Watch for unusual behavior patterns among employees.

Identify abnormalities in transactional data and audit trails.

Pay attention to whistleblower complaints and tips.

~

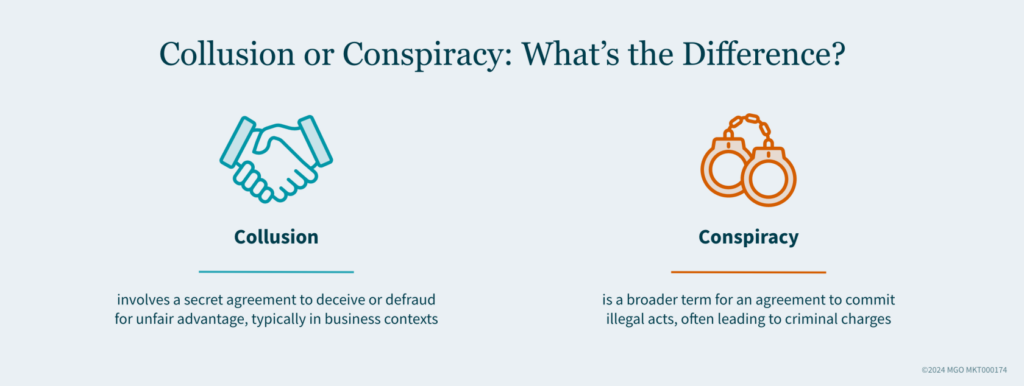

Collusion and conspiracy are serious threats that can undermine your business. Employees working together to deceive others can gain unfair advantages or harm the organization. To safeguard your business, it is crucial to recognize warning signs and implement proactive measures.

Signs of Collusion and Conspiracy

Keep an eye open for these red flags to protect your business:

1. Suspicious Behavior

Be alert to suspicious behaviors among employees. Frequent communication with external parties, secret meetings, or shared access to sensitive information can indicate collusion. These patterns often signal an intent to deceive or manipulate.

2. Unusual Patterns

Be mindful of any unusual patterns that may indicate fraudulent activities. Look for abnormalities in transactional data or audit trails. Missing documentation, altered records, or gaps in the chain of custody are warning signs. These irregularities can conceal fraudulent activities and hinder detection.

3. Changes in Relationships

Pay attention to sudden changes in employee relationships. New alliances between previously unrelated individuals or departments can indicate collusion. These shifts often aim to facilitate deceptive schemes. Businesses should be aware of these changes and investigate any unusual alliances that may form within their teams.

Proactive Measures to Prevent Fraud

Take these actions to defend your organization against the threats of collusion and conspiracy:

1. Evaluate Internal Controls

A lack of segregation of duties or internal controls can enable collusion. When employees can bypass checks and balances, they can perpetrate fraud schemes without detection. Strong internal controls are essential for preventing such activities. Evaluate your company’s internal controls to ensure duties are appropriately segregated and checks are in place.

2. Promote Whistleblower Policies

Take whistleblower complaints, tips, or allegations seriously. Reports of suspected fraudulent activities can provide critical insights. Encouraging a culture of transparency and accountability helps uncover and address collusion. Companies need to establish and promote effective whistleblower policies to ensure employees feel safe reporting suspicious behavior.

3. Review Data and Audit Trails

Your business should regularly review data and audit trails to identify and address any discrepancies promptly. By keeping a close watch on transactional data, you can detect irregularities early and take corrective actions to prevent fraud.

Strengthening Your Organization Against Internal Threats

Collusion and conspiracy pose significant risks, but vigilance and proactive measures can mitigate them. Recognizing red flags, strengthening internal controls, and fostering a culture of trust and ethical behavior help maintain your organization’s integrity. By being mindful of these behaviors, you can strengthen your company’s defenses against fraud and pave the path for long-term success.

How MGO Can Help

MGO provides the resources and experience to effectively address fraud, collusion, and conspiracy. With services including risk assessments, forensic accounting, policy development, and staff training, we can help you identify vulnerabilities, maintain compliance, and establish strong preventive measures.

This is the final article in our ongoing fraud series, “Alert Signals: Uncovering the Spectrum of Fraud,” aimed at educating businesses on identifying and preventing fraudulent activities. Read the previous articles in the series now:

Identify unexplained payments or gifts to officials as potential signs of bribery and corruption.

Monitor procurement for abnormalities like inflated pricing or bid rigging to maintain fair practices.

Maintain transparency in transactions to prevent undisclosed kickbacks or facilitation payments.

~

Maintaining integrity is paramount to the long-term success of any business. Yet, bribery and corruption remain pervasive issues across industries — undermining trust and fairness in transactions. Fraudsters exploit their influence in business dealings to gain illicit benefits for themselves or others, often at the expense of their employers and the rights of others.

Warning Signs of Bribery and Corruption

Recognizing the red flags of bribery and corruption is crucial for safeguarding your business. The signs may include:

Unexplained payments and gifts — Watch for unfamiliar payments, gifts, or gratuities to government officials, regulatory authorities, or business partners. These can be attempts to secure favorable treatment or influence decision-making processes. Such actions often violate ethical standards and legal regulations.

Lack of transparency in transactions — Be wary of undisclosed commissions, kickbacks, or facilitation payments. These hidden arrangements can mask corrupt practices and lead to significant financial and reputational damage.

Non-compliance with policies and regulations — It is essential to comply with anti-bribery and corruption policies, regulations, and legal requirements. Non-compliance can be a sign of deeper issues and can expose your organization to legal repercussions and loss of credibility.

Abnormalities in procurement processes — Pay attention to abnormalities in procurement, such as sole source contracts, inflated pricing, or bid-rigging schemes. These practices benefit certain vendors or individuals, undermining fair competition and integrity.

Unexplained changes in business practices — Sudden shifts in business relationships or unexplained changes in practices can indicate corrupt activities or unethical behavior. These changes often aim to conceal fraudulent activities and protect those involved.

Why You Should Address Fraud, Bribery, and Corruption

Navigating the complex landscape of fraud, bribery, and corruption requires careful guidance and robust systems. Here is why your organization should take a proactive approach to addressing these issues:

Fraud, bribery, and corruption can severely damage your company’s reputation and financial stability. Regular fraud risk assessments identify vulnerabilities in your business processes, enabling risk mitigation and asset protection.

Developing and implementing anti-bribery and corruption policies is crucial for maintaining ethical standards and legal compliance. Clear policies guide employee behavior and demonstrate your commitment to integrity and transparency.

