Thorough documentation is essential for maximizing R&D tax credit claims by linking innovative projects to the required criteria set by authorities.

Critical documentation methods include maintaining project plans, reports, communications, time sheets, expense logs, and categorizing all records by project with clear dates.

To substantiate experimentation, continuously update digital records like lab notes and version-controlled documents to detail hypotheses, trials, iterations, findings, and modifications.

~

For companies in industries like manufacturing, biotech and life sciences, and technology, navigating the complex world of research and development (R&D) tax credits can be challenging. Thorough documentation is the key to maximizing your claim. Effective R&D tax credit claims hinge on robust documentation. Establishing the link between your innovative projects and the tax credit criteria set by authorities is non-negotiable.

Maximizing R&D Tax Credits: A Checklist for Robust Documentation

From ideation to execution, every step of your R&D project must be documented with precision. Follow these guidelines to assist your efforts:

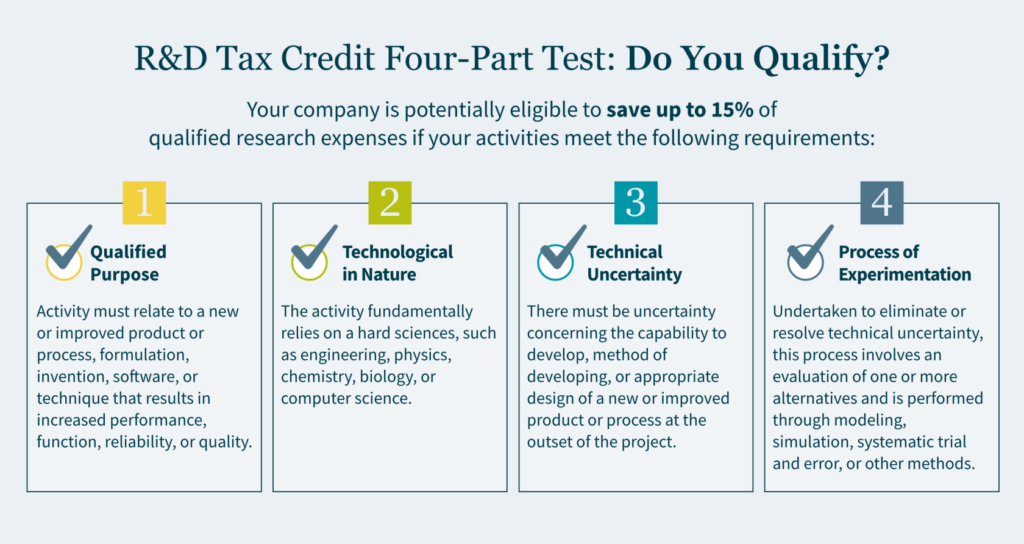

1. Foundation and Focus of Documentation

Lay the foundation for your R&D tax credit claim by aligning your innovative endeavors with the IRS’s qualifications. It is critical to consistently document every aspect of your projects, from initial goals and research stages to the hurdles you overcome and the novel outcomes you achieve. Your documentation needs to center on and address how your activities relate to the required four-part test: developing a business component, relying on science or technology, aiming to eliminate uncertainty, and involving a process of experimentation.

2. Documentation Methods and Best Practices

Incorporate a variety of records into your R&D documentation system — such as project plans, reports, and communications. For optimal organization, make sure each document is clear, concise, and bears a date stamp. Then categorize all documents by project, which aids in retrieval and review. Keep detailed records of project developments, discussions, and decisions to facilitate a straightforward audit process.

3. Tracking and Proving Your R&D Work

Maintain a log of your qualifying R&D activities and concurrent developments, clearly articulating how these relate to expenses. Accurate and up-to-date records like time sheets and expense logs are essential. Organize and categorize all R&D costs — from personnel and materials to outsourcing and cloud computing — employing accounting software for uniform expense coding. This methodical record-keeping is essential for connecting R&D endeavors with their associated costs, ensuring this support is available and complete in the event of an IRS audit.

