in MGO’s National Tax Credits and Incentives practice. She focuses on helping businesses identify, substantiate, and defend federal and state tax credits and incentives. She has helped hundreds of companies monetize and defend over $100 million in various tax credits and incentives, such as the Research and Development (R&D) Tax Credit, Orphan Drug Credit, Employee Retention Credit, meals and entertainment deduction, and the current Research and Experimental (R&E) amortization calculations. Danielle has extensive experience in various industries, including software and technology, life sciences, manufacturing, aerospace and defense, and food, beverage and agriculture businesses.

Contact Danielle to further discuss the R&E amortization or other credits and incentives at Danielle Bradley or Michael Silvio (Tax Partner).

Thanks to maturing markets, limited access to capital, and disproportionate tax burdens, many companies in the cannabis industry are facing major challenges in managing their debt and creditors. Without ready access to federal bankruptcy protection, many companies with liquidity challenges are looking at their options. Without careful consideration of the tax consequences of these options, companies may be subject to significant tax traps. Here are several factors to consider to avoid these traps and stay solvent from Tax Partner Barbara Webb.

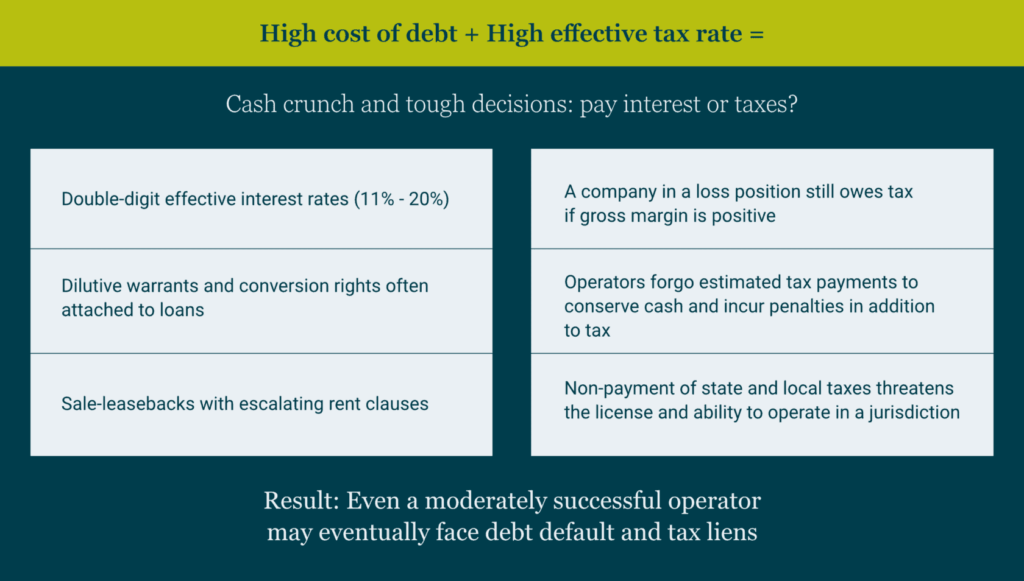

High cost of debt + high effective tax rate = cash crunch and tough decisions

How did cannabis companies arrive at this decision point? The current cash crunch in the industry has been building for years, precipitated in part by banking regulatory constraints and an abnormally high effective federal tax rate.

As the below chart illustrates, cannabis companies lack access to traditional banking and market rate loans and have turned to alternative, expensive sources of debt financing bearing effective interest rates as high as 20%. In addition, Internal Revenue Code Section 280E essentially taxes the industry on gross margins, such that even a company that would otherwise be in an overall tax loss position may still owe taxes.

Caught in this double bind, even an operationally successful cannabis company may face a difficult choice: service debt timely at the expense of keeping current with taxes, risking tax liens that threaten the license, or pay taxes when due at the price of defaulting on debt and risking the viability of the business overall.

The tax impact of debt restructuring

Restructuring debt is one route for cannabis companies in distress to remain operational, but debt modification carries potential tax traps for the unwary – both borrower and lender. Depending on the relative value of the debt exchanged, the borrower can realize cancellation of debt income. The insolvency exception to recognizing and paying current tax on this income may not be available to a cannabis company, as the fair value of its assets – including intangibles – may still exceed its liabilities. A lender may also experience a taxable event on the refinancing, either in the form of interest income, or gain due to the valuation of equity received in the exchange.

In any debt refinancing situation, both the borrower and the lender should anticipate and plan for complex tax calculations involving debt discounts (I.e., original issue discount, or OID) and the fair value of company equity in order to determine correct tax treatment. To avoid any last-minute surprises or deal delays, both the borrower and the lender should model the tax treatment on both sides.

Sales of distressed assets and the tax impact

Considerations for the borrower:

Are the assets to be sold in a different tax filing entity as the borrower?

Will the flow of cash between entities create a taxable event?

Considerations for the lender:

What is the borrower’s anticipated cash position after paying tax on the sale?

Can cannabis business assets be sold in the jurisdiction’s regulatory environment? Or is a sale restricted to equity?

Assignment of income receipt of equity

If the borrower and the lender agree on a debt workout based on assignment of income, or equity ownership, both parties should understand the borrower’s existing tax structure and the impact the restructuring will have on both sides.

