CFDs and IFDs are common options for financing capital projects, but have key differences in funding sources and eligible uses.

As component units, CFDs and IFDs must be included in your government’s financial reporting.

Determining whether to report CFDs/IFDs as fiduciary, blended, or discrete component units is crucial for accurate representation.

~

As a government leader, you are no doubt all-too-keenly aware of the challenges inherent in financing capital projects in your community. One popular option to fund infrastructure improvements in developing areas is forming special tax districts — with two of the most common variants being community facilities districts (CFDs) and infrastructure financing districts (IFDs).

While both these types of special tax districts share many similarities, it is their differences that can have a significant impact on how you report them in the financial statements of your organization. In this article, our State and Local Government professionals walk through what you need to know to successfully navigate special tax district reporting.

What are CFDs and IFDs?

Before we dive into reporting, here is a glimpse at how each of these special tax districts work and how they are different from one another.

CFDS – Funding Versatile Local Improvements

CFDs also known as Mello-Roos Districts (named for the lawmakers behind the legislation that created them), are a popular method of financing certain public capital facilities and services — especially in developing and rehabilitating areas. CFDs impose special taxes on property owners within the district, and proceeds can be used to fund any publicly owned facility with a useful life of five or more years.

This versatile special tax district has many eligible uses — including parks, libraries, childcare and recreation centers, storm drainage systems, and more. Developers frequently establish CFDs to fund initial infrastructure as an area is built out.

IFDs – Financing Large Infrastructure

IFDs fund capital projects focused on large-scale, community-wide infrastructure needs. This includes major initiatives like highways, transit facilities, sewage treatment plants, dams, flood control systems, and other regionally significant projects.

Unlike CFDs, IFD funding comes from growth in property tax increment above a base-year level, redirecting tax revenue that would otherwise flow to participating jurisdictions like the city, county, and special districts. In essence, those entities waive their rights to extra revenue generated by growth in the IFD area until the established revenue retention period expires (this period may last up to 30 years).

Special Tax Districts as Component Units (and What That Means)

Current accounting standards require your government to include in its financial statements the finances of “component units”. Component units are legally separate entities for which the elected officials of a primary government are financially accountable. The primary government is financially accountable if it appoints a voting majority of the entity’s governing body and: (1) it can impose its will on that entity or (2) there is a potential for the entity to provide specific financial benefits to, or impose specific financial burdens on, the primary government.

Under California law (different states may have different requirements), CFDs and IFDs are legally constituted governmental entities. They are established by and governed by your agency’s legislative body, whether that be the city council or county board of supervisors. This governance structure grants your government the ability to impose its will on the CFDs and IFDs since you can modify budgets or appoint key personnel. Moreover, IFDs create a financial burden by capturing property taxes that would otherwise fund services in participating jurisdictions.

Due to this financial accountability, CFDs and IFDs are considered component units and should be included in the financial reporting entity of the primary government. That means, as a primary government, you are required to report component unit financial information within your financial reporting entity’s financial statements.

Fiduciary, Blended, or Discretely Presented: Determining the Reporting Method

While the objective of including component units in your financial statements is to provide an overview of your government based on financial accountability, the method of component unit inclusion – fiduciary, blended, or discretely presented – depends on the closeness of their relationship with your government.

To assess whether a special tax district like a CFD or IFD is a fiduciary activity for reporting purposes, ask these questions:

Does your government exercise control over the assets of the district?

Does the government benefit from those assets (as opposed to external parties)?

With CFDs and IFDs, the assets are typically controlled by your government but maintained for the benefit of the district (not external parties). Therefore, their relationships with your government generally do not qualify as fiduciary.

For IFDs, the revenue they receive by capturing incremental property taxes warrants blended reporting within your government’s financial statements. That means their activity is reported like any other fund – blended in the special revenue funds or other reporting units.

Treatment gets trickier for CFDs. The key factor is whether your government is obligated in any manner for repayment of the CFD’s bonded debt in the event of delinquencies or default by property owners. If your government must back the debt, the CFD is considered a financial burden and blending is appropriate. Blending makes the long-term debt obligation clearly visible to financial statement users.

However, if your government has no obligation for CFD debts, the CFD should be reported in fiduciary funds. Here, your government serves as an agent on behalf of property owners and the bondholders within the CFD. The debt service transactions are kept separate from other activities.

Ensuring Accurate and Transparent Financial Reporting

Complicating CFD and IFD reporting is the reality that major capital improvements are often funded by a combination of financing mechanisms. You may need to untangle several types of debt and financing sources – such as grants from other governments, general obligation debt, and special assessments. The reporting guidance on CFDs and IFDs is not one-size-fits-all.

As a steward of public resources, it is important to take care to consider all nuances of how districts are established and financed in your government. Accurately reporting CFD and IFD activities is central to upholding your responsibility to constituents. By proactively addressing district reporting, you also minimize audit issues or restatements down the road. Taking the time upfront to thoroughly understand the standards will pay dividends.

While financing capital projects may be challenging, you don’t have to figure it out alone. Our specialized State and Local Government team can guide you through the nuances of CFD and IFD reporting. Contact our professionals today to discuss how we can help you meet the highest standards of accountability and transparency.

State and local governments spend billions of dollars a year procuring goods and services. However, during the procurement process, they can hit major snags and challenges that hinder them from successfully purchasing or procuring anything.

To prevent wasting valuable time and resources, it is important to perform assessments of policies, procedures and processes to identify inefficiencies and opportunities for improvement so your organization can succeed in its pursuits.

Inefficiencies in government procurement and purchasing processes

The COVID-19 pandemic acted as a catalyst for many state and local governments, demonstrating that improvements were needed when it came to their procurement and purchasing processes. Thanks to federal relief programs like the CARES Act, many organizations were able to receive the funds for economic assistance. But these programs had time constraints, meaning the money had to be spent within a relatively short time frame. Many state and local governments were interested in using the funds to purchase goods, such as personal protective equipment, and to contract with subrecipients to provide services to populations in need, such as the homeless.

However, the procurement and contracting processes took time — oftentimes, more time than the state and local governments had with the constraints set by the relief programs. This meant the funds could be wasted if the contracts were not pushed through in a timely manner.

Remote work, which was not prevalent before the pandemic, revealed issues for many state and local governments related to their lack of automated processes. For example, some organizations still collected “wet” signatures on resolutions and contracts instead of using digital programs like DocuSign. They only learned of inefficiencies like these when everyone was working from home, leaving them to wonder how to fix similar and additional issues plaguing them.