4. Showcasing Experimentation

Substantiate technological progress with thorough records of your experimental activities. Continuously update digital records to reflect the evolving nature of your R&D projects, capturing each hypothesis, trial, and iteration. Make certain these digital records, like lab notes and version-controlled documents, comprehensively detail the experiments, findings, and any modifications to procedures or products.

Unlock R&D Tax Credits to Drive Your Business Forward

Navigating the intricacies of R&D tax credits is a continuous process that demands thorough documentation and strategic planning. By adhering to the four guidelines above and meeting the four-part test, businesses can not only ensure compliance but also maximize their potential benefits. As you embark on this journey, remember each detail documented is a step towards fostering innovation and technological advancement within your company.

MGO offers a comprehensive suite of strategic financial services to support your R&D endeavors. Reach out to us today to find out how we can help you.

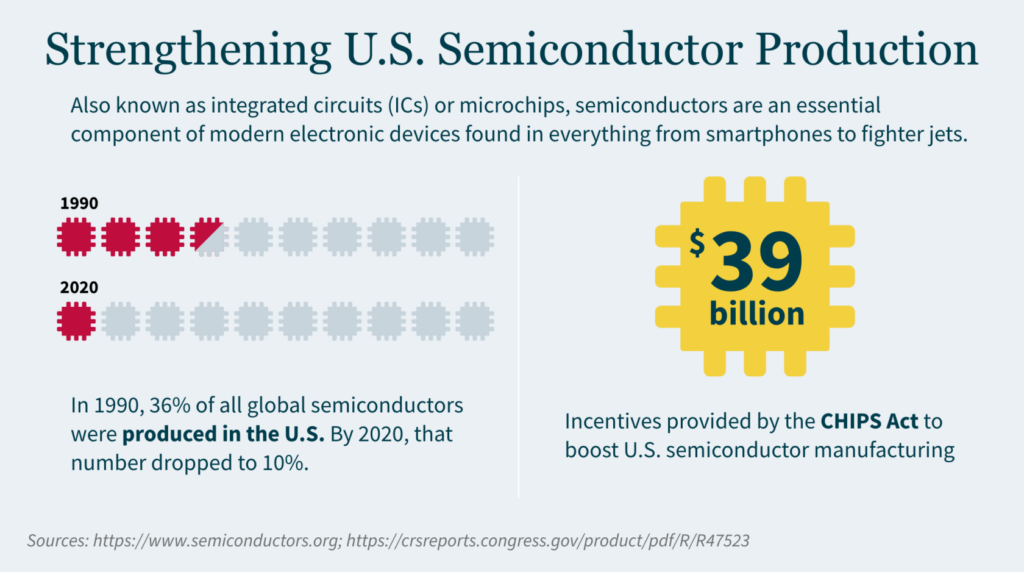

The CHIPS Act provides more than $50 billion to boost U.S. semiconductor manufacturing, including current funding opportunities for commercial fabrication facilities and advanced packaging research and development (R&D).

The Advanced Manufacturing Tax Credit (Section 48D) offers a 25% credit for qualified investments into semiconductor manufacturing facilities placed in service from 2023-2026.

Companies seeking CHIPS incentives or 48D credit should understand eligibility requirements, review application process details, and connect with specialized tax credits and incentives professionals to ensure maximum benefit.

Recently, the government awarded its first major CHIPS Act grant – providing $1.5 billion to GlobalFoundries, one of the world’s leading semiconductor manufacturers, to expand its semiconductor production in New York and Vermont. That grant is expected to be the first of several announcements in the coming months as the government ramps up CHIPS Act funding.

What is the Purpose of the CHIPS Act?

The intent of CHIPS is simple: the U.S. wants to incentivize domestic companies to manufacture semiconductors. The president called the CHIPS Act a “once-in-a-generation investment in America itself,” as the legislation aims to lower costs and create jobs in the production of these advanced chips.