The borrower should assess whether a “change in control” has occurred for tax purposes, as the use of tax attributes may be limited. If an assignment of income is structured as a fee, consider the tax treatment of the payment and deductibility under 280E.

A lender who becomes an owner or part of management should consider:

Depending on how the agreement is structured, the assignment of operating income and participation in management may turn the lender, or the lender’s entity, into a “trafficker” subject to 280E.

The lender should also be cognizant of the borrower’s standing with the taxing authorities and whether the operator can afford both paying down tax liabilities and payments under the terms of the workout. The retention of the cannabis or reseller license that the lender is depending on for cash flow is tied to staying current with state and local taxes. An IRS liability that has progressed to the lien stage unbeknownst to the lender could result in a “sudden” drain of cash from a bank account.

“Workouts” with taxing authorities

Given the current cash crunch in the industry, companies have been known to delay remittance of sales and excise taxes to state and local governments. Companies should be aware that non-payment of these “trustee” taxes can cause a loss of standing to operate legally and carries personal liability for officers and owners of the company. Taxing authorities may have limited sympathy for a distressed taxpayer who falls behind on these types of taxes and taxpayers should pay down any outstanding balances as soon as possible.

If income taxes are past due, it is important to continue to make payments toward the balance on a regular basis. A taxpayer cannot apply for a formal IRS payment plan until a revenue officer is assigned to the case. Also, a taxpayer must usually pay all outstanding taxes that are not overdue and remain “current” on all future taxes in order to establish and remain on an installment agreement. Federal and state revenue officers are generally willing to work with taxpayers in financial distress who act in good faith throughout the process. Engaging a professional representative who understands tax controversy practice and procedure and how to work with revenue officers can make all the difference between establishing a payment plan and facing a tax lien.

How MGO can help

A cannabis company navigating financial distress should engage a tax professional with both industry experience and a high level of tax technical skill to navigate the complex tax impact of a workout or restructuring. MGO’s Cannabis Tax team has both the industry experience and the technical knowledge to assist companies of all sizes during this challenging time.

President Biden has signed the Inflation Reduction Act of 2022 into law.

This large package contains many new tax credits to incentivize taxpayers to “go green” with energy from renewable resources while simultaneously receiving financial relief.

It also extends or adds to currently existing credits for additional tax-saving opportunities.

These new credits are aimed at motivating taxpayers to use energy from renewable sources, prioritizing options like wind and solar. The IRA also introduces new credits and strengthens or extends existing credits that provide tax relief for purchasing new and used clean-energy vehicles and installing energy efficient heating and cooling systems. Additionally, companies that cut their methane emissions can access certain credits, while those that do not could face penalties.

The rules and regulations around claiming these green credits can be complicated. In this article, our Tax Credits and Incentives team breaks down how individuals and organizations can capitalize on these tax saving opportunities.

Swap gas guzzlers for an electric vehicle

Taxpayers that purchase a new or used “clean car” can qualify for this consumer tax credit. Vehicles considered clean are those that use a battery partly or fully manufactured in North America and built with materials extracted or processed in one of the countries currently in a free-trade agreement with the U.S.

Your income is a factor in how much you can reap in tax credits. If a taxpayer makes less than $150,000 annually (or has a combined family income below $300,000), the taxpayer can get up to $7,500 for new electric vehicles that qualify. Note the money would be applied at the point of sale, so the taxpayer’s monthly payments would be lowered (as opposed to reducing the tax bill months down the line).

Previously, the federal tax credit for electric vehicles did not include cars from manufacturers that already sold at least 200,000 models (GM, Toyota, and Tesla were excluded). This bill unravels that; instead, there is now a price threshold per vehicle. To qualify for the credit, bigger vehicles like SUVs, pickup trucks, and vans would have to cost less than $80,000 to qualify for the credits. Smaller vehicles are capped at $55,000. So, if you have your eye on a super sporty electric vehicle, you may be out of luck.

Taxpayers can also get $4,000 off a used electric vehicle if it is sold by a dealer for $25,000 or less — but only if they individually make up to $75,000 annually or $150,000 jointly. The addition of credits for used electric vehicle purchases is a win for the industry, and advocates of the bill are hopeful that this incentive will encourage an increase in electric vehicle adoption.

Modifying your home to be more energy efficient

To incentivize taxpayers to make their homes more energy efficient, the bill’s $4.28 billion High-Efficiency Electric Home Rebate Program provides rebates for low- and moderate-income households when they replace fossil-fuel boilers, furnaces, water heaters, and stoves with more efficient electric devices powered by renewable energy.

Some taxpayers will need to upgrade their electrical panels before they are able to install the new appliances. They can take advantage of up to $4,000 to do so. Furthermore, if they are interested in making their home generally more energy efficient, they can capitalize on a rebate of up to $1,600 given to seal and insulate their house, as well as up to $2,500 to improve their home’s wiring.

In terms of appliances, taxpayers can get up to $8,000 to install heat pumps that both heat and cool their home, plus as much as $1,750 for a heat-pump water heater. To offset the cost of a heat-pump dryer or electric stove, taxpayers can claim up to $840. It is estimated by making these changes, they can save significantly on their future energy bills.