Training and educating your staff on recognizing and reporting red flags empowers your team to act as the first line of defense against unethical behavior. A well-informed workforce helps maintain a culture of integrity. Continuous monitoring and regular audits are vital for ongoing compliance and detecting unethical behavior early. Vigilance prevents small issues from escalating into major problems.

By uncovering hidden fraud, you can address issues promptly and take necessary legal actions to safeguard your organization. Forensic accounting is essential for investigating suspicious transactions. The longer it takes you to uncover fraud, the greater the damage may be.

Bribery and corruption pose significant threats, but these risks can be managed with vigilance and proper support. Recognizing red flags and implementing strong anti-fraud measures can help your organization protect its integrity and foster trust among your stakeholders, employees, and customers.

How MGO Can Help

Equip your company with the resources needed to effectively address fraud, bribery, and corruption. With services ranging from risk assessments and forensic accounting to policy development and staff training, we can help you identify vulnerabilities, maintain compliance, and establish preventive measures. Reach out to our team today to learn more.

This article is part of our ongoing fraud series, “Alert Signals: Uncovering the Spectrum of Fraud,” aimed at educating businesses on identifying and preventing fraudulent activities. Read the previous articles in the series about detecting financial reporting fraud and asset misappropriation now. Stay tuned for more insights and strategies to protect your organization.

Asset misappropriation involves the theft or misuse of an organization’s physical and digital assets, posing a major threat to businesses.

Red flags of asset misappropriation include unexplained shortages, unauthorized transactions, altered records, excessive resource use, and employees living beyond their means.

Strategies to combat asset misappropriation include strong internal controls, employee education, surveillance technology, promoting an ethical culture, and data analytics for fraud detection.

~

In the dynamic landscape of modern business, asset misappropriation remains a pervasive threat, undermining the financial stability and integrity of organizations across industries. As part of MGO’s fraud series, this article delves into the critical issue of asset misappropriation — offering your business the knowledge and tools needed to safeguard your valuable assets.

Understanding Asset Misappropriation

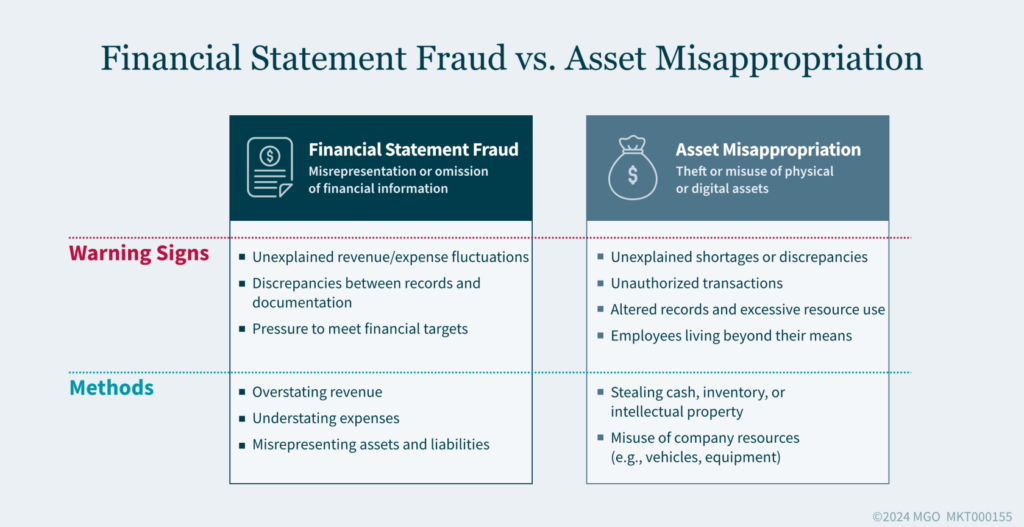

Asset misappropriation, a prevalent form of fraud, involves the theft or misuse of an organization’s assets. Unlike financial statement fraud, which distorts the truth on paper, asset misappropriation manifests in the direct pilfering or misuse of physical and digital assets. From cash and inventory to intellectual property and digital data, no resource is immune to this fraudulent activity.

Red Flags of Asset Misappropriation

Unexplained shortages or discrepancies:Whether it is cash, inventory, or other assets, unexplained shortages are classic signs of theft or embezzlement. For instance, casinos might notice discrepancies in chips or cash, pointing toward internal theft.

Unauthorized transactions: Any unauthorized withdrawals or transfers, especially in sensitive environments like casino accounts or gaming tables, should raise immediate concerns about asset misappropriation.

Alteration of records: Manipulating gaming records, player accounts, or payout systems can facilitate theft, often going unnoticed without rigorous audits.

Excessive use of company resources: When employees use company vehicles, equipment, or facilities beyond their professional needs, it suggests potential misuse of organizational assets for personal gain.

Lifestyle inconsistencies: Employees exhibiting a lifestyle significantly above their income level can be a red flag for embezzlement or fraud, often funded by stolen assets.

Strategies to Combat Asset Misappropriation

To effectively shield your organization from the perils of asset misappropriation, a multifaceted approach is necessary. These strategies are designed to fortify your defenses, helping your business operate with the highest standards of integrity and security. By implementing these measures, you can create a resilient barrier against fraudulent activities and safeguard your organization’s future.

Here are some pivotal strategies to combat asset misappropriation:

Establishing robust internal controls is the first line of defense. Professionals with experience enhancing internal controls can assist your organization in assessing and refining its practices — including segregation of duties, regular audits, and securing access to sensitive areas and systems. This approach establishes a solid foundation for preventing asset misappropriation.

Educating employees about the signs of fraud and the importance of ethical behavior is essential to deter potential fraudsters and empower your staff to report suspicious activities. Training programs, which can be supported by advisory firms, effectively communicate the risks of fraud and the importance of vigilance, helping to build a knowledgeable and proactive workforce.

Utilizing technology like surveillance cameras, advanced access controls, and cybersecurity measures can significantly reduce the risk of asset theft or misuse. Cybersecurity and physical security professionals can integrate cutting-edge solutions to protect your assets from both internal and external threats, providing a comprehensive defense strategy.

Promoting a corporate culture that values honesty and transparency can discourage fraudulent behavior. Developing policies and practices that foster open communication and a strong ethical foundation is crucial. Establishing a whistleblowing policy that encourages reporting without fear of retaliation can be an integral part of this effort.

Deploying data analytics and fraud detection software to monitor for unusual patterns or anomalies can indicate asset misappropriation. Advanced data analytics and forensic accounting services can identify and investigate suspicious activity, using sophisticated tools to detect early signs of fraud and prevent asset loss.

