Utilizing IC-DISCs is a savvy strategy for U.S. wineries aiming to expand internationally, offering significant tax benefits, and supporting cash flow management.

Successful international expansion requires understanding and navigating local regulations and choosing the appropriate business structure or appropriate method of entering a foreign market that will sustain company growth and provide necessary flexibility.

Advanced technologies and innovative practices can help wineries enhance production efficiency, market analysis, and intellectual property management.

~

You have invested time, energy, and meticulous care into crafting your wine. As a result, you have steadily increased your brand recognition and revenue. With a solid domestic footprint in place, you start the process of building your international presence.

That’s when you run into some new challenges: Cost. Compliance. Taxes. Understanding the complexities of structuring your business and strategic tax planning are crucial as your winery expands its reach to a larger global and more diverse audience.

To get the most from your winery’s international expansion, here are four key strategies to keep in mind:

1. Decreasing Your Tax Burden on International Sales

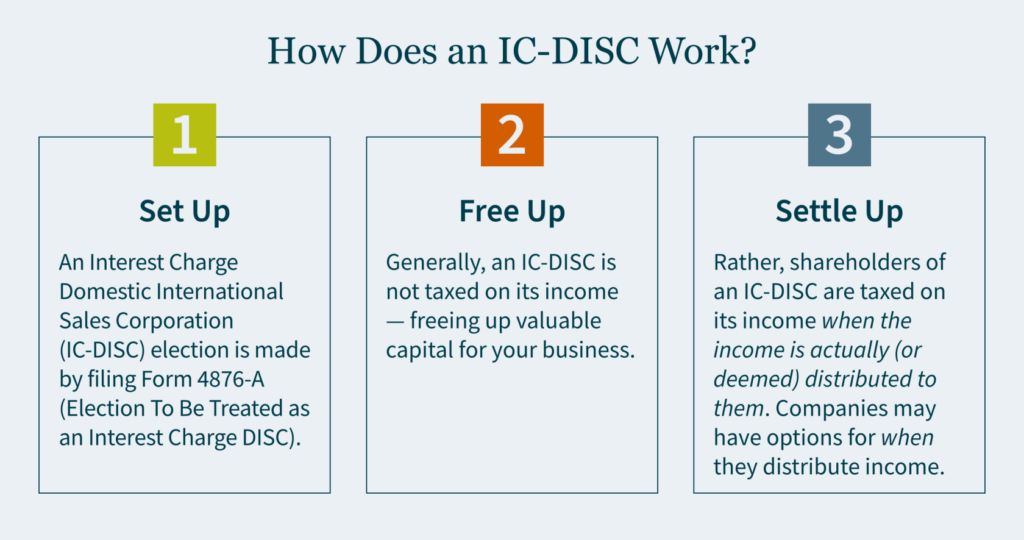

One of the primary considerations for wineries expanding internationally is the strategic formation of an IC-DISC (Interest Charge Domestic International Sales Corporation). This tax vehicle can significantly benefit U.S. exporters by reducing tax burdens on export income. By establishing an IC-DISC, your winery can enjoy deferred tax payments and lower rates on dividend distributions, which are vital for managing cash flow and reinvesting in growth.

Wineries with substantial international sales should consider an IC-DISC strategy. While the setup involves initial costs and compliance, the long-term tax savings make it an attractive option. Careful planning and advice from tax professionals with specific knowledge of the wine industry can help you maximize the benefits.

2. Navigating International Compliance and Business Structuring

Expanding into international markets requires more than just tax planning — it demands a comprehensive understanding of the local compliance and business environments. Your winery must adhere to various regulations, from local business laws to specific wine industry standards, which can differ significantly by country.

Choosing the appropriate business structure or method of entering a foreign market is pivotal. Whether establishing a direct presence through subsidiaries or leveraging partnerships, your winery must assess its operational scale and strategic goals. For smaller wineries, direct export might be feasible. Larger operations might benefit from a more established local presence, which can facilitate deeper market penetration and brand recognition.

3. Leveraging Technology and Innovation

Incorporating technology and innovation has become an increasingly important competitive advantage in the wine industry. From production techniques to supply chain management, technology can streamline your operations and enhance quality control across borders.

Advancements such as artificial intelligence (AI) offer new ways to analyze market trends and consumer preferences, enabling wineries to adapt strategies dynamically. For instance, AI is transforming the way sommeliers select and pair wines. Additionally, AI-powered systems can examine the chemical and sensory attributes of wines, recommending ideal conditions and components to achieve a specific flavor profile. This leads to time savings, minimizes waste, and provides winemakers the flexibility to explore novel mixtures and styles.

The use of AI and Generative AI (GAI) in wine inventory, selection, and pairings is growing increasingly popular. Companies that consider how to capture these business processes — and do so tax efficiently — may reap the rewards of increased profitability.

4. Building a Responsive and Agile Business Model

For wineries operating internationally, quickly adapting to new opportunities and challenges is critical. This includes being responsive to market demands, regulatory changes, and competitive pressures. Developing an agile business model allows for rapid adaptation and decision-making, enabling you to take advantage of emerging trends and mitigate potential risks.

Tax and accounting firms can assist wineries in building responsive models that quickly adapt to market demands and regulatory changes. In addition, helping wineries know when and how to upscale from one operating model to another is often critical. Strategic advisory services can help your winery anticipate shifts in the international landscape and adjust your strategy effectively, reducing risks and capitalizing on new opportunities.

Taking Your Winery to the World Stage

For wineries looking to expand internationally, a strategic approach to tax planning, compliance, and business structuring is essential. By leveraging tax strategies like IC-DISCs, ensuring compliance with local regulations, adopting innovative technologies, and developing an agile business model, you can enhance your competitiveness and position your wine for growth in the global marketplace.

How MGO Can Help

MGO can provide your winery with guidance on setting up an IC-DISC. Our tax professionals are well-versed in the complexities of international tax law, helping you enhance tax savings and manage compliance risks. Our team can also advise you on optimal business structures, market entry strategies like importing or licensing, and adherence to international standards.

With our global reach and local knowledge, MGO equips your winery with the insights needed to establish and maintain a compliant international presence. Reach out to our team today to learn more.

The potential rescheduling of cannabis presents an opportunity to reevaluate your company’s tax structure and increase deductions, reduce income, and simplify accounting.

Rescheduling may open up access to previously unavailable tax credits, incentives, and deductions at various government levels.

With anticipated increased investment and cash flow after rescheduling, companies should prepare for potential mergers and acquisitions by seeking support in areas like financial due diligence and post-acquisition planning.

~

The rescheduling of cannabis from Schedule I to Schedule III will unlock new opportunities for cannabis businesses. Is your company positioned to capitalize?

Tax Restructuring

If your existing operating structure was optimized for Section 280E mitigation, now is the time to evaluate whether it will still be tax-efficient after rescheduling.

MGO’s dedicated cannabis tax team can analyze your current structure and identify opportunities to increase deductions, reduce income, simplify accounting, and eliminate unnecessary tax exposures. We will help you develop a strategy specific to your business needs that aligns with your operational goals and any regulatory considerations.

Tax Credits, Incentives, and Deductions

Rescheduling should open cannabis operators to a world of previously unavailable tax benefits.

Our tax professionals can comprehensively review your business operations to uncover tax credits, incentives, and deductions that you may qualify for at the federal, state, and local levels.

Financial and Internal Control Audits

While rescheduling will eliminate the Section 280E tax burden and attract new investors to the cannabis industry, it could also lead to a new regulatory framework.

Our audit services can provide assurance to investors that your company is effectively managing risks, complying with any regulatory changes, and maintaining transparency.

Mergers and Acquisitions (M&A)

The projected wave of investment and increased cash flow resulting from rescheduling means more M&A should be on the horizon.