There are several parameters for these rebates. First, the program runs through September 30, 2031 — so you do have time to implement these changes to your home. The maximum amount taxpayers can collect is $14,000, and to qualify, their household income cannot exceed $150% of the median income in the area they live. For those who do not qualify, there is a tax credit of up to $2,000 available to install heat pumps, plus up to $1,200 annually to install new windows, doors, or an induction stove.

Save when installing solar panels

Lastly, taxpayers can collect a 30% tax credit for installing residential solar panels through December 31, 2034. The credit decreases to 26% if you wait until after December 31, 2032. Taxpayers can also install solar battery systems to qualify for the tax credit.

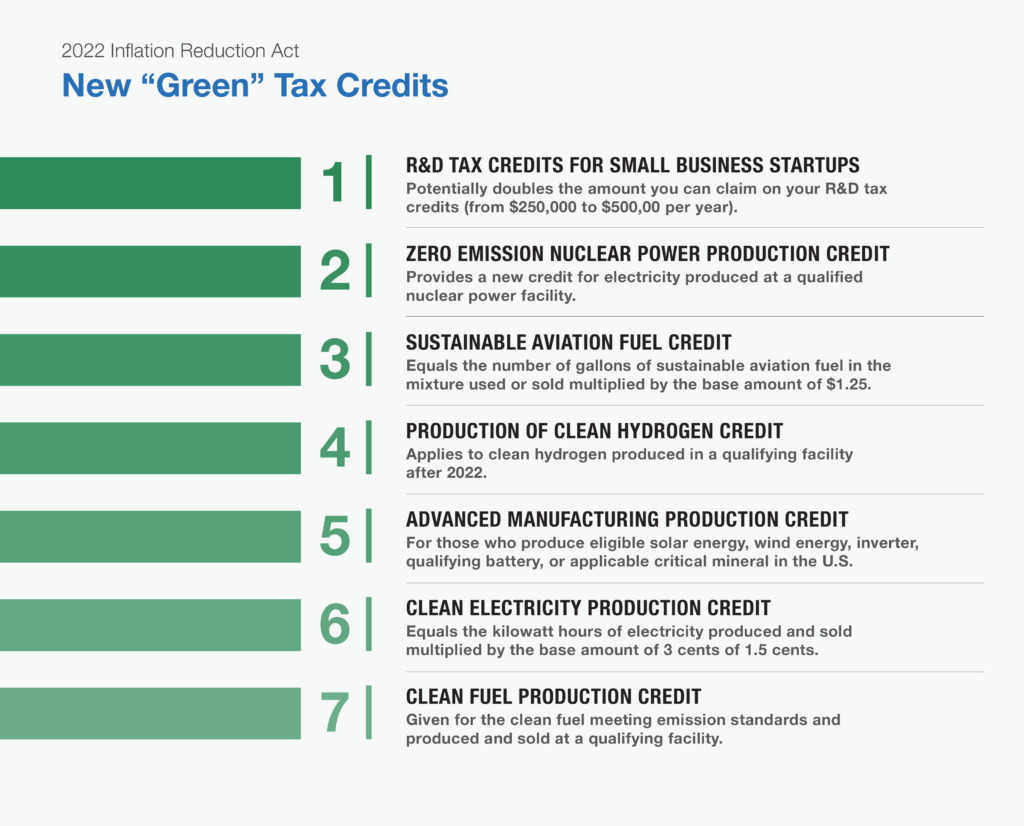

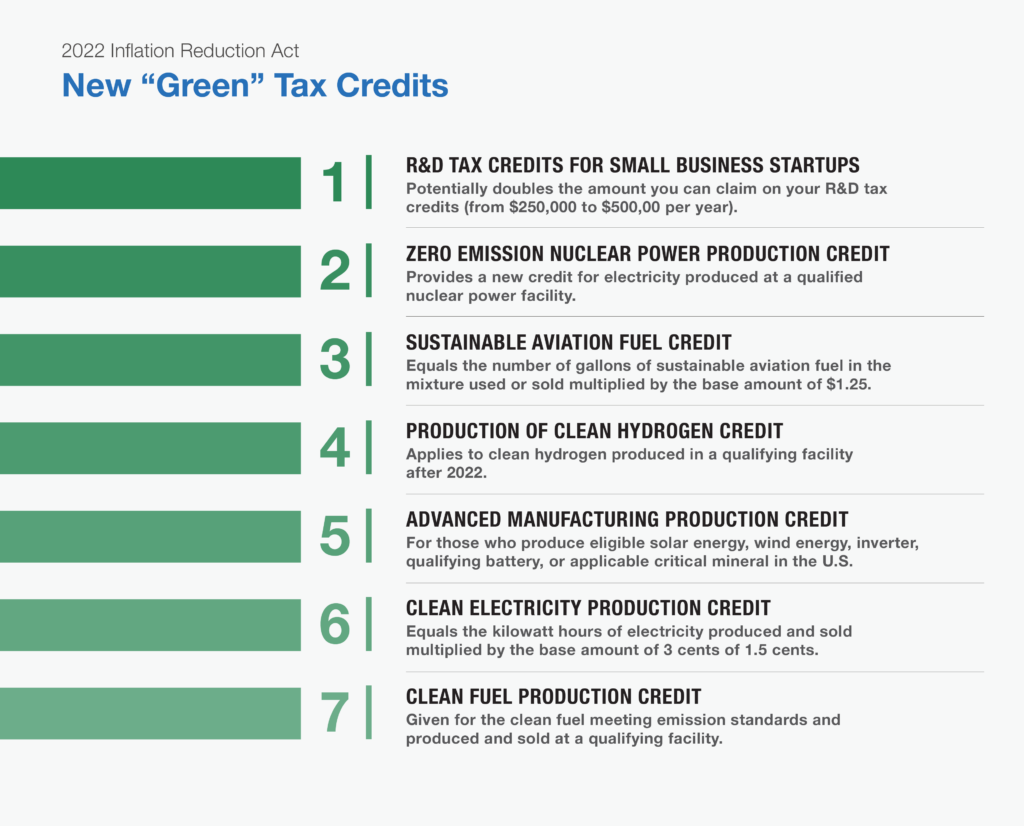

New “green” tax credits

There are other ways taxpayers can take advantage of going green. Here are some of the new tax credits to capitalize on.

Doubling of R&D Tax Credits for Small Business Startups — Would potentially allow recipients to double the amount they can claim on any R&D tax credits (from $250,000 to $500,000 per year against payroll taxes).

Zero Emission Nuclear Power Production Credit — Provides a new business credit for electricity produced by a taxpayer at a qualified nuclear power facility before the date of enactment.

Sustainable Aviation Fuel Credit – Creates a new business credit for each gallon of sustainable aviation fuel sold or used as part of a qualified fuel mixture. The credit equals the number of gallons of sustainable aviation fuel in the mixture multiplied by the base amount of $1.25. There are increases available if the taxpayer meets certain greenhouse gas emissions reductions, and it applies to fuel sold or used in 2023 and 2024.

Production of Clean Hydrogen Credit — Given to producers of clean hydrogen during the ten-year period beginning on the date a qualifying facility is originally placed in service. It applies to clean hydrogen produced after 2022.

Advanced Manufacturing Production Credit — Provides a new production credit for each eligible solar energy component, wind energy component, eligible inverter, qualifying battery component, and applicable critical mineral produced by a taxpayer in the U.S. (or in U.S. possession and sold to an unrelated person). It applies to components and minerals produced and sold after 2022.

Clean Electricity Production Credit — New business credit for clean electricity facilities placed in service after 2024 (where the greenhouse gas emissions rate is not greater than zero). The credit amount equals the kilowatt hours of electricity produced and sold multiplied by the base amount of 3 cents or 1.5 cents. The credit will phase out one year after the later of 2032 or the year when annual greenhouse gas emissions from U.S. production are equal to less than 25% of the 2022 emissions rate (whichever comes first).