Safeguarding Your Assets Against Pervasive Threats

Asset misappropriation poses a significant risk to businesses, draining resources and eroding stakeholder trust. By understanding the red flags and implementing a comprehensive strategy to detect and prevent asset misappropriation, your organization can protect its assets and maintain its financial integrity.

This article is part of our ongoing fraud series, “Alert Signals: Uncovering the Spectrum of Fraud,” aimed at educating your business on identifying and preventing fraudulent activities. Read the previous article in the series on spotting red flags of financial reporting fraud and stay tuned for more insights and strategies to protect your organization.

Financial reporting fraud poses a significant threat by misleading stakeholders about a company’s true performance and financial health.

Warning signs that may indicate fraudulent financial reporting include unexplained fluctuations in revenues or expenses, discrepancies between financial records and supporting documentation, and intense pressure to hit financial targets.

Combating financial statement fraud requires strong internal controls, specialized fraud investigation support, and regular assessments to adapt to changing risks.

~

In the modern business environment, transparency and accuracy in financial reporting are not merely regulatory requirements — they are fundamental to maintaining stakeholder trust and ensuring the longevity of your organization.

Despite this, financial reporting fraud continues to pose a critical threat with far-reaching implications. It is a sophisticated malpractice, designed to create a facade of robust financial health by deliberately misleading stakeholders about a company’s performance, financial position, or cash flows.

Recognizing Common Red Flags of Financial Statement Fraud

Identifying financial statement fraud typically starts with noticing red flags, such as:

Unexpected revenue or expense fluctuations

Document mismatches (like ledger entries not aligning with system records or inconsistent invoices)

Undue pressure to meet financial targets

These signs — alongside vague financial reporting and insufficient disclosures — demand deeper investigation as they may indicate efforts to manipulate figures to present a misleading financial performance.

Understanding the Mechanisms of Financial Statement Fraud

At its core, financial statement fraud involves the manipulation of accounting records and financial statements. This can take several forms:

Overstating revenues — By recognizing revenue prematurely or recording fictitious sales, a company can appear more profitable than it is, misleading investors and creditors about its growth prospects.

Understating expenses — Deliberately delaying the recognition of expenses or not recording them at all inflates earnings, painting a picture of a company that is more efficient and financially stable than in reality.

Misrepresenting assets and liabilities — Overvaluing assets or not fully disclosing liabilities can significantly alter a company’s apparent net worth and financial solidity.

Each type of manipulation has one goal in common: to deceive users of financial statements. Whether it is investors, creditors, or regulators, the deception aims to create an illusion of success and stability, often for personal gain, to secure financing, or to maintain a company’s share price.

How You Can Combat Financial Statement Fraud

The fight against financial statement fraud requires a multi-faceted approach, encompassing the following measures:

Strong internal controls — Combatting fraud all starts with a strong internal control environment that includes checks and balances, rigorous accounting policies, and a corporate culture of integrity.

Fraud investigation support — Even with the best controls in place, the possibility of fraud cannot be eliminated entirely. This is where specialized fraud investigation services become indispensable. Advisory firms offer comprehensive fraud and litigation support that can uncover and address these fraudulent activities. Teams of professionals use forensic accounting techniques, data analysis, and investigative expertise to peel back the layers of financial deception.

Regular assessments — In addition to the services above, your business must also regularly evaluate its internal controls. It is not enough to have controls in place; they must be effective and adaptive to changing risks.

Recognizing the red flags of financial statement fraud and understanding its various forms are the first steps in prevention and detection. But beyond awareness, it is the proactive and reactive measures — strong internal controls, regular assessments, and skilled investigative support — that can help protect your company against such threats.

If you are looking to safeguard your financial integrity, services offered by third-party firms are invaluable assets in the continuous effort to uphold the truth in your financial reporting.

How MGO Can Help

MGO’s Business Advisory solutions offer a path to strengthen your organization’s financial defenses. For more detailed information on our approach and how we can help protect your business, let’s talk.

This article is part of our ongoing fraud series, “Alert Signals: Uncovering the Spectrum of Fraud,” aimed at educating your business on identifying and preventing fraudulent activities. Stay tuned for more insights and strategies to protect your organization.

Internal controls, especially around fraud prevention, are essential for limiting losses, driving efficiency, improving accountability, and boosting company value during investments or M&A deals.

The “tone at the top” from leadership in fostering an ethical environment, along with proper segregation of duties, are key elements for fraud prevention and strong internal controls.

Well-established policies and procedures, like Delegation of Authority rules and restricted system access protocols, are also vital for maintaining adequate controls to enable company growth.

~

As the economy stands on shaky legs, private equity and venture capital firms are necessarily careful and strategic when assessing potential investment opportunities. Whether your long-term plan includes acquiring another company, selling your business, or seeking new capital, strengthening your internal control environment — with a focus on preventing fraud — is a powerful way to increase actual and perceived value.

In the following, we will lay out the reasons why fraud prevention is an essential element to proper corporate governance and illustrate key areas to examine whether your internal control environment is built to help your operation succeed.

The Importance of Internal Controls in Fraud Prevention

A robust internal control system is the first step toward managing, mitigating, and uncovering fraud. A strong internal control environment will:

Protect your company’s assets by reducing the risk of theft or misappropriation of cash, inventory, equipment, and intellectual property.

Detect fraudulent activities or irregularities early on and deter employees from attempting fraud in the first place.

Provide cost savings by limiting opportunities for financial losses, costly investigations, and legal expenses associated with fraud.

Drive operational efficiency by providing clear processes and guidelines that reduce the risk of errors or inefficiencies in day-to-day operations.

Improve employee accountability by implementing checks and balances that discourage unethical behavior.

When seeking an investment or undertaking a significant M&A deal, you should have a firm grasp of the strength and quality of your internal control environment. Not only will you reduce the risk of fraud in the near term, but you will also cultivate confidence with potential investors and M&A partners.

Fraud Prevention Starts with the “Tone at the Top”

The first key element to look for in measuring the strength of your internal controls is ensuring a clear and proactive “tone at the top”, meaning an ethical environment fostered by the board of directors, audit committee, and senior management. A good tone at the top encourages positive behavior and helps prevent fraud and other unethical practices.