The COVID-19 pandemic forced the semiconductor industry to operate at a reduced capacity, while lockdowns increased demand for products using semiconductors (computers, tablets, gaming systems, cars, etc.). This created a perfect storm, fueling a shortage of semiconductors. As a result, the U.S. recognized the need to increase its semiconductor output.

However, manufacturing semiconductors is not cheap and requires substantial investments. CHIPS, along with the available tax credit, encourages these investments.

The CHIPS Act includes provisions for:

$39 billion in incentives to build, expand, or modernize domestic facilities and equipment for semiconductor manufacturing, assembly, testing, advanced packaging, or research and development

$13.2 billion in R&D and workforce development

$500 million for international information communications technology security and semiconductor supply chain activities

Understanding the Advanced Manufacturing Tax Credit

With the addition of Section 48D to the Internal Revenue Code, CHIPS offers a new tax credit if your company invests in advanced manufacturing facilities or facilities whose primary purpose is manufacturing semiconductors or semiconductor manufacturing equipment.

Eligible businesses can receive a 25% tax credit of “qualified investments”. You can elect to treat the credit as payment against tax (i.e., direct pay) if you do not have sufficient tax liability to utilize the credit, making this essentially a refundable tax credit.

Eligibility criteria for 48D

To be eligible for 48D, you must have made a qualified investment for any taxable year integral to an “advanced manufacturing facility” for semiconductors placed in service during that year. Qualified properties must be:

Buildings, structural components, or parts of a building (not including administrative services or other functions unrelated to manufacturing)

Crucial to the operation of the advanced manufacturing facility

Constructed or built by the taxpayer

Qualified for amortization or depreciation

Taxpayers that use facilities and equipment outside the U.S. will not be eligible (similar to other investment credit requirements). Other taxpayers ineligible for the credit include:

Foreign entities noted as “foreign entities of concern” (i.e., foreign terrorist organizations or organizations included on the Office of Foreign Assets Control list).

Taxpayers that have engaged in significant transactions involving the material expansion of semiconductor manufacturing capacity in China or another foreign country of concern.

If a taxpayer enters a transaction in a foreign country of concern within 10 years of claiming the credit, it will be recaptured.

48D timing

The tax credit applies to any property placed in service after December 31, 2022, for which construction begins before January 1, 2027. It does not apply after December 31, 2026, nor can you use the tax credit for constructing a property after this date. If construction on a facility began before January 1, 2023, the credit applies only to the portion of the construction started after August 9, 2022.

Application process

In March 2023, the IRS issued proposed regulations addressing direct payment of Section 48D credit. The proposed regulations also require taxpayers to register through an IRS electronic portal before treating Section 48D as a direct payment on a tax return.

The IRS will issue a registration number for each qualified investment for which your company is claiming a credit, and that number must be included on your tax return.

CHIPS Incentive Opportunities

To access CHIPS incentives, your company must first apply for open funding opportunities. To date, the U.S. Department of Commerce has issued three Notice of Funding Opportunities (NOFOs) through the CHIPS for America program:

Application forms and instructions are available on the CHIPS Incentives Program application portal. FAQs, guides, and templates can also be found in the “Resources” section of the portal.

The application process includes the following stages:

Statement of interest

Pre-application (optional, but recommended)

Full application

Due diligence

Award preparation and issuance

Statement of interest – To submit a statement of interest, applicants need to register for an account on the CHIPS Incentives Portal. A statement of interest must be submitted at least 21 days prior to submitting a pre-application or full application.

Pre-application – The optional pre-application provides an opportunity to ensure your projects are consistent with program requirements. During this stage, you will receive feedback on strengths and weaknesses of your proposal and recommendations for improvement.

Full application – Both pre-applications and full applications are accepted on a rolling basis.

Due diligence – Your application will undergo review to ensure alignment with evaluation criteria specified in the Notice of Funding Opportunity (NOFO), with the possibility of requests for additional information.