Common issues facing procurement and purchasing

Say your organization has an IT department that has a workflow requiring its staff to manage requests in a certain way. Instead of “touching” the request just once and approving it, the purchasing employee must handle the same request three times. This is clearly inefficient, but oftentimes, state and local governments don’t realize the snags their departments are facing throughout their processes.

There are several reasons why this could be. For example, you could have a team that is stretched too thin, with several people doing multiple jobs — there are too many things to process and not enough resources, leading to things slipping through the cracks. Maybe the organization is facing a lot of turnover or new management, and without clearly outlined processes, no one is sure how to spread the workload effectively. Bottlenecks can arise, hindering progress further. Without documented procedures, roles, and responsibilities, your team won’t know who is responsible for what. And if your organization is decentralized — this can lead to even more confusion, slowing down procurement and contracting processes even further.

Details and communication are essential

If one of your departments requires a red truck and puts in a request without any detail, your purchasing department, could take a guess and buy a red truck – which may or may not meet the needs of the department. There are many kinds of red trucks, and by the department not specifying what red truck they want, time is wasted, slowing down whatever project the red truck is needed for. Does the department need to haul something? Does it need four-wheel drive? What will it be used for? Purchasing departments know how to purchase goods and services, but rely on the other departments to provide specific details on what to purchase. Purchasing needs details — and back-and-forth communication is inefficient. The organization needs to set clear responsibilities to determine the scope so purchasing can do its job, making the process far more seamless.

Plainly, state and local governments face major hurdles when trying to get a contract out the door — it can take some governments six to eight months. With many steps, including bids, evaluations, approvals, and negotiations, the process can even stretch into the next fiscal year by the time it’s finally executed. The length of time is tedious — and unnecessary. Is there a way to make the length of time shorter, or make the process more efficient?

Steps to address payment and procurement inefficiencies

A third-party assessment of your procurement and contracting processes will tell you where the inefficiencies lie — and provide recommendations on how to fix them. All you need to know is the process isn’t working, and we can do the rest.

Here is a quick look at some of the steps of an assessment:

Review current processes and practices

Identify bottlenecks and root causes of inefficiencies

Break down resource constraints with processing requests for bids or proposal

Review necessary documentation and procedures

Evaluate for best practices and opportunities for improvements

Develop detailed methods for performance improvement

Outline how to more efficiently use the resources you already have, information technology and staff

Develop training and communicate the issues discovered

Educate on how to more efficiently utilize current technology

State and local governments have distinct responsibilities to their constituents. In order to meet their needs effectively, it is crucial that they identify oversights and fulfill any control duties as efficiently as possible.

How MGO can help

At the end of the day, it can require a significant amount of time, resources, and effort for state and local governments to uncover issues and implement best practices. MGO delves deep, utilizing our extensive resources and professionals to go in, identify the issues, and recommend how to fix it — so your procurement and contracting processes flow more seamlessly, no matter your resources, staffing numbers, and size.

MGO’s dedicated State and Local Government team functions as an additional level of control to improve these important processes with comprehensive innovative strategies and solutions so you can focus on minimizing risk, optimizing performance, and exceeding the expectations of your boards, stakeholders, and communities. Contact us to learn more.

The Governmental Audit Quality Center (GAQC) promotes the importance of quality governmental audits and the value of such audits to purchasers of governmental audit services. GAQC is a voluntary membership center for CPA firms and state audit organizations that perform governmental audits. The GASB Matters section of the GAQC site highlights key interest areas, key resources, and advocacy efforts related to state and local government engagements.

Pension-related matters

GASB Pensions: Issues & Resources page of the GAQC Web site consolidates the various resources available to practitioners to assist with understanding the new standards and developing appropriate audit strategies. This page also includes links to various whitepapers and related auditing interpretations addressing cost-sharing and agent multiple-employer plans. Comment Letters

September 16, 2019 comment letter on GASB’s Exposure Draft, Public-Private and Public-Public Partnerships and Availability Payment Arrangements

September 16, 2019 comment letter on GASB’s Exposure Draft, Omnibus 20XX

April 30, 2019 comment letter on GASB’s Exposure Draft, Leases Implementation Guide

March 8, 2019 comment letter on GASB’s Exposure Draft, Fiduciary Activities Implementation Guide

February 14, 2019 comment letter on GASB’s Financial Reporting Model Improvements & Recognition of Elements of Financial Statements

On May 18, 2021, the House of Representatives passed the State and Local Cybersecurity Improvement Act (SLCIA) to address cybersecurity vulnerabilities and promote additional cybersecurity collaborative efforts between the Department of Homeland Security (DHS) and state, local, tribal, and territorial governments. The bipartisan bill was received in the Senate on July 21, 2021, read twice, and then referred to the Committee on Homeland Security and government affairs, where it has been sitting since. Once it passes, it will go to the President’s desk, where it will then immediately provide incentives to address the increasing danger of malicious cyberattacks on state and local IT infrastructure.

Giving state and local governments the resources to protect against hackers

This collaboration will encourage conducting cybersecurity exercises and hosting trainings meant to address current or future cyber risks or incidents. It will also provide operational and technical assistance to state and local governments to implement security resources, tools, and procedures to improve overall protection against attacks. The goal is to provide state and local governments with the support they need to defend themselves from hackers.

Resources to bolster government security capabilities

The SLCIA establishes a $500 million DHS grant program that will empower government institutions to increase their focus on cybersecurity. The bill also:

Requires CISA to develop a strategy to improve cybersecurity of state, local, tribal, and territorial governments, enabling them to identify federal resources to capitalize on as well as set baseline objectives for their efforts;

Indicates state, local, tribal, and territorial governments must develop a comprehensive cybersecurity plan to guide their usage of any grant money they receive;

Establishes a state and local cybersecurity resiliency committee made up of representatives from state, local, tribal, and territorial governments to provide awareness of cybersecurity needs; and

Enjoins CISA to assess the feasibility of a rotational program for the detail of approved government employees holding cyber positions.

The bill gives state and local governments the push they need to begin defending their networks. This can include the development of new strategies to boost their cybersecurity capabilities and acquisition of the funding needed to ensure their implementation. By investing in cybersecurity ahead of an attack, an entity is more likely to save money and protect its data.

Assessing eligibility for cybersecurity grants

Cybersecurity grants are available to municipalities of all sizes — but it’s important to start strategizing now by considering your IT infrastructure and cybersecurity frameworks. By applying for the grants, you indicate that you are taking your entity’s security seriously and taking the proper steps to qualify.

The State and Local Cybersecurity Improvement Act will provide up to $1 billion in grants for state, local, tribal, and territorial governments, allowing them to directly address their cybersecurity threats and risks. The program’s funding starts at $2 million for 2022, $400 million for 2023, $300 million for 2024, and $100 million for 2025.