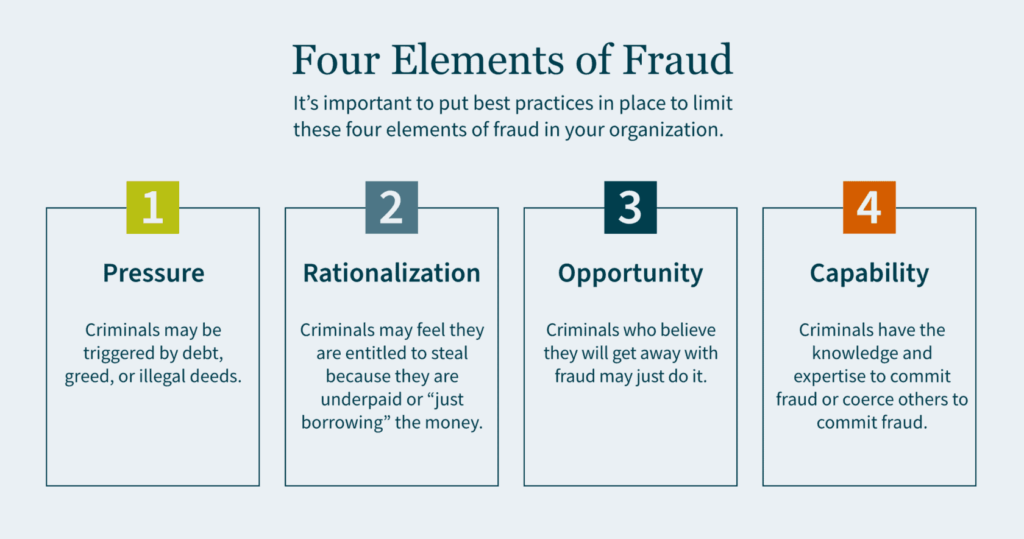

There are four elements to fraud: pressure, rationalization, opportunity and capability.

Pressure motivates crime. This could be triggered by debt, greed, or illegal deeds. Individuals who have financial problems and commit financial crimes tend to rationalize their actions. Criminals may feel that they are entitled to the money they are stealing, because they believe they are underpaid. In some cases, they simply rationalize to themselves that they are only “borrowing” the money and have every intention of paying it back.

Criminals who can commit fraud and believe they will get away with it may just do it. Capability means the criminal has the expertise as well as the intelligence to coerce others into committing fraud. The board of directors is responsible for selecting and monitoring executive management to ensure best practices are in place to limit the motivations of all four elements of fraud.

Proper Segregation of Duties for Internal Controls

The second key element to look for in your internal controls is a well-established segregation of duties. The idea is to establish controls so that no single person has the ability that would allow them the opportunity to commit fraud. Companies must make it extremely difficult for any single employee to have the opportunity to perpetrate a crime and subsequently cover it up.

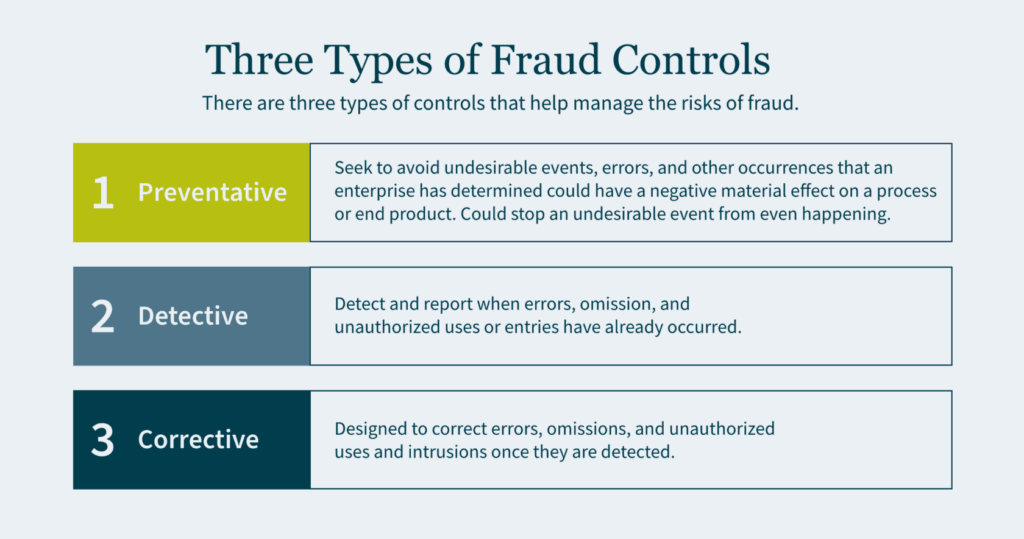

Fraud Controls

There are three types of controls that help manage the risks of fraud: preventative, detective, and corrective.

Preventative controls seek to avoid undesirable events, errors, and other occurrences that an enterprise has determined could have a negative material effect on a process or end product. Preventative controls are the best of the three as they are the first line of defense and a backstop to fraud. If designed correctly, preventative controls stop an undesirable event from even happening.

Detective controls exist to detect and report when errors, omission, and unauthorized uses or entries have already occurred. Although it is important to identify these adverse events, you are doing so after the fraud has already been committed.

Corrective (also referred to as compensating) controls are designed to correct errors, omissions, and unauthorized uses and intrusions once they are detected.

Preventing Misappropriation of Assets

An important component of segregation of duties is to prevent the misappropriation of assets and reduce fraud risk. Below are some examples of best practices for various types of assets:

Cash Receipt: segregate the receipt of cash/checks and the recording of the journal entry in the accounting system into two roles.

Accounts Receivable: segregate the responsibilities of recording cash received from customers and providing credit memos to customers. (If one person performs both functions, it creates the opportunity to divert payments from the customer to the employee and then cover the theft with a matching credit to the customer’s account).

Cash Reconciliation: the individuals who authorize, process, or record cash should not perform the bank reconciliation to the general ledger.

Inventory: individuals who order goods from the suppliers should not have the ability to log the goods received in the accounting system.

Payroll: segregate the responsibilities of compiling gross and net pay for payroll, with the responsibilities of verifying the calculation. (If a single individual performs both functions, it allows for the opportunity to increase personal compensation and the compensation of others without authorization. It also provides an opportunity to create a fictitious payee and make corresponding payroll checks).

The Importance of Policies and Procedures

The third key element to look for in your investees is well-established policies and procedures. Make sure that any company you consider acquiring has basic policies and procedures in place, such as Delegation of Authority (DOA).

The DOA is a policy where the executive team delegates authority to the management of the company. Individuals should be considered appropriate to fulfill delegated roles and responsibilities. The DOA should be reviewed at least annually. Subsequently, it is important to ensure that the DOA is being followed, and that approvals do not deviate from it. Any such anomalies should be rare and, when they do occur, they need to be reviewed and approved. Constant deviations from the DOA may be a sign that the DOA needs to be restructured.