Award preparation and issuance – Before receiving an award, you must have an active registration in the System for Award Management (SAM). It’s a good idea to begin the registration process for SAM.gov early as it may take anywhere from two weeks to six months (due to information verification requirements). Check out SAM.gov’s Entity Registration Checklist.

Maximizing Your Semiconductor Manufacturing Tax Credits and Incentives

Navigating CHIPS’s nuances can be challenging – especially when claiming the available tax credit and determining how it is refundable. Furthermore, companies seeking to increase their semiconductor manufacturing capacity in the U.S. should also assess application and opportunity for federal and state R&D tax credits and incentives.

With more than 30 years of experience, our dedicated Tax Credits and Incentives team can help you maximize your credit benefits, develop the appropriate documentation methodology, assist in calculating and claiming credits, and defend your claims. Our full-service firm, led by experienced CPAs and a

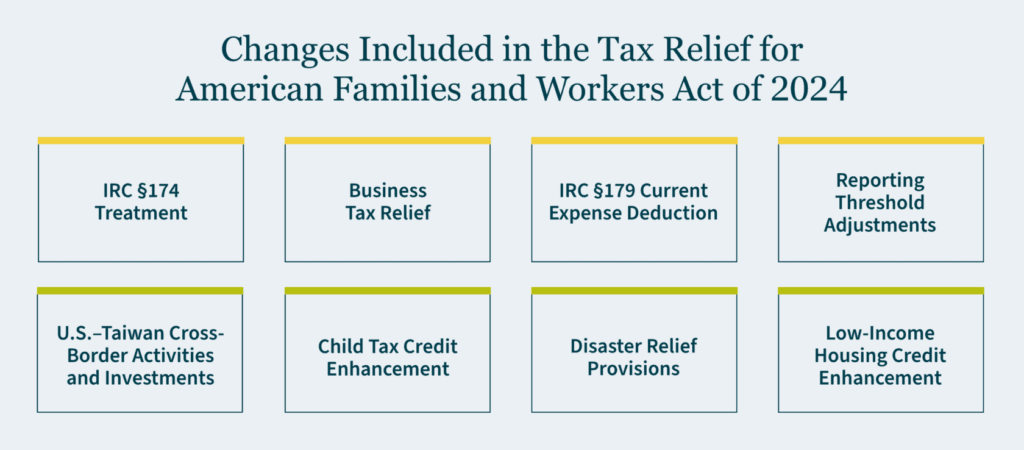

House Ways and Means Committee Chairman Jason Smith and Senate Finance Committee Chairman Ron Wyden announced agreement on a bipartisan tax framework to help families and main street businesses that is anticipated to be introduced as The Tax Relief for American Families and Workers Act of 2024. MGO will continue to monitor the development of the anticipated bill and proposals and provide related updates and information to our clients and network.

Here is a sneak peek into some of the expected goals of the tax framework:

IRC §174 Treatment

Boost innovation and competitiveness by allowing U.S. R&D expenses to be deducted in the year incurred — in comparison to the current 174 mandatory capitalization over five years, that has been in effect since the 2022 tax year. This change is anticipated to be retroactive to the beginning of 2022 and go through 2025. This should create an opportunity to decrease taxable income on an amended 2022 income tax return.

174 capitalization would still be required for foreign expenditures over 15 years.

Business Tax Relief

Retroactive deferral until 2026 of the reduction in the 100% bonus depreciation deduction.

Removal of depreciation, amortization, and depletion deductions from the calculation of adjusted taxable income for the IRC 163(j) business interest expense limitation. This change is also anticipated to be retroactive to the beginning of 2022 and be effective through 2025. This may create an opportunity to decrease taxable income and/or increase tax attributes for the 2022 tax year through an amended 2022 income tax return.

IRC §179 Current Expense Deduction

Increase in the maximum amount to $1.29 million and the investment limitation cap to $3.22 million for property placed in service in 2024, with inflation adjustments for post-2023 tax years.

Reporting Threshold Adjustments

Increase in the reporting threshold for filing Form 1099-NEC and 1099-MISC from $600 to $1,000, applicable to payments made after 2023, with inflation adjustments from 2024.