To be eligible, an entity must:

Maintain responsibility for monitoring, managing, and tracking its information systems, applications, and those user accounts owned and operated by the government;

Show it has a process of continuously prioritizing the assessment of its cybersecurity vulnerabilities and threat mitigation practices; and

Have a tangible plan that outlines:

How to manage and audit network traffic.

How the government plans to use the information to improve its systems’ resiliency and strength.

Our perspective

While the bill is still waiting on the Committee on Homeland Security and Governmental Affairs there are some things you can do to make sure you are ready. State and local governments should focus on building teams that can handle the grant application process — and be prepared to implement once awarded. This bill indicates that governments are past the point of merely updating a firewall or running a generic virus program — things like multifactor authentication and zero-trust architecture are viewed as the next steps (which was required for federal agencies in a 2021 executive order).

How we can help

Prior to starting the grant application process, your IT leaders should start thinking about how to handle security gaps with various procedures and consistent tests. MGO can help. Our Technology and Cybersecurity team can provide guidance as you prepare for the future.

About the authors

Francisco Colon is a Partner at MGO with extensive experience in external audit, fraud examinations, litigation support, operational and internal controls reviews, and buyer/seller due diligence. He specifically focuses on assisting organizations with evaluating and updating their internal controls with a focus on strategic alignment and fraud litigation deterrence management in a variety of industries, including tribal government, gaming, technology, cannabis, hospitality, government contracting, distribution, manufacturing, and private equity. Contact Francisco at [email protected].

We can expect that ESG-related disclosures will shift from voluntary guidance to mandatory reporting at some point.

Reporting and disclosure of environmental, social, and governance (ESG)-related information has long been a priority in the private sector and is now emerging as a key area of focus for state and local governments (or “government entities”).

In response to interested parties seeking more ESG-related information (e.g., investors, credit rating agencies, preparers and auditors of financial statements, citizens, policymakers, etc.) from government entities, the Governmental Accounting Standards Board (GASB) has released a publication to clarify how ESG-related information intersects with their existing standards.

The bottom line: GASB’s stakeholders and interested parties are seeking to understand the impacts of ESG-related matters on a government entity’s cash flows, financial position, and overall responsibility for fiscal accountability — and the publication can be seen as a form of interpretive guidance to bridge the gap.

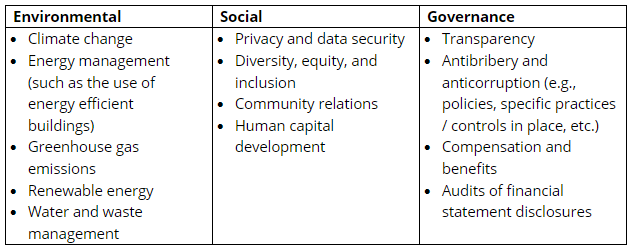

Up front, the publication acknowledges that “a single consistent definition of ESG is not prevalent in practice today.” However, broad examples are included in the publication for each pillar (note, the below list has been shortened for purposes of this article):

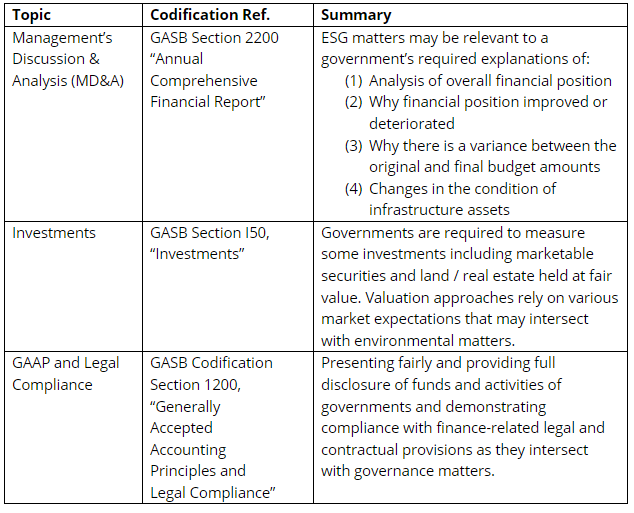

The interpretive portion of the publication goes on to assist government entities with detailed examples of how ESG-related information coincides with the current GASB standards (note, the below are 3 of 25 total examples from the publication):

Why this GASB release matters

In publishing this document, GASB is taking a traditional first step to introduce concepts and guidelines that set a foundation ahead for new reporting and disclosure rules in the future (also referred to as “interpretive guidance”).

This is not the first time a regulator or standard setter has issued interpretive guidance specific to ESG. In 2010, the Securities and Exchange Commission (SEC) released their own interpretive guidance to provide clarity to the private sector on how to leverage existing financial reports to make disclosures related to climate change. While it was uncertain how many companies would incorporate climate-related information in their financial reports, many chose to do so (at last count by the SEC in 2020, 33% of the 6,644 filings submitted to the regulator contained some form of climate-related disclosure). The interpretive guidance, therefore, laid the groundwork for a new climate-related proposal issued by the SEC in March 2022.

Essentially, interpretive guidance has historically preceded the release of new, formal guidance and the creation of new standards. If this proves true in the public sector, then we will first see an increase from state and local governments enhancing their existing financial reports and disclosures by incorporating ESG-related information. Subsequently, and after further analysis by GASB of those enhanced disclosures, we will likely see the release of a new ESG-specific standard from GASB.

Increasing the pressure

As demand for ESG-related disclosures increases, pressure will also increase on governments to begin providing or enhancing the disclosures in their financial reports. Further, if your entity issues securities (e.g., municipal bonds), you may encounter pressure from credit rating agencies depending on your approach (or lack thereof) to disclose and address ESG-related risks.

At present, ESG-related disclosures are contingent on a variety of factors (including but not limited to the government entity’s location, the historical or anticipated impacts of climate change, the level of ambition to become a leader in ESG-related reporting, etc.), but at some point these disclosures will shift from voluntary to mandatory.

How MGO can help

Many state and local governments have proactively disclosed ESG-related information on their websites or in standalone ESG / sustainability reports; however, GASB’s interpretive guidance demonstrates that ESG-information also needs to be considered when preparing your annual financial reports.

To stay ahead, MGO is helping the public sector as well as the private sector, develop and enhance their ESG disclosure strategies.

If you are interested in learning more, schedule a conversation with our ESG team today.

Grant requirements can be complicated. Developing a systematic grant management program provides a framework to mitigate against noncompliance. A sound framework includes five main elements. Answering the following questions will help identify areas you may need to strengthen to ensure your organization’s compliance.