If your company is considering an M&A deal (either as a buyer or seller), MGO can support your efforts with structuring, financial & tax due diligence, Quality of Earnings (QoE) assessments, accounting integration, strategic guidance, and post-acquisition planning.

In April 2023, the U.S. Tax Court made news when it ruled in favor of businessman Alon Farhy, who challenged the Internal Revenue Service (IRS)’s authority to assess penalties for the failure to file IRS Form 5471.

IRS Form 5471 is the Information Return of U.S. Persons With Respect to Certain Foreign Corporations.

In May 2024, the U.S. Court of Appeals for the D.C Circuit reversed the Tax Court’s initial ruling — underscoring the significance of context in assessing penalties for international information returns.

~

UPDATE (May 2024):

Recent developments in the Farhy v. Commissioner case have captured significant attention in the tax and legal sectors. On May 3, 2024, the U.S. Court of Appeals reversed the Tax Court’s initial decision, highlighting the importance of statutory context in penalty assessments for international information returns. This ruling emphasizes the need for a closer examination of statutory language, altering perspectives on penalty applicability for non-compliance.

The implications of this case extend to taxpayers and practitioners, as detailed in analyses by MGO (see below). The decision underscores the need for meticulous compliance practices and adept navigation of the complexities of U.S. international tax law, along with a deep understanding of judicial interpretations of tax regulations.

MGO’s professionals are well-positioned to assist clients in navigating the complexities arising from the recent Farhy v. Commissioner decision. With a comprehensive understanding of the changing landscape in penalty assessments for international information returns, we provide guidance to help companies adapt to new judicial interpretations and maintain compliance with evolving tax regulations.

ORIGINAL ARTICLE (published June 8, 2023):

On April 3, 2023, the U.S. Tax Court came to a decision in the case Farhy v. Commissioner, ruling that the Internal Revenue Service (IRS) does not have the statutory authority to assess penalties for the failure to file IRS Form 5471, or the Information Return of U.S. Persons With Respect to Certain Foreign Corporations, against taxpayers. It also ruled that the IRS cannot administratively collect such penalties via levy.

Now that the IRS doesn’t have the authority to assess certain foreign information return penalties according to the court, affected taxpayers may want to file protective refund claims, even if the case goes to appeals — especially given the short statute of limitations of two years for claiming refunds.

Our Tax Controversy team breaks down the Farhy case, as well as what it may mean for your international filings — and the future of the IRS’s penalty collections.

The IRS Case Against Farhy

Alon Farhy owned 100% of a Belize corporation from 2003 until 2010, as well as 100% of another Belize corporation from 2005 until 2010. He admitted he participated in an illegal scheme to reduce his income tax and gained immunity from prosecution. However, throughout the time of his ownership of these two companies, he was required to file IRS Forms 5471 for both — but he didn’t.

The IRS then mailed him a notice in February 2016, alerting him of his failure to file. He still didn’t file, and in November 2018, he assessed $10,000 per failure to file, per year — plus a continuation penalty of $50,000 for each year he failed to file. The IRS determined his failures to file were deliberate, and so the penalties were met with the appropriate approval within the IRS.

Farhy didn’t dispute he didn’t file. He also didn’t deny he failed to pay. Instead, he challenged the IRS’s legal authority to assess IRC section 6038 penalties.

The Tax Court’s Initial Ruling

The U.S. Tax Court then held that Congress authorized the assessment for a variety of penalties — namely, those found in subchapter B of chapter 68 of subtitle F — but not for those penalties under IRC sections 6038(b)(1) and (2), which apply to Form 5471. Because these penalties were not assessable, the court decided the IRS was prohibited from proceeding with collection, and the only way the IRS can pursue collection of the taxpayer’s penalties was by 28 U.S.C. Sec. 2461(a) — which allows recovery of any penalty by civil court action.

How This Decision Affects Your International Penalty Assessments

This case holds that the IRS may not assess penalties under IRC section 6038(b), or failure to file IRS Form 5471. The case’s ruling doesn’t mean you don’t have an obligation to file IRS Form 5471 — or any other required form.

Ultimately, this decision is expected to have a broad reach and will affect most IRS Form 5471 filers, namely category 1, 4, and 5 filers (but not category 2 and 3 filers, who are subject to penalties under IRC section 6679).

However, the case’s impact could permeate even deeper. For years, some practitioners have spoken out against the IRS’s systemic assessment of international information return (IIR) penalties after a return is filed late, making it impossible for taxpayers to avoid deficiency procedures. The court’s decision now reveals how a taxpayer can be protected by the judicial branch when something is deemed unfair. Farhy took a stand, challenged the system, and won — opening the door for potential challenges in the future.

It’s uncertain as to whether the IRS will appeal the court’s decision. But it seems as though the stakes are too high for the IRS not to appeal. While we don’t know what will happen, a former IRS official has stated he expects that, for cases currently pending review by IRS Appeals, Farhy will not be viewed as controlling law yet.

The impact of the ruling is clear and will most likely impact many taxpayers who are contesting — or who have already paid — IRC 6038 penalties. It may also affect other civil penalties where Congress has not prescribed the method of assessment in the future.

How You Should Respond to the Court’s Decision

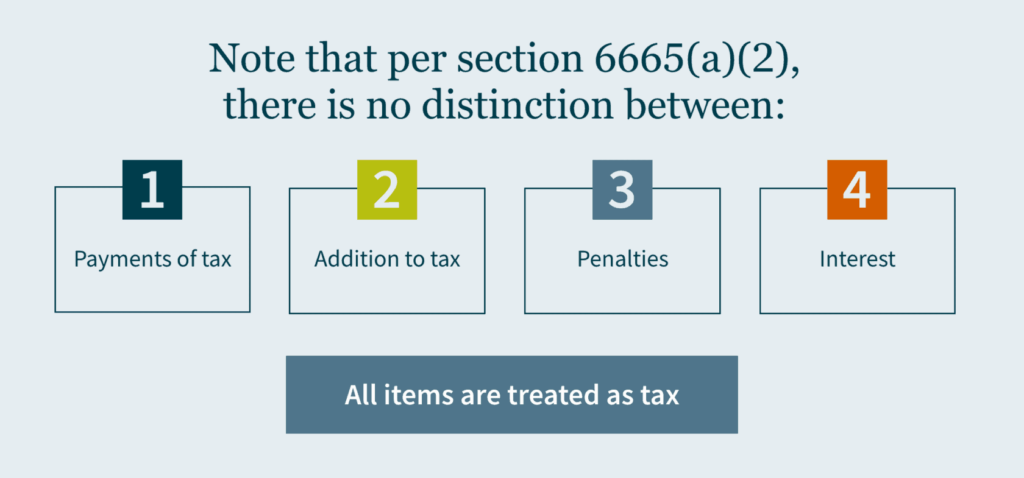

You should move quickly to take advantage of the court’s decision, as there is a two-year statute of limitations from the time a tax is paid to make a protective claim for a refund. It’s likely this legislation wouldn’t affect refund claims since that would be governed by the law that existed when the penalties were assessed. Note that per IRC section 6665(a)(2), there is no distinction between payments of tax, addition to tax, penalties, or interest — so all items are treated as tax.

If you’ve previously paid the $10,000 penalty, it’s important to file your protective claim now, unless you’ve entered into an agreement with the IRS to extend the statute of limitations, which can occur during an examination. Requesting a refund won’t ever hurt, but some practitioners believe the IRS may try to keep any penalty money it collected, even if the assessment is invalid — because, in its eyes, the claim may not be. Just know, you can file your protective claim for a refund, but may not get it (at least not any time soon).

The Farhy decision could likewise be applied to other US IRS forms, such as 5472, 8865, 8938, 926, 8858, 8854. Some argue the Farhy decision may also be applied to IRS Form 3520.

How MGO Can Help

Only time will tell if the court’s decision will open the government up to additional criticisms for other penalty assessments. If you have paid your penalties and are wondering what your current options are, MGO’s experienced International Tax team can help you determine if you’re eligible to file a refund claim.