Clean Electricity Investment Credit — New investment credit for clean electricity property investments in energy storage technology and qualified facilities placed in service after 2024 where the greenhouse gas emissions rate is not greater than zero. It phases out after the later of 2032 or when the annual greenhouse gas emissions from U.S. electricity production are equal to or less than 25% of the 2022 emission rate (whichever comes first).

Clean Fuel Production Credit — Creates a business credit for the clean fuel a taxpayer produces at a qualifying facility and sells for qualifying purposes. The fuel must meet certain emissions standards.

Extension and modification of “green” tax credits

Several tax credits already in existence were extended and modified in the Inflation Reduction Act. They include:

Renewable Electricity Production Tax Credit (PTC) — Extends the beginning of construction deadline for certain renewable electricity production facilities through the end of 2024, as well as reduces the base amount of credit with the potential to qualify for five times that amount. It applies to facilities placed in service after 2021, and increases the credit amounts for domestic content, energy communities, and hydropower.

Energy Investment Tax (ITC) — Extends the beginning of construction deadline for some types of energy property, including qualified fuel cell property, for one year through the end of 2024. It extends the beginning of construction deadline for geothermal equipment through the end of 2034 and permits the credit for new types of energy property like energy storage technology, microgrid controller property, and qualified biogas.

Carbon Oxide Sequestration Credit — Extends and enhances carbon oxide sequestration credits for qualified industrial facilities and direct air capture facilities IF construction begins before 2033. It also lowers the minimum carbon capture requirement, and generally applies to those facilities and equipment placed in service post-2022.

Tax Credits for Biodiesel, Renewable Diesel, and Alternative Fuels — Extends these tax credits through 2024 and apply to fuel sold or used after 2021.

Second Generation Biofuel Credit — Extends tax credits to second generation biofuel through 2024 and applies to second generation biofuel production after 2021.

Nonbusiness Energy Property Credit — Extends this credit through 2023, as well as changes the credit rate to 30% for both qualified energy efficiency improvements and residential energy property expenditures. It replaces the $500 lifetime limit with a $1200 annual limit, modifies the limits for specific types of property, and modifies standards for qualified energy efficiency improvements on property placed in service after 2022.

Residential Energy Efficient Property Credit — Extends the residential energy-efficient property credit through 2034 and replaces the credit for biomass fuel property expenditures with a new credit for battery storage technology expenditures on those made after 2022.

New Energy Efficient Home Credit — Extends the business credit for contractors who manufacture or construct energy efficient homes through 2032. It applies to dwellings acquired by the contractor after 2022.