A second essential policy and procedure is restricted computer and application access. This is to protect sensitive company financials and proprietary data. The company should have a robust control environment and maintain computer logins and password access on a need-to-know basis. Access should only be granted by the owner of the application or system and subsequently logged by the administrator. Now more than ever companies are hiring remote employees. This shift in the dynamic workspace further emphasizes the need for a quality IT controls environment.

How We Can Help

As you prepare your company for future growth, getting an impartial third-party opinion on your internal control environment can be a powerful tool for finding gaps and inefficiencies, and implementing value-added changes.

Our dedicated Public Company teams offer a deep level of industry experience and technical skills. We can help prepare your company for a major capital raise, including going public via an IPO or RTO. Or we can help optimize value for an M&A deal, whether you are buying or selling. Contact us today to access an external, holistic vision focused on helping you grow and succeed

A growing organization is a positive, but along with it usually comes increasingly complex financial accounting.

Outsourcing provides businesses of all sizes with an opportunity to manage an array of issues — from staffing shortages or a lack of specific expertise to disorganized or unsecure financial records.

Benefits of outsourcing include significant cost savings, direct access to specific accounting knowledge, the minimization of turnover, the ability to scale, access to tools and processes, and flexibility.

Many CEOs and business leaders are experiencing challenges in the aftermath of the COVID-19 pandemic, including changing customer trends, aggressive competition, emerging digital technologies, and the new normal of employee expectations for workplace flexibility.

These uncertain economic forces and cultural shifts are putting increased pressure on staffing for organizations of all sizes – especially fast-growing ones. While these difficulties are difficult to overcome, they are also an opportunity to change the “status quo” and level-up back-office performance.

For leaders navigating the uncertain tailwinds of the pandemic and planning to enter a new era of growth, outsourcing represents a powerful opportunity to address any staffing issues or business challenges. It empowers you to access specialized insight on a temporary basis, create value ahead of a major transaction, manage overhead costs, and modernize and revitalize business processes.

A recent study showed that 59% of all businesses utilize outsourced resources and that accounting is the most commonly outsourced function. So, how do you know if outsourcing your accounting function is right for your organization?

In this article we’ll look at five indicators that this strategy might be right for you and detail the key benefits to outsourcing or augmenting your accounting function.

Five signs your business may benefit from outsourced accounting

Here are some questions you should ask yourself to determine if your organization would benefit from outsourced accounting services:

Is your business growing rapidly?

If you’re experiencing a significant influx of revenue, first off, great work! Your business model is proving out and you’re on the fast-track to success. But what is happening to your expenses, profitability and working capital? Depending on your answer it could mean that your accounting needs are evolving, the risks of a breakdown are higher, and overall, there is simply more at stake. It may be time to confirm that your current in-house team is qualified and staffed appropriately to handle these new responsibilities.

Are you struggling to keep up with your accounts receivable or payroll?

One way to get a firm answer to whether your team is understaffed is if you’re missing key deadlines or struggling to get timely collection of cash from your accounts receivable. The inability to collect and follow-up on AR is essential to funding current and future growth and is directly connected to meeting your payroll commitments – one of the largest expenses of any business. If anything falls behind, you can find yourself in a difficult position if you do not have the ability to access cash or financing.

Are your financial records organized and producing usable data?

Your accounting function does more than compliance, it should help guide your organization’s financial hygiene. Organized financials tell a clear story of earnings, spending, and investment, so you can make informed decisions. An over-worked or inexperienced accounting team will be working furiously to keep up with compliance and may not have the capacity, or necessary experience, to provide guidance on your financial scorecard to accrete value to the organization.

Do your accounting needs fluctuate significantly throughout the year?

If your business experiences big shifts in labor productivity based on the calendar year and your taxes filings are late with significant overages from the tax preparers, or your audits have a significant number of adjustments, that may mean your accounting team lacks capability. Striking the right balance between hiring quality talent and the speed of bringing new hires up to date with company procedures can be a challenge. Outsourcing your team can deliver the resources you need, when you need them, and limit costs during the slower periods.

Are you concerned about financial security and checks and balances?

If your internal accounting team is one or two individuals, you may be open to hidden risks. An independent team can provide the checks-and-balances that help mitigate the risk of fraud and asset misappropriation.

If you answered yes to any of these questions, you should consider outsourcing part or all of your accounting function. With an outsourced accounting team, you gain immediate access to trained, knowledgeable staff with the knowledge you need in technical accounting. The right outsourced resources can help your business grow faster and run more smoothly — often at a lower price than building an internal accounting department.

Benefits of outsourced accounting services

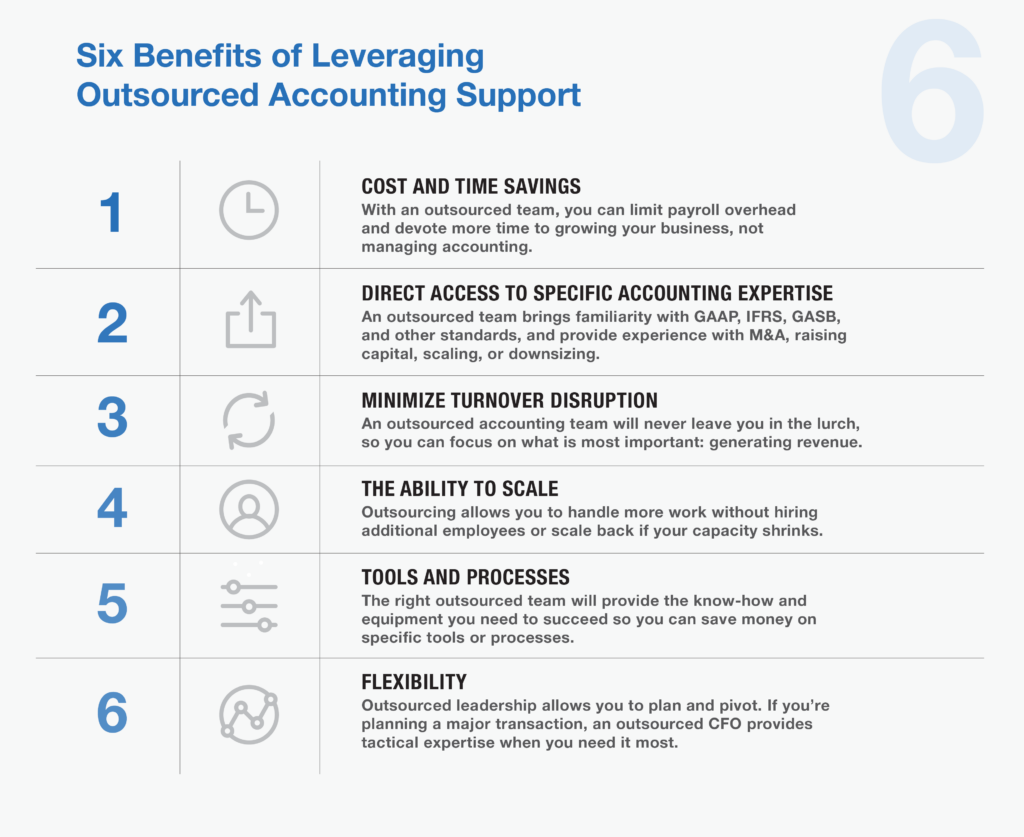

1.Cost and time savings

Maintaining full-time employees can be costly — and for most organizations, labor costs are some of the highest expenses. By relying on an outsourced team, you can devote your time to growing your business and spend less time managing accounting.