Orphan drug credits offer a significant tax incentive to encourage pharmaceutical companies to develop treatments for rare diseases.

The tax credit is worth up to 25% of qualified clinical testing expenses.

It is possible for companies to claim both R&D and orphan drug credits in the same tax year, maximizing support for a broad range of medical research.

~

Developing new pharmaceuticals and bringing them to market is an expensive endeavor. Uncommon diseases and conditions, often called “orphan diseases,” affect small populations in the United States. Given the high costs of research and development (R&D), this limited patient base can make treatment development less economically attractive for pharmaceutical companies.

Congress passed the Orphan Drug Credit (IRC Section 45C) to address this challenge and encourage the development of treatments for less profitable drug therapies.

What Is the Orphan Drug Tax Credit?

The Orphan Drug Credit is a federal tax credit designed to encourage pharmaceutical companies to invest in the research and development of treatments, cures, and preventive measures for rare diseases or conditions.

Before the Orphan Drug Act was enacted in 1983, life sciences companies often hesitated to invest in development costs for rare diseases because the small populations of potential patients made it difficult to recover development costs.

If your testing qualifies, the nonrefundable tax credit equals 25% of qualified clinical testing expenses (QCTEs) for the current taxable year.

In general, you can claim the credit between the date the U.S. Food and Drug Administration (FDA) grants the orphan drug designation and the date it approves the drug for patients.

Orphan Drug Tax Credit Eligibility Criteria

To qualify for the Orphan Drug Credit, you must first receive an orphan drug designation from the FDA. This designation is granted to drugs intended for the treatment, diagnosis, or prevention of diseases or conditions that affect fewer than 200,000 people in the United States or that affect more than 200,000 people but are not expected to recover the costs of developing and marketing a treatment drug.

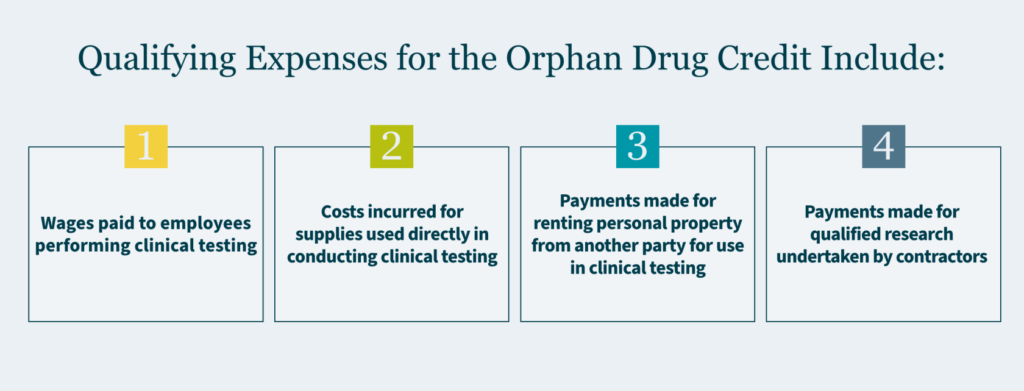

Once receiving the orphan designation, you can deduct 25% of qualified clinical testing expenses incurred in the U.S.

Wages paid to employees performing clinical testing

Costs incurred for supplies used directly in conducting clinical testing

Payments made to another party for computer hosting and leasing pertaining to clinical testing activities

Payments made for qualified research undertaken by contractors

Research activities funded by a government entity or another entity other than the taxpayer do not qualify for the tax credit.

Orphan Drug Tax Credits vs. R&D Tax Credits

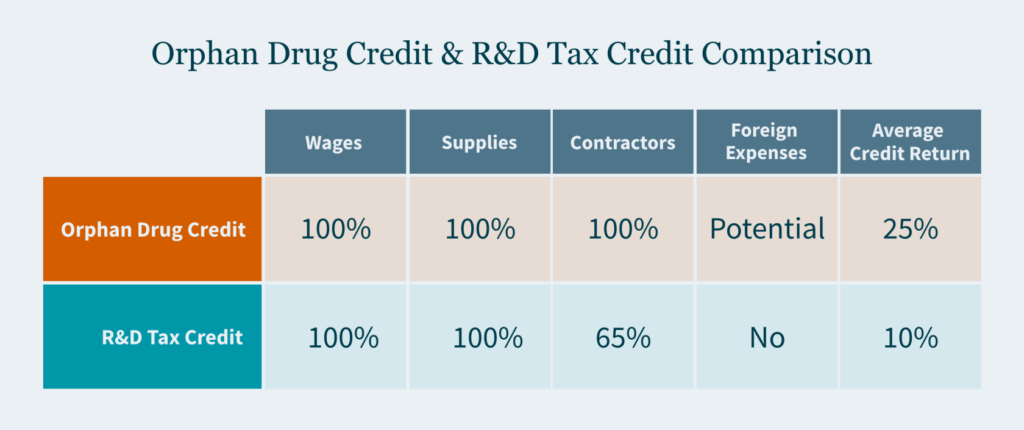

The Orphan Drug Credit and the R&D credit (IRC Section 41) offer substantial financial incentives to spur U.S.-based research. However, the Orphan Drug Credit provides a greater incentive than the R&D credit.

If you are researching non-orphan diseases, you can claim the standard R&D credit, which on average results in an overall credit benefit of roughly 10% of the qualified expenses.

Other benefits of the Orphan Drug Credit include claiming 100% of qualified contract research expenses, compared to 65% under the R&D credit, and claiming the credit on foreign clinical testing expenses provided the testing meets certain criteria. The criteria include:

The testing is conducted outside the United States because there is an insufficient testing population within the U.S., and

Ideally, you can claim the Orphan Drug credit on qualified clinical testing expenses until the FDA approves your drug for patients, then claim the R&D credit for any ongoing qualified research expenses post-FDA approval.

Is it possible to claim both the R&D credit and the Orphan Drug Tax Credit in the same tax year?

Yes, you can claim both credits in the same tax year, provided you meet the eligibility criteria for each. However, the expenses used to claim the Orphan Drug Credit cannot also be used to claim the R&D credit. The return on investment is greater under the ODC, so a company with an eligible orphan drug designation would likely pursue the ODC credit pertaining to those expenses. A company may have expenses pertaining to a non-ODC program, or expenses incurred prior and post the ODC eligible timelines, that would benefit under the R&D credit.

How MGO Can Help

The Orphan Drug Credit provides significant incentives for pharmaceutical companies developing treatments for rare diseases, making these endeavors more financially viable.

As with any tax credit, the qualifications for claiming the Orphan Drug Credit are nuanced, and it’s critical to have the necessary documentation to calculate and substantiate your claim.

If you need help determining which expenses qualify, calculating your credit, or determining how it works in tandem with the R&D credit, call or contact MGO online today. We’re happy to help you identify potential qualified expenses and maximize the tax benefits of bringing these new drugs to market to treat rare diseases.

Agents and managers can help globally earning clients like professional athletes, musical artists, and entertainers strategically manage finances and taxes across borders to maximize earnings.

For U.S. citizens and residents earning money abroad, key areas for advisors to address include endorsement deals, royalties, foreign properties, foreign tax returns, and tax structuring that considers foreign investments.

For foreign (non-resident) athletes, artists, and entertainers performing in the U.S., considerations include but are not limited to U.S. taxable income, withholding rules, tax status, Central Withholding Agreements (CWA), and tax treaties.

~

As an agent or manager for athletes, artists, and entertainers, many of your clients likely earn income across borders as they perform worldwide. Strategically managing their finances and taxes is crucial to maximize earnings. Proper planning can help reduce tax burdens and avoid double taxation across jurisdictions. This allows your clients to focus on their careers while you may finesse your assistance to them in optimizing their income with guidance from tax professionals.