Alternative Fuel Vehicle Refueling Property Credit — Extends the tax credit through 2032 and increases the credit limit to $100,000 per item of depreciable refueling property and $1,000 per item of non-depreciable refueling property.

Advanced Energy Project Credit — Extends the competitively awarded investment tax credit for clean energy and energy efficiency manufacturing projects. It provides as much as $10 billion of new credit allocations effective in early 2023.

Increase in Energy Credit for Solar and Wind Facilities — In order to qualify, one must have a maximum net output of less than five megawatts and must be in a low-income community, on American Indian land, or part of a low-income residential building project (or low-income economic benefit project), effective in early 2023.

Reinstatement of Superfund Hazardous Substance Financing Rate — Reinstates a financing rate on crude oil and imported petroleum products at a rate of 16.4 cents per gallon through 2032.

Our perspective on the Inflation Reduction Act’s tax credits

Looking ahead, it is imperative that you are ready to capitalize on these tax credits. Getting into the weeds with some of the qualifications, however, could prove challenging, and working with a professional services firm could make all the difference in ensuring you take advantage of the credits you qualify for.

At MGO, our dedicated Tax Credits and Incentives team brings more than 30 years of experience in helping you structure your expenses in a way that will help you acquire appropriate documentation, assist in calculating and claiming credits, and maximize the amount you can receive. Our full-service firm, led by experienced CPAs and attorneys, provides a holistic approach to examining your organization and determining how you can best reach your goals.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

You’ve figured out who gets the beloved Hermès Kelly bag. You’ve split custody — of both the kids and the dog. The boat’s been sold. And, miraculously, everyone’s feeling pretty amicable. Divorce: it’s not something you ever anticipated, but it’s happening, and you feel prepared.

We just have one question: have you hired a Certified Divorce Financial Analyst (CDFA®) yet?

The truth of the matter is, your attorney can do a lot, but they can’t provide all the guidance you need. Read on to learn the five things you don’t know about the tax implications of a divorce — and why you should hire a CDFA for your own financial security and peace of mind.

1: Be prepared for the long haul

It’s great that you and your former spouse are on good terms now, but you want to make sure you understand the divorce’s full scope of financial impact. Splitting everything down the middle sounds easy, but things are rarely simple, and the process could take longer than anticipated — especially if you want to make sure your interests are being looked after. As soon as you’ve decided on a divorce, equip yourself with financial knowledge by hiring a CDFA. If you know your interests, you have control over how they are handled, giving you the upper hand, preventing you from being blindsided later — no matter how long the “long haul” ends up being.

2: Know your long-term tax liabilities for the assets you’re divvying up pre-divorce

Whether it is interest-free bonds, the house you raised your kids in, your retirement fund, or a timeshare to Walt Disney World, there will be tax consequences and implications for the assets you divide between the two of you.

Often, people look at the fair market value of jointly owned property instead of a property’s tax basis, assuming that this is enough to go on when divvying up. But let’s say you have two different assets you’re splitting “fairly”: stock options and undeveloped land (you never did get around to building that second home together … ). Both assets are valued at the same amount. So, naturally, it makes sense for you to get one, and your spouse to get the other. That is, until one of you sells your asset, and you get a hefty tax bill. This is considered a tax carryforward, and you should understand them before the divorce is finalized.

Tax carryforwards are important to consider when dividing assets because of the tax consequences — and planning opportunities — that could exist in the future. They include carryovers like:

net operating loss carryovers,

business tax credit carryovers,

capital loss carryovers,

excess business loss carryovers,

investment interest expense carryovers, and

suspended passive activity loss carryovers.

Tax regulations give you a great framework, but unfortunately, they do not tell you how these carryovers should be allocated between you and your spouse; instead, you must decide. A CPA should be leveraged to identify the tax considerations, as well as any potential impact they could have on each spouse.

3: Rely on a seasoned professional to gain the full financial picture

You don’t want to think this way, but you need to be prepared for the fact your spouse may have been getting away with unsavory tax practices you were not aware of when you were married. And if so, you need someone on your side. A CDFA can help you gain the clarity and understanding you will need to strategize so you are satisfied with the choices you make during a divorce long after the marriage is dissolved.

For example, imagine your spouse purchased a Mercedes-Benz G-Wagon SUV during the marriage. At the time, you thought everything was above board. But your analyst uncovers that the G-Wagon’s full value was written off because of the weight, thus showing a lower annual income — negatively impacting you and your likelihood of a fair division of property and income.

To combat this, your CDFA would provide a lifestyle analysis. This entails scrutinizing everything from tax returns to credit card transactions, which could uncover hidden trails of unreported income or assets in the uncovered discrepancies. The party’s liquid assets may not support their current standard of living with business class flights abroad and stays at the newest Dorchester Collection hotel. An analysis would show the warning signs.

The examinations and reports gathered by an analyst can show both you and your attorneys a clear picture of the financial matters you’re dealing with on both sides, which can contribute to an equitable resolution between parties. This applies whether you settle or go to court. If it’s the latter, your CDFA can be an invaluable witness on your “team.”

4: Conduct a financial analysis early in the divorce process

As we mentioned, projecting financial impacts for both the short- and long-term is critical to understanding how you will be affected by the divorce. Have your CDFA prepare an independent analysis of the tax consequences under different scenarios, so you know possible outcomes. This will not only create a framework for you moving forward, but it will prevent your partner from successfully sneaking around and attempting to pull the wool over your eyes. These financial analyses can also include a review of the last income tax return filed by your spouse.