Who is your grant administrator?

This seems like a simple question, but if an organization only has a few grants, grant administration may be one of many roles. Or, responsibility may be shared among several roles. That situation works until the size of the organization and the complexity of the grants make responsible grant management impossible.

When the responsibility and complexity of grant management becomes too demanding to include as one of many responsibilities, it’s time to identify one person to take the lead. Eventually, that person may build the team responsible for overseeing and coordinating grant administration.

It is easy to see the benefits of having one person develop the full knowledge of grant requirements and take responsibility for establishing policies and procedures for the organization. This person provides guidance for the organization and monitors compliance requirements. They also serve as the point person for grant related audits.

Do you have policies and procedures for grant administration?

A grant administrator’s first priority is to develop policies and procedures that outline each step in the lifecycle of the grant. Typically, this document will answer the following questions:

Who approves grant applications?

Who executes grant agreements?

What systems will be used to track grant activities, such as qualifying expenses, reporting dates, performance metrics (both financial and programmatic)?

What documentation is required for compliance?

Who reviews and approves grant activities to ensure compliance?

Who develops and manages a schedule and process for annual financial reporting (financial statements and grant reporting, e.g., single audit)?

Who is responsible for training staff in grant requirements?

Are subrecipient contracts standardized, and do they comply with your responsibilities as a grantor?

Who is responsible for resolving audit findings?

Are you prepared for grant reporting?

One of the key responsibilities of a grant administrator is to manage deadlines (monthly, quarterly, biannually, annually, and grant close out). In addition to the initial application deadline, grants require consistent attention. You need to file updates and reports throughout the life of the grant, and they will often require specific documentation. The information in these reports must be complete, accurate, and filed promptly. If they are not, you can count on the grantor requiring you to follow-up and resolve the issues.

Do you have the resources to monitor activities?

It’s true, monitoring grants is a full-time job. Or it should be.

Being awarded a grant is the first chapter of a long story. The rest of the tale involves using the grant for its intended purposes and documenting that fact. Responsible monitoring and documentation require time, energy, systems, and personnel.

Someone should be assigned responsibility for the continuous monitoring and evaluation of grant administrative policies and procedures. This involves looking for changes in grant requirements communicated by the grantor.

For subrecipients, the grant administrator must convey the expectations about their activities and then monitor the progress toward the stated goals. On-site visits will sometimes be necessary and require time. Verifying the status of periodic reporting responsibilities can also take up resources that may already be scarce.

The final chapter of monitoring activities is to develop a clearly defined plan for responding to audit findings. Depending on the complexity of the findings, resolving these issues can require rewriting procedures, documenting changes, and verifying the implementation.

Are you ready for an audit?

While this may seem obvious, knowing your requirements should be the first step in preparing for the possibility of an audit.

In addition to reviewing grant requirements, look back at your prior year findings to confirm that they were fully resolved. If they were not, they need to be addressed immediately.

The next step in being prepared for an audit is to ensure all necessary documentation is complete and accurate. Your documentation should demonstrate compliance with the grant requirements. Usually, your materials will need to include evidence of internal controls that supports the process of reviews and approvals. Internal policies and procedures should be easily accessible. (Thankfully, once this document is complete, it only needs to be updated going forward.) When these items are assembled, make sure all reconciliations connected to the grant are complete.

Once the preparations are made, the hardest part of an audit is done. You will still need to meet with auditors and discuss expectations, timelines, and requests for information, but these are more scheduling and time management issues. If your paperwork and systems are in good order, your work will consist mainly of providing evidentiary support, and possibly providing explanations on details that may not appear obvious to an outsider.

Continuously improving your grant compliance processes

With a lot of subjectivity in the process of managing grants, along with requirements changing on a regular basis, it is important to continuously evaluate the adequacy of your grant administration policies and procedures. So, no matter what your situation is, your processes can always improve, and any deficiencies can be remediated. But it takes commitment as an organization to devote the resources to do the ongoing work of grant compliance.

Many state and local governments have compliance questions about the federal grants that were distributed during the pandemic. The reporting rules of these programs are complex, and requirements continue to evolve.

MGO’s state and local government professionals can help answer questions about these federal grants and help organizations document their systems of internal controls, improve their audit preparation, and address audit findings. Contact Linda Hurley at +1 (949) 296-4340 or [email protected] for more information on how to improve your grant compliance processes.

Throughout the COVID-19 pandemic, state, local, and Tribal governments have been on the frontlines, organizing and providing essential medical care and navigating the endless complications created by shutdowns in their communities. Until now, these government agencies have received aid to directly support COVID-19 responses, but not address disastrous budget deficits, looming layoffs and other emerging issues.

That all changed on March 11, when President Biden signed the American Rescue Plan Act of 2021 into law. The bill allocates $432 billion in direct financial support to U.S. territories, states, and local and tribal governments. In the following, we highlight how the bill affects state, local, and Tribal governments, and breakdown the details of key provisions.

American Rescue Plan of 2021: Impact on State, Local and Tribal Governments

The American Rescue Plan of 2021 contains wide-ranging programs designed to support state, local, and Tribal governments through the financial crises resulting from the COVID-19 pandemic. These include active support for COVID-19 response and planning, funds for in-state capital improvement projects, emergency housing support, and much more.

Much of the relief funding is allocated and disbursed automatically using metrics that include population, economic conditions, and unemployment rates. While each program has different disbursement details, broadly speaking, payments are delivered in two or more installments, the first coming within a 60-day window following the bill becoming law, and future installments through 2022 and beyond.

Other programs will require state and local authorities to apply for grants based on specific needs.

One of the highlights of the revised funding and plan is looser restrictions on how funds from the Coronavirus State Fiscal Recovery Fund can be utilized. The accepted uses include: • Funding government services that have been curtailed due to decreases in tax revenue caused by the pandemic. • Aid to households, small businesses and nonprofits, and impacted industries like tourism, hospitality and travel. • Making “necessary investments” in water, sewer, or broadband infrastructure.

While potential uses have been broadened, all programs require stringent rules for intended use, tracking and reporting.

50 States and the District of Columbia receive $195.3 billion in aid:

$25.5 billion will be split evenly among each state and the District of Columbia, with each state and the District of Columbia receiving $500 million in aid.

$168.55 billion distributed based on each state’s share of total unemployed workers over the period of October 2020 to December 2020.

District of Columbia receives additional $1.25 billion.

Tribal governments receive $20 billion (further discussion to come).

U.S. territories receive $4.5 billion.

U.S. Treasury receives $50 million to cover costs of administration of the fund.