Understanding key tax considerations can enable you to put frameworks in place to mitigate your clients’ liabilities. For clients who are citizens or residents of the United States earning money abroad, all worldwide income must be reported to the IRS. However, foreign countries also tax income earned by non-residents. Assessing relevant tax treaties and structuring contracts in an appropriate manner can lead to more advantageous tax treatment.

When your clients have income from various sources both from inside and outside the United States, proactive tax planning is key. Common international income types to consider include:

Salaries from foreign leagues and tournaments

Performance fees from concerts and festivals

Royalties

Endorsements and sponsorships

Bonuses and prizes from international tournaments

Merchandise sales

Other income earned while playing or performing overseas

How these income types are classified and sourced impacts tax liabilities. Consulting tax professionals before your clients sign any deals allows for upfront planning that can keep more money in your clients’ pockets.

5 Key Considerations for U.S.-Based Athletes, Artists, and Entertainers Earning Income Abroad

If you are an advisor to musical artists, professional athletes, film actors, or other performers who are U.S. citizens, residents, or green card holders with foreign income sources, here are five important areas to address:

Endorsement Deals – How will the construction of a contract impact tax treatment abroad? Will the income be considered U.S. or foreign sourced? What are some ways to proactively plan for potential tax savings?

Royalties – Can royalties be classified differently if content is published while clients are abroad? How are royalties affected by collaborations with international artists? Is it considered U.S. income if royalties are received while playing or performing abroad?

Foreign Properties – What are the tax rules surrounding your clients purchasing or renting homes abroad (rules may vary by country)? Did you know that foreign rental income may need to be disclosed on a U.S. tax return? How do investments in foreign countries get reported and taxed?

Foreign Tax Returns – When is return filing required for extended stays abroad? Can foreign taxes be credited (and is the credit dollar-for-dollar)? What should be expected for payments received as a contractor versus as an employee? Which expenses are deductible in each country? For example, are agent fees, travel expenses, and entertainment deductible?

Foreign Tax Structuring – Is it better to withhold taxes on gross revenues or after deductible expenses? How do local, state, and regional (provincial, cantonal, district, county) taxes factor in?

With these areas addressed upfront, you can maximize income and minimize overall tax burdens for your clients as opportunities arise.

5 Top Considerations for Foreign Domiciled Athletes, Artists, and Entertainers Performing or Playing in the U.S.

If you are an advisor to athlete, artist, and entertainer clients who are not residents or citizens of the U.S. but earn income in this country, areas that could have an impact on your clients’ taxes include (but are not limited to):

U.S. Taxable Income – Is U.S.-sourced income taxable? What types of income may this include? Is there a requirement to file a U.S. federal income tax return? Is there an income threshold that must be met?

Withholding Rules – What are the withholding rules surrounding payments to foreign athletes, artists, and entertainers?

U.S. Tax Status – How is U.S. tax status determined — residency for income tax and domicile for transfer tax? How is taxation affected with or without a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN)?

Tax Treaties – Does the individual’s home country have a tax treaty with the U.S.? How does it impact tax liabilities?

Evaluating options surrounding tax statuses, withholding approaches, and applicable treaties can mitigate liabilities and optimize tax treatment for your foreign clients.

Work with Tax Professionals to Help Your Clients Maximize Global Income

As an agent or manager navigating global income for your clients, working with experienced tax professionals is key. Advisors can assess your clients’ situations across jurisdictions to put frameworks in place reducing liabilities and avoiding double taxation. With the right global tax strategy tailored to each client, you can position them to pursue worldwide career opportunities with maximum income and minimum taxes.

State tax authorities are escalating audits of intercompany transactions, as transfer pricing crackdowns in several states are generating millions in tax revenue.

These state initiatives indicate growing regulatory emphasis on transfer pricing, which may encourage more aggressive audits (especially if budgets tighten).

Companies operating across state borders should take proactive steps, like conducting transfer pricing studies to validate policies and strengthen defenses before audits strike.

~

A recent Bloomberg article affirms state tax authorities are ramping up audits of intercompany transactions at multistate corporations. The report points to an increase in audits in three “separate-reporting” states following transfer pricing settlement initiatives as a beacon of audit activity to come across other states that take this approach.

While not ideal for multistate operators, this development may not come as a surprise to companies with international operations who have dealt with a myriad of cross-border tax issues in recent years. Close observers of state and local tax (SALT) developments have been predicting for many years the potential that states will be adopting similar positions with respect to transfer pricing. In a 2022 article focused on SALT transfer pricing enforcement, we highlighted several key indicators that more state transfer pricing audits could be on the horizon – including state budget deficits, a surge in auditor and consultant hirings, and renewed interest among states in collaborating on multistate audits.

With confirmation that state-driven transfer pricing audits are on the rise, it is imperative for corporations operating across state borders to assess your transfer pricing risks and fortify your documentation and audit defense strategies.

Surge of Transfer Pricing Audits in Separate-Reporting States

According to the Bloomberg Tax report, the recent spike in transfer pricing audit activity has predominantly affected Southeastern states categorized as separate-reporting states. Currently, there are 17 separate-reporting states in the United States. With the exception of a handful of states like Indiana, Pennsylvania, Iowa, and Delaware, most separate-reporting states are located in the Southeast region.

How separate-reporting states differ from other states in their taxation approach to corporations:

In separate-reporting states, each corporation within an affiliated group is required to file its individual tax return. This treatment considers them as separate entities with independent income, recognizing intercompany transactions, and allowing for varying tax liabilities.

In contrast, combined-reporting states require or allow affiliated corporations within a corporate group to file a single tax return, treating them as a unitary business with shared income, often eliminating intercompany transactions.

Notably, two Southeastern states, Louisiana and North Carolina, have recently concluded audit resolution programs that significantly boosted their state revenues. Louisiana’s program generated nearly $38 million, while North Carolina’s efforts resulted in more than $124 million. Meanwhile, New Jersey, a Mid-Atlantic state that abandoned separate reporting in favor of combined reporting in 2019, is in the midst of a transfer pricing resolution program that has already collected almost $30 million. The success of these programs in collecting tax revenue is likely to motivate other states to explore similar initiatives.

The success and subsequent expansion of these programs signify a growing emphasis on transfer pricing at the state tax authority level. State tax agencies are enhancing their knowledge and enforcement activities in this domain, giving auditors more confidence to adjust returns in transfer pricing disputes. This increasing competency may be viewed as a valuable tool by states – both those requiring separate and combined reporting – that are seeking ways to augment revenue streams.

Strengthen Your Transfer Pricing Defenses Before State Audits Strike

To preemptively safeguard your business from a state transfer pricing audit, a proactive approach to validating pricing policies is essential – and a comprehensive transfer pricing study is your primary defense.

Here are three key advantages of conducting a transfer pricing study:

Document Your Transfer Pricing Policy: A transfer pricing study provides robust documentation that can counter inflated tax assessments by identifying key intercompany transactions, referencing benchmark data, and highlighting any deviations that necessitate policy adjustments. Even if your company has undertaken prior studies, annual updates are indispensable to align with evolving business landscapes and provide tax penalty protection.

Mitigate Your Risk: Beyond reducing audit risks and potential liabilities, these studies also play a pivotal role in supporting major corporate events like mergers and acquisitions (M&A). By demonstrating pricing compliance, they ensure that domestic affiliates have robust documentation and effective cost allocation analysis, thus preventing over-taxation or under-taxation.

Ensure Consistency: Minimize uncertainty by achieving uniform entity-specific compensation across state agencies and affiliated entities. Swift collaboration with advisors when audits arise enhances dispute resolution capabilities.

As states continue to gain confidence in challenging transfer pricing, multistate corporations must take proactive measures to ensure the resilience of their intercompany transactions under intensified scrutiny.