5: Remember, this service pays for itself

You may be tempted to forgo a CDFA in the throes of your divorce, thinking it’s just another bill to pay. But the truth is, the service they provide does pay for itself. If fraud or misuse is identified at any point in the divorce process, you will save yourself money in the long run having prepared for these tax liability scenarios, and when it comes to figuring out your assets, you will be able to see beyond the current fair market value, so you won’t be blindsided later on.

Our perspective on hiring a CDFA for your divorce

At the end of the day, think of the financial side of your divorce like a puzzle: you need each and every piece in order to complete the picture. While you may be on good terms with your spouse now, things are rarely simple when money is involved. It is far better to see the puzzle in its entirety now instead of picking up a piece that got edged under the sofa later and discovering you’ve been misled or treated unfairly.

Hiring a CDFA purges the emotion from the situation, which is exactly what you must do to ensure your financial security.

The end of the tax year is fast approaching for many businesses, but their ability to engage in traditional year-end planning may be hampered by the specter of looming tax legislation. The budget reconciliation bill, dubbed the Build Back Better Act (BBBA), is likely to include provisions affecting the taxation of businesses — although its passage is uncertain at this time.

While it appears that several of the more disadvantageous provisions targeting businesses won’t make it into the final bill, others may. In addition, some temporary provisions are coming to an end, requiring businesses to take action before year end to capitalize on them. As Congress continues to negotiate the final bill, here are some areas where you could act now to reduce your business’s 2021 tax bill.

Research and experimentation

Section 174 research and experimental (R&E) expenditures generally refer to research and development costs in the experimental or laboratory sense. They include costs related to activities intended to uncover information that would eliminate uncertainty about the development or improvement of a product. Currently, businesses can deduct R&E expenditures in the year they’re incurred or paid. Alternatively, they can capitalize and amortize the costs over at least five years. Software development costs also can be immediately expensed, amortized over five years from the date of completion or amortized over three years from the date the software is placed in service.

However, under the Tax Cuts and Jobs Act (TCJA), that tax treatment is scheduled to expire after 2021. Beginning next year, you can’t deduct R&E costs in the year incurred. Instead, you must amortize such expenses incurred in the United States over five years and expenses incurred outside the country over 15 years. In addition, the TCJA requires that software development costs be treated as Sec. 174 expenses.

The BBBA may include a provision that delays the capitalization and amortization requirements to 2026, but it’s far from a sure thing. You might consider accelerating research expenses into 2021 to maximize your deductions and reduce the amount you may need to begin to capitalize starting next year.

Income and expense timing

Accelerating expenses into the current tax year and deferring income until the next year is a tried-and-true tax reduction strategy for businesses that use cash-basis accounting. These businesses might, for example, delay billing until later in December than they usually do, stock up on supplies and expedite bonus payments.

But the strategy is advised only for businesses that expect to be in the same or a lower tax bracket the following year — and you may expect greater profits in 2022, as the pandemic hopefully winds down. If that’s the case, your deductions could be worth more next year, so you’d want to delay expenses, while accelerating your collection of income. Moreover, under some proposed provisions in the BBBA, certain businesses may find themselves facing higher tax rates in 2022.

For example, the BBBA may expand the net investment income tax (NIIT) to include active business income from pass-through businesses. The owners of pass-through businesses — who report their business income on their individual income tax returns — also could be subject to a new 5% “surtax” on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million.

Capital assets

The traditional approach of making capital purchases before year-end remains effective for reducing taxes in 2021, bearing in mind the timing issues discussed above. Businesses can deduct 100% of the cost of new and used (subject to certain conditions) qualified property in the year the property is placed in service. You can take advantage of this bonus depreciation by purchasing computer systems, software, vehicles, machinery, equipment and office furniture, among other items. Bonus depreciation also is available for qualified improvement property (generally, interior improvements to nonresidential real property) placed in service this year. Special rules apply to property with a longer production period.

Of course, if you face higher tax rates going forward, depreciation deductions would be worth more in the future. The good news is that you can purchase qualifying property before year-end but wait until your tax filing deadline, including extensions, to determine the optimal approach.

You can also cut your taxes in 2021 with Sec. 179 expensing (deducting the entire cost). It’s available for several types of improvements to nonresidential real property, including roofs, HVAC, fire protection systems, alarm systems and security systems.

The maximum deduction for 2021 is $1.05 million (the maximum deduction also is limited to the amount of income from business activity). The deduction begins phasing out on a dollar-for-dollar basis when qualifying property placed in service this year exceeds $2.62 million. Again, you needn’t decide whether to take the immediate deduction until filing time.

Business meals

Not every tax-cutting tactic has to be dry and dull. One temporary tax provision gives you an incentive to enjoy a little fun.

For 2021 and 2022, businesses can generally deduct 100% (compared with the normal 50%) of qualifying business meals. In addition to meals incurred at and provided by restaurants, qualifying expenses include those for company events, such as holiday parties. As many employees and customers return to the workplace for the first time after extended pandemic-related absences, a company celebration could reap you both a tax break and a valuable chance to reconnect and re-engage.