Direct access to specific accounting expertise

Every company is different, which means every company’s needs are different. By outsourcing, you have access to the service you need when you need it. An outsourced team will bring familiarity with an array of accounting and reporting standards, including GAAP, IFRS, GASB, etc. Plus, they can provide specific experience with M&A transactions, raising capital, scaling, or downsizing operations.

Minimize turnover disruption

In a smaller organization, each employee is vital to the business’s success. When you lose one, the disruption left in their wake can provide additional challenges. An outsourced accounting team will never leave you in the lurch, so you can focus on what is most important: generating revenue.

The ability to scale

If your organization has grown quickly, you may experience growing pains when your fortunes suddenly shift. In boom times, you may need to hire more staff to meet demand. But that also means you may find yourself laying off employees in a downturn. Outsourcing allows you to handle more work without hiring additional employees or scale back if your capacity shrinks.

Tools and processes

No matter what your organization’s size, you should always try to keep your overhead costs minimal. By outsourcing, you can save money on specific tools or processes you might otherwise need to function. The right outsourced team will provide the know-how and equipment you need to succeed.

Flexibility

By outsourcing certain jobs, you can plan — and pivot, as needed — depending on your organization’s needs. This is especially relevant in the case of needing specialized guidance. If you’re planning a major transaction or other market move, an outsourced CFO can provide tactical expertise when and where you need it.

MGO can help

As your organization grows, your financial accounting needs become increasingly complex. Because your in-house accountants may be limited to handle the basics, outsourcing to professional teams with specialized knowledge and experience can provide precisely the kind of service you require — and give you the time you need to focus on the organization’s other needs.

MGO has a robust outsourced accounting team staffed by CPAs with diverse industry background and technical specialties. We’ll provide the right-size solution to your organization’s needs. Areas we support include day-to-day accounting tasks, complex financial systems projects, regulatory compliance demands, and support for M&A deals, raising capital, and other major transactions.

Whether you’re interested in simply augmenting your team with additional financial knowledge, or undertaking a complete accounting transformation, we can help you with the people, processes, and technology you need to move your business forward.

To explore your options and start along the path to organizational change, contact us.

Often viewed as a “public company problem,” private organizations may want to consider implementing internal controls similar to Sarbanes-Oxley (SOX) Section 404 requirements. The inherent benefits of a strong control environment may be of significant value to a private company by providing: enhanced accountability throughout the organization, reduced risk of fraud, improved processes and financial reporting, and more effective inclusion of the Board of Directors.

Private organizations, while not always smaller, often have limited resources in specialty areas, including accounting for income tax. This resource constraint —the work being done outside the core accounting team — combined with the complexity of the issues, means private companies are ideal candidates for, and can achieve significant benefit from, internal controls enhancements. Thinking beyond the present, the following are five reasons private companies may want to adopt public-company-level controls:

1. Future Initial Public Offering (IPO) – Walk before you run! If the company believes an IPO may be in its future, it’s better to “practice” before the company is required to be SOX compliant. A phased approach to implementation can drive important changes in company culture as it prepares to become a public organization. Recently published reports analyzing IPO activity reveal that material weaknesses reported by public companies were disproportionately attributable to recent IPO companies. Making a rapid change to SOX compliance can place a heavy burden on a newly public company.

2. Merger and Acquisition Deals – If the possibility of the company being sold to an M&A deal exists, enhanced financial reporting controls can provide the potential buyer with an added layer of security or comfort regarding the financial position of the company. Further, if the acquiring firm has an exit strategy that involves an IPO, the requirement for strong internal controls may be on the horizon.

3. Rapid Growth – Private companies that are growing rapidly, either organically or through acquisition, are susceptible to errors and fraud. The sophistication of these organizations often outpaces the skills and capacity of their support functions, including accounting, finance, and tax. Standard processes with preventive and detective controls can mitigate the risk that comes with rapid growth.

4. Assurance for Private Investors and Banks – Many users other than public shareholders may rely on financial information. The added security and accountability of having controls in place is a benefit to these users, as the enhanced credibility may impact the cost of borrowing for the organization.

5. Peer-Focused Industries – While not all industries are peer-focused, some place significant weight on the leading practices of their peers. Further, some industries require enhanced levels of security and control. For example, cannabis companies with a heavy regulatory burden, industries with sensitive customer data like lifesciences, and tech companies that handle customer data, often look to their peer group for leading practices, including their control environment. When the peer group is a mix of public and private companies, the private company can benefit from keeping pace with the leading practices of their public peers.

Private companies are not immune from the intense scrutiny of numerous stakeholders over accountability and risk. Companies with a clear understanding of the inherent risks that come from negligible accounting practices demonstrate their ability to think beyond the present, and to be better prepared for future growth or change in ownership.

Welcome to the Cannabis M&A Field Guide from MGO. In this series, our practice leaders and service providers provide guidance for navigating M&A deals in this new phase of the quickly expanding industries of cannabis, hemp, and related products and services. Reporting from the front-lines, our team members are structuring deals, implementing best practices, and magnifying synergies to protect investments and accrete value during post-deal integration. Our guidance on market realities takes into consideration sound accounting principles and financial responsibility to help operators and investors navigate the M&A process, facilitate successful transactions, and maximize value.

Deal structure can be viewed as the “Terms and Conditions” of an M&A deal. It lays out the rights and obligations of both parties, and provides a roadmap for completing the deal successfully. While deal structures are necessarily complex, they typically fall within three overall strategies, each with distinct advantages and disadvantages: Merger, Asset Acquisition and Stock Purchase. In the following we will address these options, and common alternatives within each category, and provide guidance on their effectiveness in the cannabis and hemp markets.