Get Ahead of the Game with a Transfer Pricing Study

If your company engages in substantial intercompany transactions across state lines, initiating a review of your current pricing policies, preparing your transfer pricing policies, and ensuring compliance with U.S. transfer pricing rules should be a top priority. Proactive measures can help you stay ahead of potential issues before state auditors come knocking. We have a robust transfer pricing team that works closely with our State and Local (SALT) Tax and Tax Controversy practices. Through a combined effort we can support you through every stage of managing a transfer pricing audit. Talk to our transfer pricing professionals today to find out how we can help you minimize your exposure to transfer pricing audits.

The world of wineries and vineyards is a harmonious blend of tradition, innovation, and meticulous craftmanship. As California grapes transform into wines that delight consumers across the globe, another transformation process is unfolding behind the scenes: one that involves intricate tax considerations like transition planning, international exporting, and proactive tax planning strategies.

In this overview, our International Tax and Private Client Services teams “uncork” the complexities of tax issues that permeate the winery and vineyard industry so you can seamlessly confront tax challenges and seize tax opportunities. As financial landscapes continue to evolve, understanding these challenges becomes essential for vineyard owners, winemakers, and investors alike in their pursuit of crafting both exquisite wines and sustainable financial success. And as some new seasons start, others come to an end. When the time comes to transition the business, you will likely want a seasoned professional to guide you through.

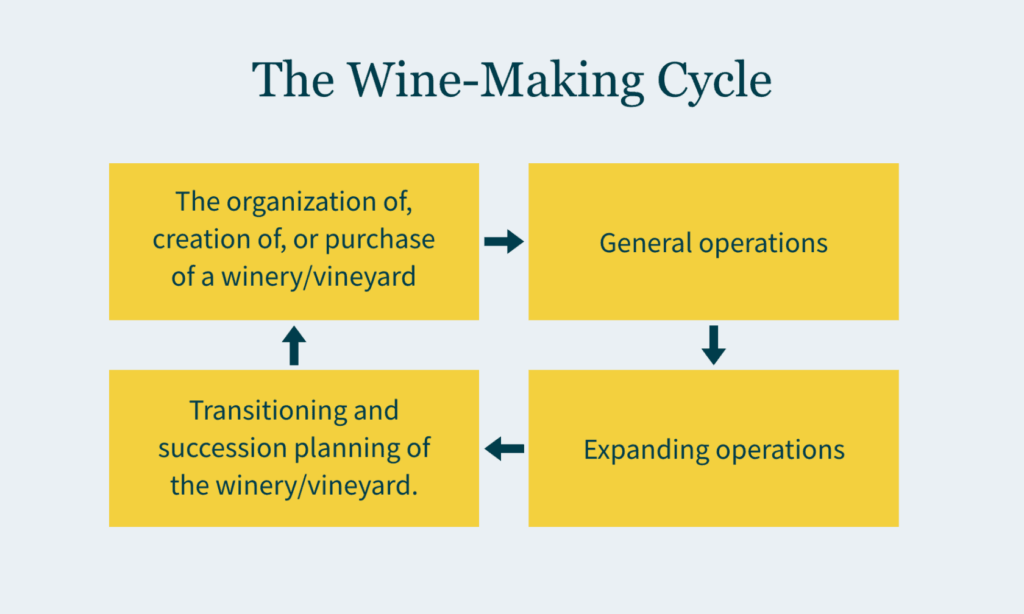

The wine-making cycle

Generally, a vineyard or winery has a business cycle that may take various courses but the course we see most commonly goes as follows:

Organization / Creation / Purchase

The creation of the organization generally entails the creation of an appropriate legal entity. Whether this act should be taxable or not will depend on the tax attributes of the potential owners and should be reviewed to position the organization optimally for taxing purposes.

The purchase of an existing winery or vineyard should be structured in a tax efficient manner such that future depreciation and deductions are maximized for the purchaser. Typically, the maximization of deductions will be at odds with what a seller would desire, so the final decision will stem from negotiations between both the buyer(s) and seller(s). Ultimately, a good due diligence exercise is always warranted in these situations.

Operations

Both metaphorically and physically, the seasons always present themselves with a new beginning for the industry.

There are many ways to operate a winery or vineyard. You may start with raw land—and then have vines, or not. Rocky soil and warm temperatures provide an excellent environment for grapes to make Cabernet Sauvignon, for example. Cooler microclimates and sandier soil offer great growing conditions for Sauvignon Blanc. A vineyard manager may want to “test” some of the grounds and only plant a smaller portion of the plot.

When planting a new crop, it can sometimes take up to three years before a vine produces viable grapes. Veraison is that magical moment when those hard, green grapes transform into plump, juicy clusters. In white grapes, such as those used for Sauvignon Blanc and Chardonnay, the clusters turn from bright green to a more mellow, golden green.

Once your grapes are ready, one may harvest and then crush, press, and start the primary fermentation process. Then the aging and malolactic fermentation sets in. Towards the end of the aging process, winemakers will frequently taste the wine to ensure the flavors are just right. They do this with a “wine thief,” or a special tool that extracts a small amount of wine from the container it is aging in. This is commonly referred to as racking and bottling. Once the process is complete, then one obtains the finished bottle.

Having an appropriate cost accounting system is crucial to tracking the costs that are attributed to each step in the process — and will be the cornerstone to any tax planning you will want to implement.

Having an appropriate cost accounting system should help track the costs that are attributed at each step of the way.

Some of the tax implications that should be considered are provided below.

Qualifying for R&D tax credits

Archaeological records insinuate that wine was first produced in China around 7000 B.C., with the oldest winery in the world in Armenia. So, it’s no secret that wine making has been around for a long time. However, this doesn’t mean winery owners can’t and don’t implement new technologies or approaches to making their cultivation and fermentation methods more innovatively efficient.

And many in the industry do not claim the Research and Development (R&D) tax credit, failing to realize their research activities actually fall into the qualifying research activity (QRA) category. In fact, many daily activities you may already conduct — as well as wages paid to your employees involved in these activities — can qualify.

R&D tax credits enable your business to apply for a dollar-for-dollar reduction of your tax applied to any qualified research and development expenditures you may have. In some circumstances, these credits can be applied against payroll taxes as well. These can provide significant value to your organization, as it provides reduced tax liability and cash back so you can reinvest or apply to other needs. Companies of all sizes are eligible — and the tax definition of “qualified research” is broader than you might think, covering more than research that takes place in a lab. If you develop new or improved products, processes, and/or software to use in your operations, you could be eligible for technologically advancing the industry.

Whether it’s making unique improvements to products already available on the market or inventing something completely new, if you demonstrate you’ve experimented to resolve technological uncertainties and tackle challenges that are new to you, you could qualify. This includes new or improved beverages. The best part? You don’t have to actually achieve your goals in order to qualify.

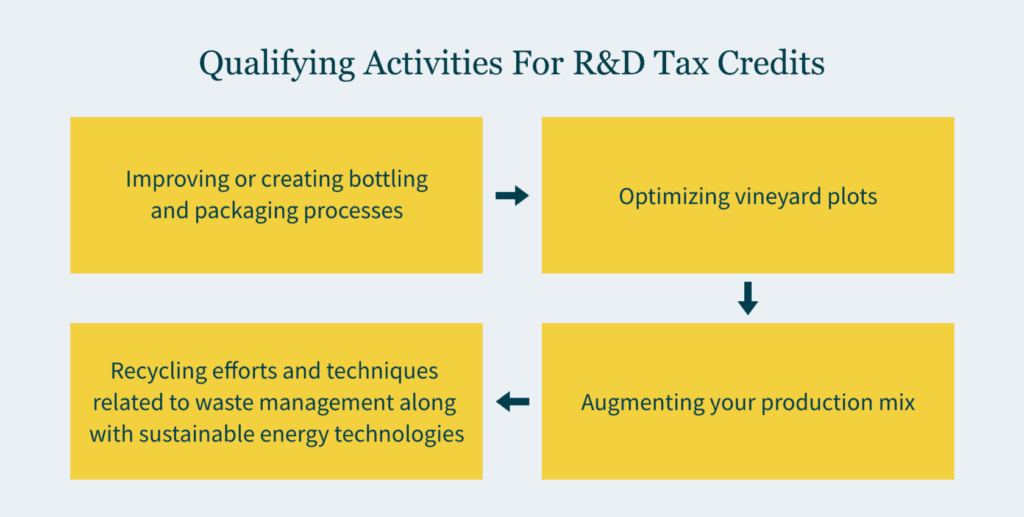

Examples of qualifying activities

Improving or creating bottling and packaging processes.