Stay tuned

The TCJA was signed into law with little more than a week left in 2017. It’s possible the BBBA similarly could come down to the wire, so be prepared to take quick action in the waning days of 2021. Turn to us for the latest information.

The corporate fundraising environment has changed dramatically this year due to several factors, including a wide sell off in the equity markets, high interest rates, inflation, and a general tightening of the credit markets. Prior to the recent downturn, companies had the luxury of spending to develop their products and marketing ideas first, and then focusing on turning a profit later.

Because of these newly tightened conditions, companies may face challenges when raising capital, forcing them to adopt a more thoughtful approach to seek funding. Likewise, investors will want to ensure their priorities are protected and their returns met. The combination of a given borrower’s need for capital and a financer’s desire to seek favorable returns may lead to the creation of agreements that have characteristics of both debt and equity. As such, it is crucial for all parties involved to understand the resulting tax classification and the treatment of these arrangements, so all expectations are met.

The taxation of debt and equity

For borrowers, the difference between debt and equity can be critical because interest payments are generally tax deductible and subject to certain limitations. Dividends or other payments related to equity would not be deductible for U.S. federal income tax purposes.

Enacted as part of the Tax Cuts and Job Act (TCJA) of 2017, one main limit on interest deductibility is the IRC 163(j) limit on the amount of business interest that can be deducted each year. This limit is calculated as 30 percent of adjusted taxable income, which prior to the 2022 tax year closely resembled earnings before interest, taxes, depreciation, and amortization (EBITDA). However, starting with the 2022 tax year adjusted taxable income excludes depreciation and amortization, becoming EBIT. This should result in a lower limit on the amount of interest expense that can be deducted each year. Any interest expense exceeding this annual limit can be carried forward to future years.

Determining if an arrangement is debt or equity for federal income tax purposes

Classifying an arrangement as debt or equity is made on a case-by-case basis depending on the facts and circumstances of a given agreement. While there is currently little guidance in this area beyond case law, the Internal Revenue Service (IRS) has issued a list of factors to consider when questioning whether something is debt or equity. (Keep in mind, however, that the IRS states not one factor is conclusive.) The factors include whether:

An agreement contains an unconditional promise to pay a sum certain on demand or at maturity,

A lender can enforce the payment of principal and interest by the borrower, and

A borrower is thinly capitalized.

The courts have also established a broader — but similar — list of factors to consider when determining whether an instrument should be treated as debt or equity. Both the IRS and the courts have generally placed more weight on whether an instrument provides for the rights and remedies of a creditor, whether the parties intend to establish a debtor-creditor relationship, and if the intent is economically feasible. Some factors include:

Participation in management (as a result of advances),

Identity of interest between creditor and stockholder,

Thinness of capital structure in relation to debt, and

Ability of a corporation to obtain credit from outside sources.

For international companies, the characterization of debt or equity when considered in a cross-border funding arrangement is important, as withholding tax rates may apply to interest payments and may differ from tax rates applied to dividends. Further, withholding tax obligations occurs when a cash payment is made. If you have a cross-border arrangement, it is crucial to know if you have debt or equity on your hands.

Special rules related to payment-in-kind

Once it is determined that an agreement should be classified as debt for U.S. federal income tax purposes, some borrowers may prefer to set aside interest payments or pay interest with securities, which is often referred to as payment-in-kind (PIK). This is generally done to preserve cash flow for operations and growth of the business. When a borrower chooses this route, U.S. federal income tax rules will impute an interest payment to the lender.

While using a PIK mechanism will not automatically result in the debt being recharacterized as equity for federal income tax purposes, it can support viewing the instrument as equity.

Limits to deductible debt interest

There are limitations that can apply to interest deductibility. As noted above, IRC 163(j) limits deductibility of business interest; for a corporation, this is deemed to be all interest regardless of use. Another provision that can result in interest deductibility limitation is IRC 163(l), which applies to certain convertible notes and similar instruments held by corporations.

For cannabis operators, it is important to consider that IRC 280E disallows interest deductions. Hence, it is highly detrimental for cannabis operators to issue debt from entities that are cannabis plant-touching.

How we can help

Due to the nature of the debt versus equity analysis, companies thinking about fundraising should plan on how they intend to perform the raise and whether to have the raise treated as equity or debt. If debt classification is desired, a borrower should take the steps needed to strengthen the facts of the transaction to support the arrangement as a debt instrument.

MGO’s dedicated tax team has extensive experience advising companies across industries on capital-raising, debt refinancing and restructuring, recapitalizations, and other tax transactions. If you are planning to fundraise, or you are currently in the process of conducting a debt versus equity analysis, contact us today.

On August 16th, 2022, President Biden signed the Inflation Reduction Act (IRA) of 2022 into law. The Act is a slimmed down version of the Biden Administration’s proposed Build Back Better legislation and addresses several key areas including:

Increasing Internal Revenue Service (IRS) budget

Implementing a corporate tax minimum

Instituting and increasing tax credits focused on investing in green technologies

Notable items that were not addressed in the IRA include removing the $10,000 SALT cap and mandatory capitalization of research and development (R&D) expenses, both provisions of the Tax Cuts and Jobs Act of 2017.