Local governments to receive $130.2 billion in aid to be split among counties, metropolitan cities, and non-entitlement units of local government:

Counties receive $65.1 billion in population-adjusted payments, with additional adjustments for Community Development Block Grant (CDBG) recipients.

Metropolitan cities receive $45.57 billion.

Non-entitlement units of local government receive $19.53 billion, distributed by individual states and funded by the U.S. Treasury. Each jurisdiction receives population-adjusted payments based on such jurisdiction’s share of the state population.

$10 billion available for states, territories, and Tribal governments to support critical capital projects directly enabling work, education and health monitoring in response to COVID-19:

Each state receives $100 million.

U.S. territories receive $100 million to be split among them.

Tribal governments and the state of Hawaii receive $100 million to be split among them.

Remainder of funds to be allocated to states based on population.

NOTE: The Treasury Department will establish an application process for grants from the fund within 60 days of enactment of the law.

$2 billion for eligible revenue-sharing counties and tribal governments:

Eligible revenue-sharing counties will receive $750 million allocated based on economic conditions for each FY 2022 and FY 2023.

Eligible tribal governments will receive $250 million allocated based on economic conditions for each FY 2022 and FY 2023.

NOTE: Payments from this fund may be used for any governmental purpose other than a lobbying activity and will remain available until September 30, 2023.

Other State, Local, and Government Funding Sources

Additional federal government programs have received funding earmarked to support recovery efforts in states, Tribes, and territories. These funds can be applied for via grant applications depending on each government agency’s circumstances.

$10 billion allocated to states, territories, and tribes through grants to prevent homeowner mortgage defaults, foreclosures, and displacements.

Funds may be used to reduce mortgage principal amounts, assist homeowners with housing payments and other aid needed to prevent eviction, mortgage default, foreclosure, or the loss of utility services.

Funds may also reimburse state and local governments that have provided similar assistance since January 2020.

Each state, along with the District of Columbia and Puerto Rico, will receive at least $50 million. Additional amounts will be set aside for other U.S. territories and tribes.

States, territories, and Tribes receiving funding will have to set aside at least 60% of their allocation to assist homeowners who make less than 100% of the local or national median income.

Homelessness Assistance and Supportive Services Program

$5 billion allocated to state and local governments to provide supportive services for homeless and at-risk individuals. Permitted fund uses include tenant-based rental assistance, housing counseling and homeless prevention services, and acquiring non-congregate shelter units.

Low-Income Home Energy Assistance Program (LIHEAP) and Water Assistance Program

$4.5 billion allocated to fund the LIHEAP program, and $500 million provided in state grants to assist low-income households with drinking water and wastewater services.

$50 billion to reimburse state and local governments for the costs of ongoing COVID-19 response and recovery activities, and other emergencies.

Funding to remain available through FY 2025.

Final thoughts

With billions of dollars in aid becoming available to state, local and tribal government agencies, the use of these funds is going to be tracked very closely by federal regulators. If you have any questions about how funds can be utilized, and how to track and report this use, MGO’s dedicated State and Local Government team can help. Contact Us.

With every state and local government institution doing their best to manage adversity during the COVID-19 pandemic, federal lawmakers have made support available through the CARES Act and related economic stimulus packages.

To assist our state and local government clients during these unprecedented times, MGO is offering support designed to help you understand and access funding options, manage regulatory complexity, and institute financial best practices.

Support accessing CARES Act funding

Assistance with identification of eligible funding provisions within the CARES Act.

Training of applicable personnel regarding CARES Act provisions and requirements.

General Advisory Services related to CARES Act provisions and requirements.

Assistance with preparation of initial appropriation requirements, if applicable.

Process and procedure development for CARES Act funding provision requirements by source, including:

Governance

Document Retention

Procurement

Timelines & Scope

Reporting and Other

Assistance with preparation of ongoing reporting requirements by funding provision.

Preparation of cash flow and revenue projections resulting from the impact of COVID-19.

Identification of methods to address budget gaps resulting from the impact of COVID-19.

For more information, please contact your MGO advisor directly, or email our team at [email protected]

On March 27, 2020 the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) was signed into law by President Donald Trump and is the largest economic stimulus package in U.S. history.

The bill is the third phase of Congress’ COVID-19 response and provides substantial federal government support aimed to address the economic fallout associated with the COVID-19 pandemic in the United States.

For state and local governments the Act provides substantial appropriations to assist with the financial impacts of COVID-19. There are various funding provisions that state and local governments will be able to participate in, each of which has differing eligibility and reporting requirements.

MGO understands the complexities of this historic Act and in an effort to provide support and clarity to our state and local government clients we have summarized some of the significant funding sources by type, total monies allotted, general purpose, and eligible parties.

As state and local governments, you will be facing significant fiscal and personnel restraints not only due to new costs incurred directly related to the COVID-19 pandemic, but also due to decreased revenue resulting from the reduction in overall economic activity. As leaders in serving state and local governments for more than 30 years, we are here to help you navigate through this time.

For more information, please contact your MGO advisor directly, or email our team at [email protected].

Greta Bernard MacDonald, MPA Director, Macias Gini & O’Connell LLP Scott P. Johnson, CPA, CGMA Partner, Macias Gini & O’Connell LLP

As the second article in a three-part series, this piece provides more detail on the professional standards associated with governmental performance audits. It provides discussion on (1) why an agency would want a performance audit instead of a non-audit engagement and vice versa; and (2) what key factors should be considered.

As a recap, in Scott Johnson’s first article, “Does Your Organization Have a Need for an Independent Eye on Performance?,” his overview of the differences between engagement types and the applicable standards of each, which then provided a range, from a performance audit under generally accepted government auditing standards as set forth in Government Auditing Standards (commonly referred to as the Yellow Book or GAGAS) to an advisory services engagement under the AICPA’s Statement on Standards for Consulting Services. The forthcoming third article will focus on GAGAS performance audit reporting standards and a sample report outline.

In performance audit trainings, the same story is often told that the group that put the Yellow Book together in the 1970s intended it to have a gold cover; and it was originally titled, “The Golden Rules of Auditing.” While it may be just a myth, the truth of the matter is, regardless of the color assigned to the original book, GAGAS performance audits are the gold standard for governmental operational audits. The standards provide auditors with the framework they need for a solid, fully-supported product – exactly what the public demands for accountability and improvements when it comes to any taxpayer-funded program or operation. Performance audits also provide the end user of the report – citizens, government officials, and legislators, as well as the government entity (client) — with the added assurance of the auditors’ objectivity and independence.