This includes bottle labeling or equipment, corks, and methods to improve filtration and shelf life. This could include new packaging designs to improve shelf life.

Optimizing vineyard plots.

This can mean evaluating soil, water availability, and ground slopes for optimal grape cultivation; soil and rootstock process improvement; plant irrigation system development; and trellis improvements.

Augmenting your production mix.

This can include evaluating conditions that affect winemaking like humidity, lighting, and ventilation in your barrels; developing product formulations; experimenting with new combinations for unique flavors; creating new aroma/flavor profiles and ingredient mixing methodologies; experimenting with prototype batches and preservative chemicals; developing new fermenting techniques; developing or refining press-fraction, press-yield or other crush or press trials; etc.

Recycling efforts and techniques related to waste management along with sustainable energy technologies.

Fixed assets — i.e., property, plant, and equipment involved in your winemaking — can prove a powerful tax savings tool if you manage them correctly as well as increase your cash flow, so you can reinvest the savings or hold onto them to endure an uneven or less fruitful year.

Some of the tax opportunities you can capitalize on in the wine industry include:

Reducing your current-year tax liabilities,

Increasing your current-year cash flow, and

Deferring your tax liabilities to later years.

Depreciated assets are one area you might overlook. Because wine production requires a significant amount of equipment you might not think about initially (like infrastructure and process-related electrical and plumbing hookups in your facility), you can count them in the total share of your property’s acquisition or constructed cost. The higher the percentage in assets available for shorter recovery periods, the more tax deferral opportunities you may have. Careful categorizing of assets between personal property v. real property can mean a substantial difference in tax benefit including amount and timing in a given year.

If you have implemented ways to make your winery more environmentally friendly, you may also capitalize on energy efficiency incentives. With an intensifying focus on environmental, social, and governance (ESG) permeating more industries, you can take advantage of available credits and deductions, which are measured against your facility’s ability to utilize alternative power systems (like solar energy) or the installation of energy efficient heating, ventilation, air condition, and lighting.

American viticulture areas

When you first purchase a vineyard, you have the option of acquiring an American Viticulture Area (AVA) intangible asset, whose value is recovered over 15 years through amortization. This provides annual deductions that lower your taxable income — a beneficial opportunity as it shifts the value out of the land that is normally not able to be depreciated.

Didn’t measure an AVA intangible when you bought your vineyard? That’s okay. An AVCA valuation can be performed — and any missed amortization deductions will be taken out from your application year.

Once the domestic tax planning is well oiled, some wineries and vineyards decide to expand.

Expanding operations

Many owners tend to expand their domestic operations, or some even venture overseas. Going offshore presents its own diverse challenges, some of which are described below.

International tax challenges

Exporting your wine abroad is a huge step — and one that can yield significant brand recognition and financial gain. Navigating the challenges associated with crossing borders and marketing in foreign markets coupled with international tax can prove extremely complex for wineries and vineyards because tax regulations vary from country to country, significantly impacting your operations and profitability. The taxes one may need to contend will be beverage taxes, customs and duties, tariffs and income tax, to name a few.

First and foremost, it’s critical that you work directly with experienced tax professionals who are knowledgeable not only about the area where your vineyard is located but also about the laws in the countries where you are exporting to. They can help you remain compliant amid the many seemingly convoluted challenges you face.

Because many countries have double taxation agreements (DTAs) to prevent the same income from being taxed twice, you should understand how these work between your home country and the countries you do business in. You certainly don’t want to be taxed twice!

Another way to successfully traverse these challenges is ensuring your transfer pricing practices are aligned with international guidelines. You’ll want your pricing transactions to remain fair between related entities to avoid tax evasion or an excessive tax burden in specific jurisdictions.

In general, it’s important to ensure you’re well versed in the tax laws of the countries you’re exporting to or operating in. That’s why a tax professional can come in handy. Different countries have different rules about importing, excise taxes, value-added taxes (VAT), and other forms of taxation that can majorly affect your business if you’re not complying.

This brings us to compliance with your reporting. Reporting all your international transactions and income is critical to avoiding penalties or legal issues. You’ll also need to consider any customs duties and tariffs, which may impact how successfully your wine competes in international markets. International tax regulations can change frequently at the hands of political, legal, or economic factors. Stay up to date on changes that could impact your business operations—or tax liabilities.

And just like the U.S. provides tax incentives, some countries do as well to encourage foreign investment and exportation. Your winery or vineyard could take advantage of these if they are available.

International tax compliance when exporting your wine can be complex. It also involves risk. Because every situation is different, you must tailor your approach based on the specific circumstances of your winery with advice from a professional knowledgeable in international tax. They can ensure you are adhering to the most updated regulations as well as maximizing your tax efficiency while remaining compliant.

From simply exporting abroad to setting up local in-country distribution operations we may assist by tailoring a strategy that best meshes with your company. A strategy many exporters use is an IC-DISC. The IC-DISC (Interest Charge-Domestic International Sales Corporation) is a federal income tax incentive for U.S. companies that may export their California wines outside of the United States. Domestic U.S. entities and sole proprietorships are eligible to receive this federal income tax savings. Our team may guide you as to whether an IC-DISC or other strategies are more suitable for you and your winery or vineyard.

Transition and succession planning

Whether you’re passing the business to the next generation or selling to a new owner, transition planning is crucial for taxes in the winery business, as it helps to ensure a smooth and successful transfer of ownership and management. However, transitioning a winery business involves complex financial transactions like asset transfers and potential restructuring. Tax efficiency is key to minimizing potential tax liabilities that could arise from poorly executed transfers. Here are some things to consider.

Minimizing your capital gains tax

Depending on if your winery has appreciated in value since its inception, transferring ownership can trigger capital gains tax. Strategizing the timing and structure of the transfer can potentially minimize these taxes through options like installment sales, gifting, or estate planning techniques. In fact, if the winery has been owned by a corporation, you might be able to sell your stock in that corporation with no taxable gains at all and/or rollover the gain into a new business, income tax free.

Navigating estate and gift tax considerations

Many wineries or vineyards are family affairs. If this is the case, you might face estate and gift tax implications. Taking advantage of exemptions and deductions can help you reduce the impact of estate and gift taxes.

Creating a smooth succession plan

Whether or not you’ve seen the popular show Succession, you know that sometimes, passing something as large as a corporation down to the next generation can cause some drama. That’s why succession planning is critical — it smooths the handover of management and ownership, which will help maintain your business’s stability and profitability. This can include a phased transition, training and development of successors, and establishing clear roles and responsibilities.

Optimizing your business structure

Different business structures have different tax implications. Knowing how to take advantage of your current structure’s tax efficiency and being open to changing it if that could prove advantageous before a transition occurs can pay dividends.

Assessing your value

Knowing the accurate value of your winery business is essential for tax purposes to calculate estate taxes or establish a fair selling price. Conducting a professional appraisal can ensure your business’s value is appropriately assessed.

Determining if you qualify for tax breaks

Some areas offer tax incentives for qualified business transfers, including reduced rates for capital gains taxes or other tax breaks. If you conduct transition planning, you can understand and leverage these applicable incentives.