The bill is over 300 pages in length with a number of wide-ranging components. In the following summary we’ll provide the key points that will be affecting taxpayers in the coming years.

Additional funding to the IRS for tax enforcement

One of the most talked-about provisions involves increased funding for the IRS.

Key details:

Approximately $80 billion in funding over the next 10 years for tax services, operations support, business system modernization, and enforcement

Enforcement – $46 billion

Operations support – $25 billion

Business systems modernization – $5 billion

Taxpayer services – $3 billion

An estimated $124 to $200 billion will be generated from enforcement and compliance efforts

Enforcement is focused on taxpayers – both corporate and non-corporate – with income greater than $400,000

Extension of the business loss limitation of noncorporate taxpayers

The IRA extends the excess business loss limitation for noncorporate taxpayers.

Key details:

Two year extension on IRC Sec. 461(l) until December 31, 2028

IRC Sec. 461(l) limits noncorporate taxpayers from deducting business losses above thresholds that are annually indexed for inflation

These limits are $540,000 for married filing jointly and $270,000 for single and married filing single for the 2022 tax year

Suspended amounts are converted to net operating losses and may be able to be used in subsequent years

Excise tax on repurchases of corporate stock

The IRA includes a 1% excise tax on stock repurchases by domestic public companies listed on an established securities market. The tax applies to repurchases executed after December 31st, 2022.

Key details:

1% excise tax on the full market value (FMV) of stock repurchased by publicly traded US corporations

Will impact redemptions and certain acquisitions and repurchases of publicly traded foreign corporation stock

Not an income tax for purposes of ASC 740

Includes special rules for “applicable foreign corporations” and “surrogate foreign corporations”

Notable exceptions:

Stock is contributed to employer sponsored retirement plan

Stock repurchase is part of a corporate reorganization

Total value of stock repurchased during the taxable year does not exceed $1 million

Repurchase by securities dealer in ordinary course of business

If the repurchase qualifies as a dividend

If the repurchase is by a regulated investment company (RIC) or a real estate investment trust (REIT)

15% corporate alternative minimum tax

The IRA reinstates the corporate alternative minimum tax (AMT) for large corporations, which had been previously eliminated by the Trump Administration’s Tax Cuts and Jobs Act.

Two key elements to note is that this revised AMT only impacts corporations with annual profits exceeding $1 billion, and includes carve-outs for certain manufacturers and subsidiaries of private equity firms.

Key details:

15% tax on adjusted financial statement income (i.e., this would be a book minimum tax)

Affects tax years beginning after December 31, 2022

Applies to corporations with profits over $1 billion based off adjusted financial income

For US corporations with foreign parents, it would apply to income earned in the US of $100 million or more of average annual earnings in three prior years and where the overall international financial reporting group has income of $1 billion or more

Treatment of split offs remains uncertain. Even though these are tax-free reorganizations for tax purposes, gain is recorded for financial accounting purposes

Joint Committee on Taxation expects that this new tax would apply to only about 150 corporate taxpayers, approximately equal to 30% of the Fortune 500

Tax credit additions and modifications

A significant number of provisions add or enhance credits and incentives that pertain to domestic research and green energy initiatives. Noteworthy changes include:

Increased small business payroll tax credits for research activities:

Qualified payroll tax credit for increasing research activities raised from $250,000 to $500,000

First $250,000 will be applied against the FICA payroll tax liability. Second $250,000 will be applied against the employer portion of Medicare payroll tax.

Applies for taxable years beginning after December 31, 2022

Limited to tax imposed for calendar quarter with unused amounts being carried forward

Qualifying small businesses are required to have less than $5 million in gross receipts in current year and no gross receipts prior to the 5 year period ending with the current year

Green initiative tax credits and incentives:

Credits for purchasing new and previously-owned clean vehicles

Extension of IRC Sec. 45L – New Energy Efficient Home Credit – extended to qualified new energy efficient homes acquired before January 1, 2033. Increase value of available credit for single-family homes to $2,500 and modified the credit available for multi-family homes.

Extension, increase, and modifications to IRC Sec. 25C nonbusiness energy property credit

Extension and modification of IRC Sec. 25D residential clean energy credit

IRC Sec. 48 energy credit for businesses and investors

Expansion of qualifying property, extension of credit including phasedown and phaseout rules, and introduction of incentives

Credit for producing energy from renewable sources (IRC Sec. 45)

Retroactive for facilities placed in service after December 31, 2021

Extends beginning of construction deadline to projects beginning construction before January 1, 2025 including solar energy facilities

Increased energy credit for solar and wind facilities in certain low-income communities

New credit for clean hydrogen production

New credit for zero-emission nuclear power

Extension of incentives for biodiesel, renewal diesel, and alternative fuels

Extension of biofuel producer credit

New income and excise tax credits allowed for sustainable aviation fuel

Modification of IRC Sec. 179D – Energy Efficient Commercial Buildings Deductions

Modification of building qualifications

Deduction increased from $1.88 per square foot to up to $5 per qualified square foot

Changes in depreciation for certain green energy properties

Final thoughts

The Inflation Reduction Act should have wide-ranging impacts on taxpayers, especially large corporations and high-net-worth individuals. In the coming weeks our tax leaders will dive into the specifics of the legislation, outline immediate and long-term impacts, and provide tax-planning strategies and considerations.