This article is focused on government auditing, which is essential in providing accountability to legislators, oversight bodies, those charged with governance, and the public,1 as well as non-auditing consulting engagements in the government sector. The information presented can be useful to practitioners and clients in making engagement decisions, and for clients to better understand factors to be considered when an engagement opportunity arises.

Performance audits have become a central feature in responding to the need for accountability. This is a clear benefit because they go beyond traditional transactional or financial audits to address the efficiency, effectiveness, and economy of government programs. In terms that financial auditors may relate to, one can look at financial audits and performance audits as the flip sides of the same accountability coin. One side looks at whether management has provided users of financial statements with reliable information, while the other side whether management has met its responsibilities efficiently and effectively. Overall, both Financial and Performance Audits serve the taxpaying public because they hold managers of government programs accountable for the dual roles of ensuring fair representation of financial information and program operations are efficient, effective, or in compliance.

Performance audits defined:

Performance audits provide objective analysis that can assist management, and those charged with governance and oversight, in using the audit findings and conclusions which can improve program performance and operations, reduce costs, facilitate decision making by parties with responsibility to oversee or initiate corrective action, and contribute to public accountability.2 Performance audits provide findings or conclusions based on evaluation of sufficient, appropriate evidence against specified criteria. Performance audits conducted under GAGAS can provide one of the highest levels of assurance due to the level of work required to develop the required elements of a finding and provide recommendations, as compared to other types of engagements like attestation engagements, where the level of assurance can be lower, based on the objectives of the engagement.3

The professional standards that auditors must follow when conducting governmental performance audits are known as GAGAS, also known as the Yellow Book.4,5 Specifically, the Yellow Book states that GAGAS provides a “framework for conducting high quality engagements with competence, integrity, objectivity, and independence.”6

The Yellow Book is used by auditors of government entities, entities that receive government awards, and other audit organizations performing Yellow Book audits. These audits are “essential in providing accountability to legislators, oversight bodies, those charged with governance, and the public,” and “provide an independent, objective, nonpartisan assessment of the stewardship, performance, or cost of government policies, programs, or operations, depending upon the type and scope of the engagement.”7

1 See Paragraph 1.05 of GAGAS 2 See Paragraphs 1.21 and 8.14 3 Attestation engagement standards are covered in GAGAS Chapter 7, and include agreed-upon-procedures, reviews, and examinations. Examinations have the highest level of assurance of attestation, as an opinion is given, not so for the others. GAGAS incorporates AICPA standards by reference for financial audits and attestation engagements. In addition, AICPA promulgates the consulting standards. AICPA standards committees have taken the position that only the GAO sets performance audit standards. 4 The most recent version of the Yellow Book was issued by the Comptroller General of the United States in July 2018, and is effective for financial audits, attestation engagements, and reviews of financial statements for periods ending on or after June 30, 2020, and for performance audits beginning on or after July 1, 2019. 5 Throughout this article, the terms “GAGAS” and “Yellow Book” are used interchangeably. 6 See Paragraph 1.06 of the Yellow Book. 7 See Paragraph 1.05 of the Yellow Book.

While the role of performance auditing has become more pronounced for audit institutions and state and local governments, especially in determining efficiency and promoting accountability, another product offering is available. The decision between the products can be confusing to both clients and practitioners: Operational assessments, which are in-depth, objective studies or analyses of an organization, can also be performed as non-audits, otherwise known as Consulting Engagements. These are a go-to for accounting firms that serve both corporate and government clients. Consulting engagements are aimed to serve management’s need for specific information or operational improvements when the effort required for an audit is not required. The client is the customer and the end user of the product, as opposed to a performance audit where the public or regulatory body, is the end user. The other important distinction between audits and consulting engagements is the end user of the work product and the client relationship. Consulting engagements are governed by the AICPA’s Statements on Standards for Consulting Services (SSCS) CS Section 100.02, which states that the nature and scope of work is determined solely by the agreement between the practitioner and the client. Generally, the work is performed only for the use and benefit of the client. The latter fact is what sets consulting engagements apart from performance audits. In consulting engagements – there are only two parties involved: the auditor and the client. There is a third party in government audits – the tax paying public or regulatory body, which are the primary beneficiaries of the product. It is important to make the distinction that consulting engagements are non-audit services and GAGAS does not cover these, other than under the topic of independence.