Complying with tax laws and regulations.

Because tax laws and regulations can vary widely depending on where your winery or vineyard is located — not to mention they change over time — transition planning helps you stay aware of relevant tax regulations over the course of the transfer process, so you don’t incur penalties or legal issues.

Transition planning is a strategic process that analyzes the various tax implications that could affect a seamless and financially sound transition of ownership and management in your business. Tax professionals with experience in the wine industry can help you develop a transition plan tailored to your exact circumstances.

How we can help

Making and selling great wine is your top priority — which is why we’re here to help you navigate the tax challenges and seize the opportunities that can accompany following that passion. Our Private Client Services and International Tax teams are rooted in California, one of the most wine-centric regions in the world. We understand the nuances of your work while providing an external, holistic eye to help you grow and succeed. Contact us today.

The California Franchise Tax Board (FTB) recently announced a one-time penalty abatement program for California resident and non-resident individual taxpayers.

Here’s what you need to know to claim it:

It’s a one-time abatement of any “timeliness” penalties incurred on individual income tax returns (Form 540, Form 540NR, Form 540 2EZ) for tax years beginning on or after January 1, 2022.

It’s only available to individual taxpayers subject to personal income tax law (so estates, trusts, and fiduciaries aren’t eligible).

It can be requested verbally or in writing starting on April 17, 2023.

For California taxpayers who qualify for an extended 2022 income tax return due date because of the California Winter Storms (i.e., most California taxpayers), the “timeliness” penalties that would be abated through this program should not start being imposed until after the new extended due date for that tax year – October 16, 2023.

Which penalties are eligible?

Both the Failure to File Penalty (i.e., you did not file your tax return by the due date nor did you pay by the due date of your tax return) and the Failure to Pay Penalty (i.e., you did not pay the entire amount due by your payment due date) on California individual income tax returns for tax years beginning on or after January 1, 2022 are eligible for the one-time penalty abatement.

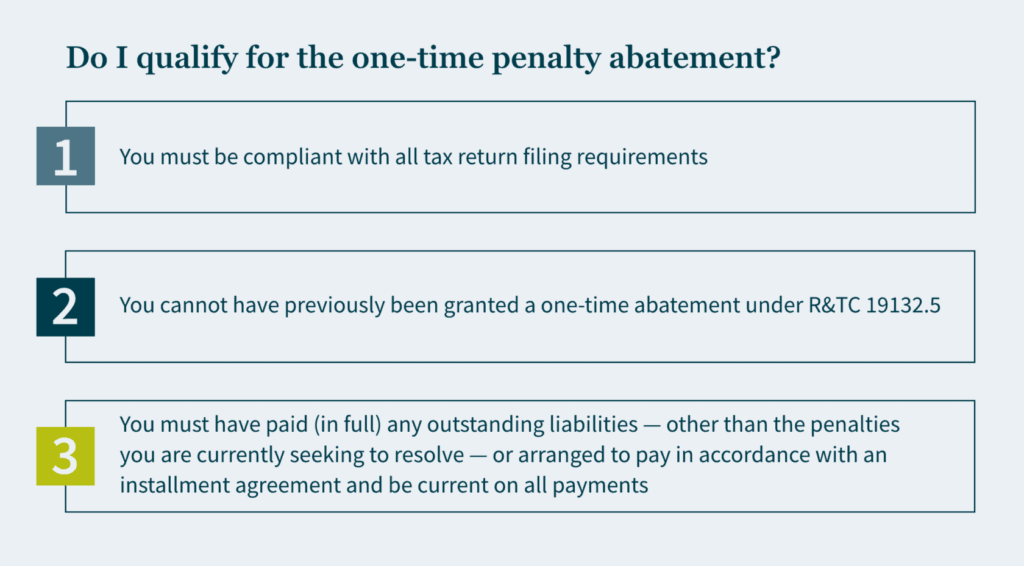

How do I qualify?

How do I request a one-time penalty abatement?

You can mail in a completed Form FTB 2918 or call the FTB at +1 (800) 689-4776 to request penalty abatement.

What if I can provide that I had reasonable cause for late filing or late payment?

If you can demonstrate that you exercised ordinary care and prudence and were nevertheless unable to file your return or pay your taxes on time, then you may qualify for penalty relief due to reasonable cause. Reasonable cause is determined on a case-by-case basis and considers all the facts of your situation.

You may request penalty abatement based on reasonable cause by mailing in a completed Form FTB 2917 or by filling out a reasonable cause request on your MyFTB online account. Penalty abatement based on reasonable cause may – depending on the circumstances – be preferable to using up your one-time penalty abatement request.

How we can help

If you need help with relief for your “timeliness” penalties or if you need help with any other state and local tax matters, please reach out to our experienced State and Local Tax team.

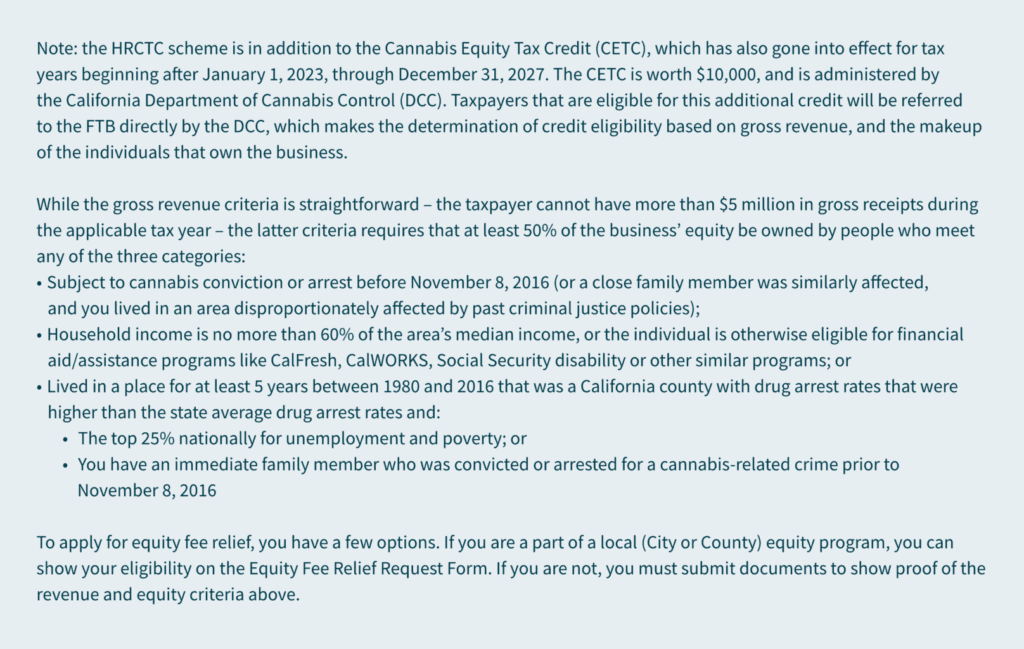

California now has a new tax credit called the High-Road Cannabis Tax Credit (HRCTC) available for eligible cannabis retailers and microbusinesses.

The credit is available for tax years starting after January 1, 2023, through December 31, 2027, and can be applied against current year (and future) income taxes.

To claim it, you must make a “tentative credit reservation.”

Expenditures that qualify include wages for full-time employees; safety-related equipment, training, and services; and workforce development and safety.

While the cannabis industry in California has been struggling on many levels, tax credit relief has come in the form of excise tax changes for distributors and has now arrived for retailers. The High-Road Cannabis Tax Credit is a new tax credit from the California Franchise Tax Board (FTB) available for cannabis retailers or microbusinesses for taxable years beginning January 1, 2023, through December 31, 2027. In order to capitalize on this opportunity, eligible calendar-year taxpayers must make a tentative credit reservation during the month of July to claim the credit on their 2023 CA income tax return.