Key considerations of an M&A structure

Before we get to the actual M&A structure options, it is worth addressing a couple essential factors that play a role in the value of an M&A deal for both sides. Each transaction structure has a unique relationship to these factors and may be advantageous or disadvantageous to both parties.

Transfer of Liabilities: Any company in the legally complex and highly-regulated cannabis and hemp industries bears a certain number of liabilities. When a company is acquired in a stock deal or is merged with, in most cases, the resulting entity takes on those liabilities. The one exception being asset deals, where a buyer purchases all or select assets instead of the equity of the target. In asset deals, liabilities are not required to be transferred.

Shareholder/Third-Party Consent: A layer of complexity for all transaction structures is presented by the need to get consent from related parties. Some degree of shareholder consent is a requirement for mergers and stock/share purchase agreements, and depending on the Target company, getting consent may be smooth, or so difficult it derails negotiations.

Beyond that initial line of consent, deals are likely to require “third party” consent from the Target company’s existing contract holders – which can include suppliers, landlords, employee unions, etc. This is a particularly important consideration in deals where a “change of control” occurs. When the Target company is dissolved as part of the transaction process, the Acquirer is typically required to re-negotiate or enter into new contracts with third parties. Non-tangible assets, including intellectual property, trademarks and patents, and operating licenses, present a further layer of complexity where the Acquirer is often required to have the ownership of those assets formally transferred to the new entity.

Tax Impact: The structure of a deal will ultimately determine which aspects are taxed and which are tax-free. For example, asset acquisitions and stock/share purchases have tax consequences for both the Acquirer and Target companies. However, some merger types can be structured so that at least a part of the sale proceeds can be tax-deferred.

As this can have a significant impact on the ROI of any deal, a deep dive into tax implications (and liabilities) is a must. In the following, we will address the tax implications of each structure in broad strokes, but for more detail please see our article on M&A Tax Implications (COMING SOON).

Asset acquisitions

In this structure, the Acquirer identifies specific or all assets held by the Target company, which can include equipment, real estate, leases, inventory, equipment and patents, and pays an agreed-upon value, in cash and/or stock, for those assets. The Target company may continue operation after the deal. This is one of the most common transaction structures, as the Acquirer can identify the specific assets that match their business plan and avoid burdensome or undesirable aspects of the Target company. From the Target company’s perspective, they can offload under-performing/non-core assets or streamline operations, and either continue operating, pivot, or unwind their company. For the cannabis industry, asset sales are often preferred as many companies are still working out their operational specifics and the exchange of assets can be mutually beneficial.

Advantages/Disadvantages

Transfer of Liabilities: One of the strongest advantages of an asset deal structure is that the process of negotiating the assets for sale will include discussion of related liabilities. In many cases, the Acquirer can avoid taking on certain liabilities, depending on the types of assets discussed. This gives the Acquirer an added line of defense for protecting itself against inherited liabilities.

Shareholder/Third-Party Consent: Asset acquisitions are unique among the M&A transaction structures in that they do not necessarily require a stockholder majority agreement to conduct the deal.

However, because the entire Target company entity is not transferred in the deal, consent of third-parties can be a major roadblock. Unfortunately, as stated in our M&A Strategy article, many cannabis markets licenses are inextricably linked to the organization/ownership group that applied for and received the license. This means that acquiring an asset, for example a cultivation facility, does not necessarily mean the license to operate the facility can be included in the deal, and would likely require re-application or negotiation with regulatory authorities.

Tax Impact: A major consideration is the potential tax implications of an asset deal. Both the Acquirer and Target company will face immediate tax consequences following the deal. The Acquirer has a slight advantage in that a “step-up” in basis typically occurs, allowing the acquirer to depreciate the assets following the deal. Whereas the Target company is liable for the corporate tax of the sale and will also pay taxes on dividends from the sale.

Stock/share purchase

In some ways, a stock/share purchase is a more efficient version of a merger. In this structure, the acquiring company simply purchases the ownership shares of the Target business. The companies do not necessarily merge and the Target company retains its name, structure, operations and business contracts. The Target business simply has a new ownership group.

Advantages/Disadvantages

Transfer of Liabilities: Since the entirety of the company comes under new ownership, all related liabilities are also transferred.

Shareholder/Third Party Consent: To complete a stock deal, the Acquirer needs shareholder approval, which is not problematic in many circumstances. But if the deal is for 100% of a company and/or the Target company has a plenitude of minority shareholders, getting shareholder approval can be difficult, and in some cases, make a deal impossible.

Because assets and contracts remain in the name of the Target company, third party consent is typically not required unless the relevant contracts contain specific prohibitions against assignment when there is a change of control.

Tax Impact: The primary concern for this deal is the unequal tax burdens for the Acquirer vs the Shareholders of the Target company. This structure is ideal for Target company shareholders because it avoids the double taxation that typically occurs with asset sales. Whereas Acquirers face several potentially unfavorable tax outcomes. Firstly, the Target company’s assets do not get adjusted to fair market value, and instead, continue with their historical tax basis. This denies the Acquirer any benefits from depreciation or amortization of the assets (although admittedly not as important in the cannabis industry due to 280E). Additionally, the Acquirer inherits any tax liabilities and uncertain tax positions from the Target company, raising the risk profile of the transaction.

Three types of mergers

1: Direct merger

In the most straight-forward option, the Acquiring company simply acquires the entirety of the target company, including all assets and liabilities. Target company shareholders are either bought out of their shares with cash, promissory notes, or given compensatory shares of the Acquiring company. The Target company is then considered dissolved upon completion of the deal.

2: Forward indirect merger

Also known as a forward triangular merger, the Acquiring company merges the Target company into a subsidiary of the Acquirer. The Target company is dissolved upon completion of the deal.

3: Reverse indirect merger

The third merger option is called the reverse triangular merger. In this deal the Acquirer uses a wholly-owned subsidiary to merge with the Target company. In this instance, the Target company is the surviving entity.

This is one of the most common merger types because not only is the Acquirer protected from certain liabilities due to the use of the subsidiary, but the Target company’s assets and contracts are preserved. In the cannabis industry, this is particularly advantageous because Acquirers can avoid a lot of red tape when entering a new market by simply taking up the licenses and business deals of the Target company.

Advantages/Disadvantages

Transfer of Liabilities: In option #1, the acquirer assumes all liabilities from the Target company. Options #2 and #3, provide some protection as the use of the subsidiary helps shield the Acquirer from certain liabilities.

Shareholder/Third Party Consent: Mergers can be performed without 100% shareholder approval. Typically, the Acquirer and Target company leadership will determine a mutually acceptable stockholder approval threshold.