Other factors for consideration – audit vs. non-audit

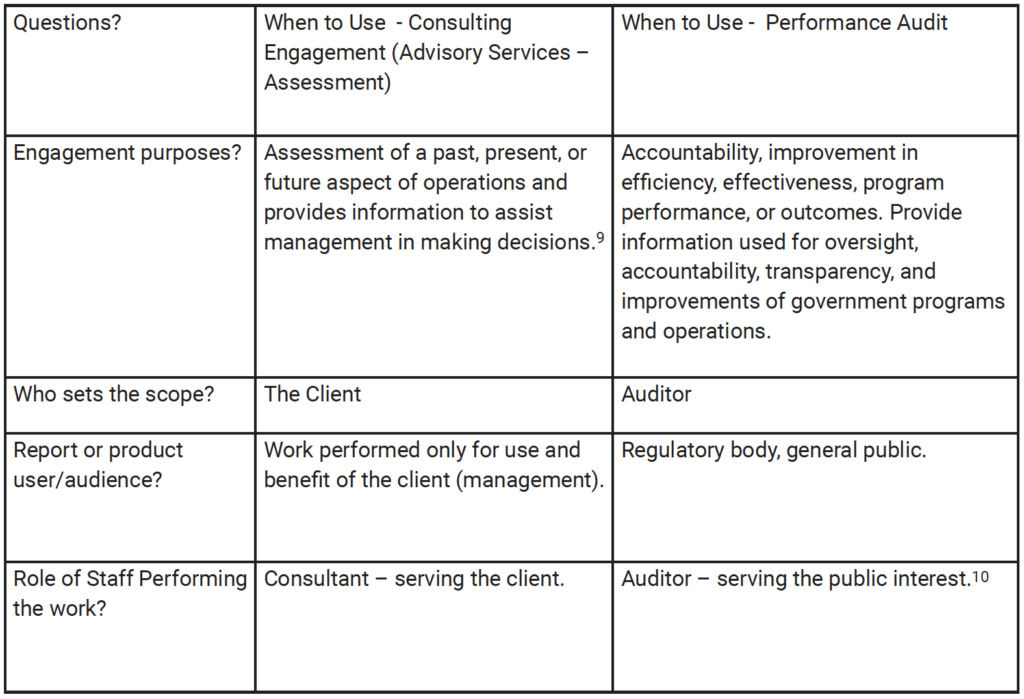

This leads to the most important factor in determining the engagement type – audit or non-audit. What is the purpose of the work (who, what are we looking at?) and the audience of the end product (who is it for?). Governmental audit reports routinely provide assurance to outside parties, especially the general public or other governmental entities.8 Performance audits typically provide historical perspectives of performance, compliance or efficiency, and effectiveness of a particular agency or program, or can provide prospective analysis. These audits are sometimes required by regulations, requested by legislators, and are aimed at determining compliance and/or program efficiency and effectiveness. Consulting engagements — non-audits — provide information, findings, or recommendations to benefit the client, and tend to be more forward-looking. Requests for these engagements typically come from internal management wanting to look into their own operations and for specific information. Sometimes just identifying the audience of the product will point to the appropriate engagement type. For example, if the end product goes nowhere beyond a client’s desk or is limited to distribution internally within a department, then a consulting engagement is preferable. Conversely, if the report will be seen by a governing board, or the intent is to make it a public document, an audit performed under GAGAS may be preferable when there is a need for accountability and recommendations for improvements in efficiency and effectiveness.

It helps to start with the intended user of the report: If it is strictly for management’s internal use, especially if there is a narrow scope of work that management has pre-determined, the non-audit option is preferable. The decision will then depend on factors as shown below. Figure 1.0 below provides an overview of a decision matrix to narrow down the determination of the best approach for the type of engagement. 8 Urton Anderson, Chapter 4 Assurance and Consulting services. 2003 Internal Audit Research Foundation.

Figure 1.0: Decision Matrix

The first major distinction between the two engagement types is the scope. While in a consulting engagement, the objectives are determined by management; in a performance audit, the scope is often determined by the auditor who determines coverage and depth depending on the time, cost, and other constraints. The second distinction lies in the requirement of preliminary work, such as the mandatory risk assessment, fraud questions, and internal control assessment. In a performance audit the auditor can determine the time period covered, sources of evidence, the population to be reviewed, and sample size rationale, and can focus the audit to address risk appropriately.11 These are key components auditors would normally determine in the planning phase of a performance audit, based on a preliminary assessment, risk assessment, and review of internal controls. All of these requirements allow the auditors to determine the focus of the audit as needed. 9 Urton Anderson, Chapter 4 Assurance and Consulting services. 2003 Internal Audit Research Foundation. 10 GAGAS 3.08: A distinguishing mark of an auditor is acceptance of responsibility to serve the public interest. This responsibility is critical when auditing in the government environment. GAGAS embodies the concept of public accountability for public resources, which is fundamental to serving the public interest. 11 See GAGAS paragraphs 8.05 through 8.19 for additional context.

GAGAS 8.16. “Audit risk is the possibility that the auditors’ findings, conclusions, recommendations, or assurance may be improper or incomplete, as a result of factors such as evidence that is not sufficient or appropriate, an inadequate audit process, or intentional omissions or misleading information because of misrepresentation or fraud. The assessment of audit risk involves both qualitative and quantitative considerations. Factors impacting audit risk include the time frames, complexity, or sensitivity of the work, size of the program in terms of dollar amounts and number of citizens served, adequacy of the audited entity’s systems, and processes for preventing and detecting inconsistencies, significant errors, or fraud, and auditors’ access to records.”

This is in contrast to consulting engagements where the scope is usually determined by management, and no preliminary work is required. In these engagements, management directs the scope, the time frame, and sometimes even dictates the methodologies to employ, or prescribes the sample size.

GAGAS provides consistency across audit organizations

GAGAS ensures consistency of the work for auditors and across the many audit organizations or private companies performing the work. For example, performance auditors are required to adhere to standards during the course of an audit; for instance, Fieldwork Standards. This does not represent the sum total of the requirements. The audit organization and audit team must also comply with a set of standards that include Independence, Quality Control, and Competency standards. With regard to how engagements are staffed, auditors must ensure that adequate and appropriate training occurs. They must exercise professional judgment while exhibiting ethical behavior and, most importantly, it is their responsibility to employ a system of quality control that ensures personnel comply with those professional standards.

The following GAGAS standards highlight what sets performance auditing apart from a consulting engagement and why a performance audit renders the preferable product when the public or regulatory body is the intended audience. Specific standards must be followed when conducting performance audits that serve to ensure sound, well-supported findings in the report, which make the case for change and improvements: Fieldwork Standards, Quality Control and Assurance, and Competence Standards. For each of these standards, the Consulting Standards do not provide detailed information for comparison.

Independence

The Independence standards are another key component in differentiating between a Consulting Engagement and a Performance Audit. In the government sector, performance audits are performed by auditors serving the public interest. GAGAS states that, “auditors and audit organizations maintain independence so that their opinions, findings, conclusions, judgments, and recommendations will be impartial and viewed as impartial by reasonable and informed third parties.12 Auditors should avoid situations that could lead reasonable and informed third parties to conclude that the auditors are not independent and thus are not capable of exercising objective and impartial judgment on all issues associated with conducting the audit and reporting on the work.” 13

Consulting engagements are performed by staff that also may conduct audits, but their role in a non-audit service is to serve the client. While objectivity and integrity are required, there is no concern for a lack of independence due to the nature of the work and, thus, Consulting Standards do not address independence. CSS 100.07 states (that staff), “Serve the client interest by seeking to accomplish the objectives established by the understanding with the client while maintaining integrity and objectivity.”

GAGAS does, however, take independence very seriously when it comes to auditors performing non-audit services, and requires that the auditors document that independence has not been compromised by applying the conceptual framework,14 that the client (management) has the skills, knowledge, and experience to oversee the work, and requires management to agree that they are responsible for the results of the consulting engagement.15,16

Fieldwork standards

Chapter 8 of GAGAS provides fieldwork requirements and guidance for performance audits. The purpose of fieldwork requirements is to establish an overall approach for auditors to apply in obtaining reasonable assurance that the evidence is sufficient and appropriate to support the auditors’ findings and conclusions. The fieldwork requirements for performance audits relate to planning the audit, supervising staff, obtaining sufficient, appropriate evidence, and preparing audit documentation. The concepts of reasonable assurance, significance, and audit risk form a framework for applying these requirements. Chapter 8 contains 141 paragraphs related to these sections.

Consulting standards SCSS 100.06 do not provide guidance for performing the engagement or a framework, but in bullet form, do require (1) planning and supervision; and (2) sufficient and relevant data.