Who qualifies for the HRCTC

To be eligible, you would need to meet three basic requirements.

Which expenditures qualify for the HRCTC

There are several types of expenditures eligible for the credit with specific parameters that you would need to meet to qualify for them. Qualified expenditures are amounts that you have paid or incurred for any of the following expenses.

Wages for full-time employees

Not every employee has to meet these requirements — but for those that do, their wages count as a qualified expenditure. First, full-time employees must be paid for no less than an average of 35 hours per week — or they must be a salaried employee paid compensation for full-time employment.

In addition, full-time employees must be paid no less than 150% ($23.25) but no more than 350% ($54.25) of the state minimum wage. To meet the 150% minimum wage requirement, you may include the following employee benefits in qualified wages: group health insurance, childcare support, employer contributions to employer-provided retirement plans, or contributions to employer-provided pension benefits. But if you pay employees wages that surpass more than 350% of the state minimum wage, those wages are not considered a qualified expenditure.

Safety-related equipment, training, and services

Expenditures related to safety, training, and providing services can also qualify if they meet the following criteria:

Equipment primarily used by the employees of the cannabis licensee to ensure personal and occupational safety, or the safety of the business’s customers.

Training for nonmanagement employees on workplace hazards. (This includes safety audits, security guards, security cameras, and fire risk mitigation.)

Workforce development and safety

Qualified training for your employees includes:

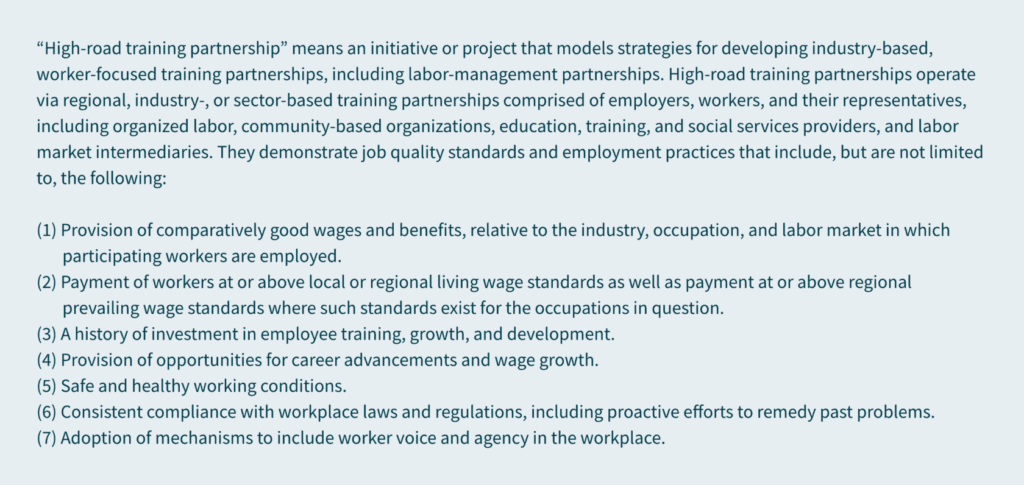

Joint labor management training programs

Membership in a joint apprenticeship training committee registered by the Division of Apprentice Standards, and a state-recognized “high-road training partnership” (as defined in Section 14005 of the Unemployment Insurance Code).

Available credit

The amount of available credit is equal to 25% of qualified expenditures. The aggregate credit that can be claimed by each taxpayer (as determined on a combined reporting basis) is a maximum of $250,000 per year. Any unused credit can be carried over to the following eight taxable years. Availability is limited as the total cumulative amount of HRCTC available to all taxpayers is $20 million.

To claim the HRCTC on your California tax return, you must reduce any deduction or credit otherwise allowed for any qualified expenditure by the amount of the HRCTC allowed.

How do I make a tentative credit reservation — and when?

You must make a tentative credit reservation (TCR) with the FTB to claim the credit. This reservation must be made online and once you’ve done so, you’ll receive an immediate confirmation. FTB currently reports that the system will be up and running by July 1, 2023, but you can start preparing now.

How we can help

The HRCTC is a valuable tax credit opportunity for any commercial cannabis business operating in California. Determining if you qualify and calculating how much you can save could be complex. Our extensive experience in cannabis, cannabis tax, and state and local tax enables us to help you take advantage of this tax credit so you can stay focused on thriving in this ever-growing, culture-shaping industry.

Reach out to MGO’s State and Local Tax team to find out whether you qualify for this tax credit opportunity and determine how much you could potentially save.

California Governor Newsom strives to amend the personal income tax laws to prevent wealthy taxpayers from utilizing Incomplete Gift Non-Grantor trusts.

California residents use this by transferring assets into trusts held by nonresident trustees in states without income tax.

If this legislation passes, taxpayers will no longer be able to take advantage of the strategy.

If you reduce California income tax with an ING, Newsom is onto you

Californian legislators propose to amend the personal income tax laws to close a little-known-but-effective loophole for the wealthy by targeting Incomplete Gift Non-Grantor (ING) trusts set up in other states with more favorable income tax rules. To date, California residents have had the opportunity to transfer assets into these trusts held by nonresident trustees in states without income tax, utilizing the state’s sourcing rules to avoid the tax. If approved, this new legislation will put a stop to this tax planning strategy.

Taxing the rich in California

As it stands, the ING trust is not commonly used. There are about 1,500 California residents with this trust in states without income tax — and if implemented, California would see a minimal revenue increase (about $30 million in the first year and $15 million in the following years). However, this would put an end to a tax planning strategy the wealthy have been using to their benefit for about 20 years.

Because California is home to more billionaires than any other state at the same time as it also has the highest rate of poverty in the U.S., the concept of taxing the rich holds a certain appeal. In the past, Newsom has opposed proposals to raise taxes — but this proposal was included in the governor’s $223.6 billion budget plan for the next fiscal year, which begins in July. Whether the item survives the legislative process remains to be seen, but if New York’s passage of a similar law in 2014 is any indication, we are likely to see the end of this tax planning strategy for California’s ultra-rich.

Moreover, this proposal has a retroactive element, differentiating it from New York’s and opening it up to potential lawsuits (New York trust holders had a five-month period to move their accounts to a different type of trust without incurring the tax). Newsom is pushing for the measure to begin the calendar year after its implementation.

How the ING works (worked)

What is an ING, and why is Newsom trying to prevent its use? California taxpayers can transfer their assets into out-of-state, incomplete, non-grantor trusts (INGs), which constitute separate, taxable entities under state and federal tax law, and this move avoids California income tax on any appreciation or gains from those assets because it is “sourced” to another state based on the location of the trustee (i.e., the bank or whatever financial institution offers the trustee services in the other state). The non-grantor aspect comes into play when the taxpayer establishing the trust (the “grantor”) gives up control over managing investments or distributing assets to the trustee (contrast with a “grantor trust” in which the grantor continues to control how money is invested/distributed within the trust during their lifetime). For the trust to be deemed “incomplete,” the grantors specify how the money can be used.

Some of the states where these trusts are typically established include Florida, Wyoming, Delaware, Nevada, Tennessee, and South Dakota. For example, a California resident (TP) may decide to transfer stock in their business into an ING established in South Dakota. If TP held the stock directly, then as a resident, all the dividends (or if he sold it, the gain) would be taxable by California on their personal income tax return. But since TP doesn’t hold the asset – the ING does – the ING recognizes the income relating to the stock. California’s current rules provide that the income is sourced to (and thus taxable in) the state where the trustee is domiciled, and for this ING that location is South Dakota, which, incidentally, does not tax this sort of income.

Newsom is hoping that by eliminating this tax-free option, the state of California will be able to increase tax revenue in a way that will not alienate a large number of voters.

How MGO can help

If you are a California resident and currently use an ING as a tax strategy, there are steps to take now to avoid a negative impact. MGO’s experienced Private Client Services team can help you identify and implement an effective response.