Options #1 and #2, where the Target company is ultimately dissolved, will require re-negotiation of certain contracts and licenses. Whereas in option #3, as long as the Target company remains in operation, the contracts and licenses will likely remain intact, barring any “change of control” conditions.

Tax Impact: Ultimately, the tax implications of the merger options are complex and depend on whether cash or shares are used. Some mergers and reorganizations can be structured so that at least a part of the sale proceeds, in the form of acquirer’s stock, can receive tax-deferred treatment.

In conclusion

Each deal structure comes with its own tax advantages (or disadvantages), business continuity implications, and legal requirements. All of these factors must be considered and balanced during the negotiating process.

Time and time again we’ve seen reactions to various accounting scandals, after which new policies, procedures, and legislation are created and implemented. An example of this is the Sarbanes-Oxley Act (SOX) of 2002, which was a direct result of the accounting scandals at Enron, WorldCom, Global Crossing, Tyco, and Arthur Andersen.

SOX was established to provide additional auditing and financial regulations for publicly held companies to address the failures in corporate governance. Primarily it sets forth a requirement that the governing board, through the use of an audit committee, fulfill its corporate governance and oversight responsibilities for financial reporting by implementing a system that includes internal controls, risk management, and internal and external audit functions.

Governments experience challenges and oversight responsibility similar to those encountered by corporate America. Governance risks can be mitigated by applying the provisions of SOX to the public sector.

Some states and local governments have adopted similar requirements to SOX but, unfortunately, in many cases only after cataclysmic events have already taken place. In California, we only need to look back at the bankruptcy of Orange County and the securities fraud investigation surrounding the City of San Diego as examples of audit committees that were established in response to a breakdown in governance.

Taking your audit committee on the right mission

Governments typically establish audit committees for a number of reasons, which include addressing the risk of fraud, improving audit capabilities, strengthening internal controls, and using it as a tool that increases accountability and transparency. As a result, the mission of the audit committee often includes responsibility for:

Oversight of the external audit.

Oversight of the internal audit function.

Oversight for internal controls and risk management.

Chart(er) your course

Most successful audit committees are created by a formal mandate by the governing board and, in some cases, a voter-approved charter. Mandates establish the mission of the committee and define the responsibilities and activities that the audit committee is expected to accomplish. A wide variety of items can be included in the mandate.

Creating the governing board’s resolution is the first step on the road to your audit committee’s success.

Follow the leader(ship)

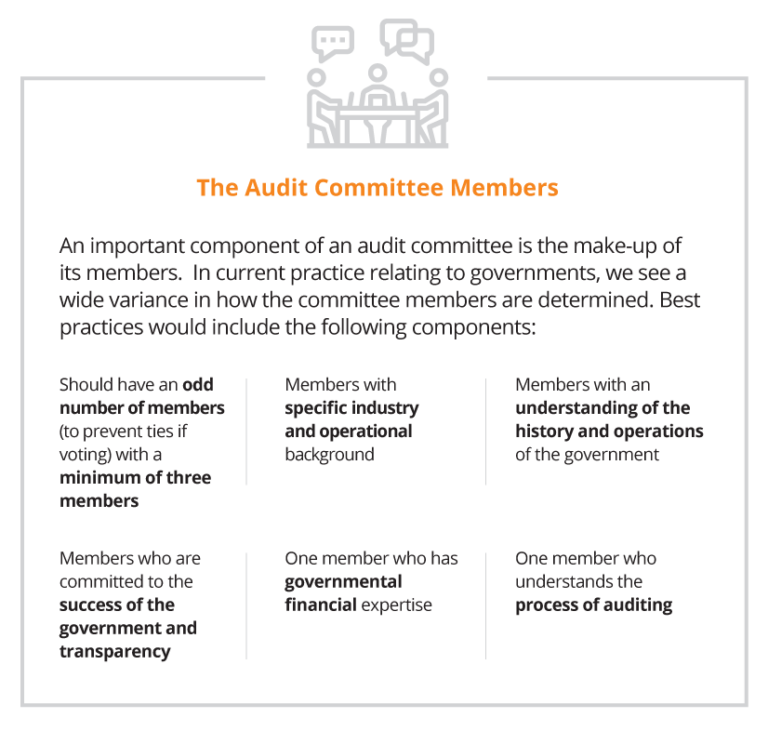

In practice we see a combination of these attributes, ranging from the full board acting as the audit committee, committees with one or more independent outsiders appointed by the board, and/or members from management and combinations of all of the above. While there are advantages and disadvantages for all of these approaches, each government needs to evaluate how to work within their own governance structure to best arrive at the most workable solution.

Strike the right balance between cost and risk

The overriding responsibility of the audit committee is to perform its oversight responsibilities related to the significant risks associated with the financial reporting and operational results of the government. This is followed closely by the need to work with management, internal auditors and the external auditors in identifying and implementing the appropriate internal controls that will reduce those risks to an acceptable level. While the cost of establishing and enforcing a level of zero risk tolerance is cost prohibitive, the audit committee should be looking for the proper balance of cost and a reduced level of risk.

Engage your audit committee with regular meetings

Depending on the complexity and activity levels of the government, the audit committee should meet at least three times a year. In larger governments, with robust systems and reporting, it’s a good practice to call for monthly meetings with the ability to add special purpose meetings as needed. These meetings should address the following:

External Auditors

Confirmation of the annual financial statement and compliance audit, including scope and timing.

Ad hoc reporting on issues where potential fraud or abuse have been identified.

Receipt and review of the final financial statements and auditor’s reports

Opinion on the financial statements and compliance audit;

Internal controls over financial reporting and grants; and

Violations of laws and regulations.

Internal Auditors

Review of updated risk assessments over identified areas of risk.

Review of annual audit plan, including status of the prior year’s efforts.

Status reports of ongoing and completed audits.

Reporting of the status of corrective action plans, including conditions noted, management’s response, steps taken to correct the conditions, expected time-line for full implementation of the corrective action and planned timing to verify the corrective action plan has been implemented.

Establish resources that are at the ready

Audit committees should be given the resources and authority to acquire additional expertise as and when required. These resources may include, but are not limited to, technical experts in accounting, auditing, operations, debt offerings, securities lending, cybersecurity, and legal services.

Taking extra steps now will save time later

While no system can guarantee breakdowns will not occur, a properly established audit committee will demonstrate for both elected officials and executive management that on behalf of their constituents they have taken the proper steps to reduce these risks to an acceptable tolerance level. History has shown over and over again that breakdowns in governance lead to fraud, waste and abuse. Don’t be deluded into thinking that it will never happen to your organization. Make sure it doesn’t happen on your watch.