Quality control and peer review

An organization that conducts performance audits shows commitment to performing quality assurance work, which can be recognized by the users of the reports, clients, potential clients, and the national standards setters. GAGAS states that each audit organization performing audits in accordance with GAGAS must: a) establish and maintain a system of quality control that is designed to provide the audit organization with reasonable assurance that the organization and its personnel comply with professional standards and applicable legal and regulatory requirements;1 and b) “must obtain an external peer review conducted by reviewers independent of the audit organization being reviewed.”18 The peer review allows an independent reviewer to look at the design of the audit organization’s system of quality control, and whether the organization is complying with its quality control system so that it has reasonable assurance that it is performing and operating in conformity with professional standards. In other words, these requirements ensure that quality control measures, such as policies and procedures, are in place within the organization that performed the audit, and that quality assurance activities are actually being performed on all audits.

12 GAGAS 3.22 13 GAGAS 3.19 14 See Paragraph 3.64 of GAGAS. 15 See Paragraph 3.76 of GAGAS. 16 See Paragraph 3.107 of GAGAS. 17 See Paragraph 5.02 of GAGAS. 18 See Paragraph 5.60 of GAGAS.

Competence and continuing professional education

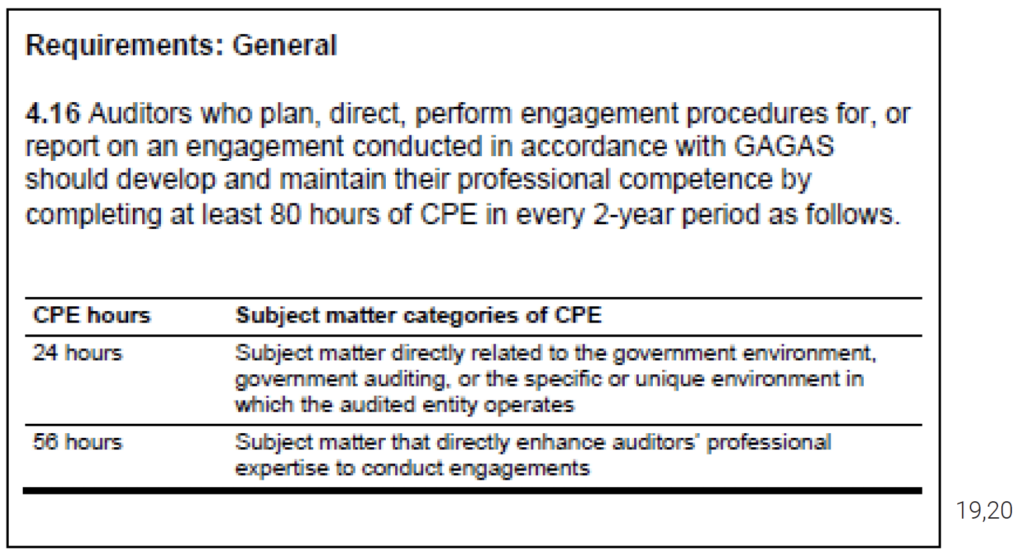

The competence requirements provide a guarantee to the client, and those relying on the audit that, in addition to independence and objectivity, staff assigned to the audit (1) have the knowledge of specific GAGAS requirements, as well as the skills and abilities to proficiently apply it to their work; and (2) are current with their continuing professional education requirements and have taken courses to enhance their skills. This ensures a team of staff with a high-level of competency appropriate for each staff level and specific government auditing related training; assigned to each audit. See below for GAGAS 4.16.

AICPA Consulting Standards have general competence standards; however, they are not detailed or specific in terms of type and total amount required. It is assumed that a CPA firm that provides consulting services has their own training requirements; and with CPAs on staff, they must obtain a certain number and type of continuing education depending on the state they are licensed in.

While the competency standards provide an added guarantee that staff performing the work have the required training and experience in government auditing, there is strength in an established multi-disciplinary team that conduct performance audits. Since performance auditing is more similar to program evaluation than financial audits, the staff that conduct performance audits often can have a broad range of educational backgrounds and training, and their experience or specializations provide additional value to the quality of performance audits. Career government auditors and evaluators often have graduate level degrees in Public Administration, Public Policy, Economics and Social Science backgrounds, with experience at federal and state auditor levels, as well as some traditional CPAs with governmental clients.

19 Therefore, each auditor performing work in accordance with GAGAS should complete, every 2 years, at least 24 hours of CPE that directly relates to government auditing, the government environment, or the specific or unique environment in which the audited entity operates. Auditors who are involved in any amount of planning, directing, or reporting on GAGAS engagements and auditors who are not involved in those activities, but charge 20 percent or more of their time annually to GAGAS engagements should also obtain at least an additional 56 hours of CPE (for a total of 80 hours of CPE in every 2-year period) that enhances the auditors’ professional expertise to conduct engagements. 20 See Paragraph 4.16 and 4.25 of the Yellow Book.

Conclusion

Government auditing serves a critical function for accountability and strengthens governance, while the application of GAGAS establishes a foundation for the credibility of the auditor’s work. Engagement quality assurance, peer review requirements, and competency requirements are the real “gold” behind a performance audit. Yellow Book standards assure the client that the findings were intensely scrutinized and sound, while the report is balanced and neutral. There is no question that governmental auditing or consulting of government programs or business units can add value in terms of providing an independent look into operations. While the performance audit framework can be useful when applied to other non-audit advisory engagements, such as a consulting engagement under the AICPA’s Statement on Standards for Consulting Services, there is no substitute for conducting a performance audit in accordance with the Yellow Book when it comes to public accountability of government entities

Author bios

Greta Bernard MacDonald, MPA Director, Macias Gini & O’Connell LLP

Ms. MacDonald has a Bachelor of Arts degree in Economics from California State University, Chico, and a Master of Public Administration from the University of Southern California. She has over 17 years of experience conducting performance audits according to GAGAS. Specifically, she has participated in over 35 performance audits according to GAGAS, in addition to performing dozens of other engagements leading, designing, and conducting risk assessments, operational and compliance audits of state and local government agencies, and non-profit organizations.

Scott P. Johnson, CPA, CGMA Partner, Macias Gini & O’Connell LLP

Scott Johnson has a combined experience of over 35 years working in the government industry, with over 24 years successfully overseeing government agencies’ internal service operations including: debt management, information technology, human resources, municipal finance, and budget. He has led large and mid-sized operations for California government agencies, including the cities of Santa Clara, Milpitas, San Jose, Oakland, and Concord and the County of Santa Clara. Scott is a past president of the California Society of Municipal Finance Officers (CSMFO), and a member of the AICPA Government Performance and Accountability Committee (GPAC). He is currently a partner with Macias Gini & O’Connell LLP (MGO), leading the Advisory Services sector specializing in State and Local Governments, based out of California.