U.S.–Taiwan Cross-Border Activities and Investments

The bill creates a new section 894A of the Internal Revenue Code (“IRC”), providing substantial benefits to Taiwan residents (“qualified residents of Taiwan”), similar to those that are provided in the 2016 United States Model Income Tax Convention (“U.S. Model Tax Treaty”). Since the legislation requires full reciprocal benefits, it does not come into full effect until Taiwan provides the same set of benefits to U.S. persons with income subject to tax in Taiwan, similar to the reciprocal operation of a tax treaty.

Child Tax Credit Enhancement

Increase in the maximum refundable Child Tax Credit from $1,600 to $1,800 in 2023, $1,900 in 2024, and $2,000 in 2025.

Revision of the refundable portion, calculated on a per-child basis.

Disaster Relief Provisions

Retroactive exclusion of qualified wildfire relief payments from gross income.

Introduction of disaster-related personal casualty loss provisions and treatment of disaster relief payments for victims of the East Palestine, Ohio, train derailment.

Low-Income Housing Credit Enhancement

Enhancing the Low-Income Housing Tax Credit, by restoring the 12.5% LIHTC ceiling for taxable years beginning after December 31, 2022.

What should your business do in the meantime?

R&D/174 Proposed Changes – There likely is no immediate timeline sensitivity for the 174 capitalization requirement currently, unless you are a fiscal year filer or have an upcoming tax provision. In the event you have a return being filed in Q1, we recommend connecting with your tax credits service provider to discuss timeline for a formal analysis and processes. Please note that the anticipated changes are only to U.S. expenditures and therefore any foreign-based expenditures would still require capitalization over 15 years. A formal 174 analysis is recommended to support the research expenditures and to be able to apply the most favorable treatment of either immediately deducting or deferring, in the event of a bill passing and depending on whether the expense is a domestic or international expense.

It is also recommended to assess how the modification of the research and experimentation expense treatment would affect an amended 2022 return and forecasts for the 2023 tax year, especially for businesses that had material domestic research and experimentation expenditures. If all research and experimentation expenditures in the 2022 tax year were foreign, there will be no related change.

Other Business Tax Reliefs and Proposed Modifications – Please connect with your specialty tax service provider to discuss the timeline for your return filings and address forecasts and changes that may be created from these proposed changes. We have summarized a few recommendations and examples:

International

All U.S. citizens and U.S. resident taxpayers with activities within Taiwan should review their activities in light of these provisions to determine if reduced withholding taxes or minimization of creating a taxable presence is possible. All Taiwan residents with activities in the U.S. should review U.S. activities for similar issues.

Private Client Services

Assess how the proposed enhancements of the Child Tax Credit and Assistance for Disaster-Impacted Communities affect your personal deductions and 2023 tax liability.

State and Local Taxation

Evaluate variances in state conformity for the various changes. While some states have rolling conformity and will match changes at the federal level, others have fixed conformity and will not necessarily adopt these changes without further legislation.

Corporate Taxation

Evaluate the need to file an amended return to “unwind” the 2022 Sec. 174 research and development amortization to deduct those costs in full for 2022. This could provide significant refund opportunities.

Assess how the removal of depreciation, amortization, and depletion deductions from the calculation of adjusted taxable income for the IRC 163(j) business interest expense limitation affects taxable income and liability.

It is essential to note that despite this bipartisan breakthrough, the absence of an actual bill and the uncertainties surrounding the enactment of these provisions in a divided Congress should remain critical considerations.

Our perspective

As experienced advisors, MGO can help model the best position for you through the 2023 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors into not only the direct effects of the current legislation (i.e., the proposed tax framework summarized in this article), but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state and local tax) and what potential savings you can obtain by claiming credits and incentives. Please feel free to reach out to any of our MGO professionals below to get the experienced insight that you deserve.

Contact our leaders in the following areas for their specialty or to further address proposals in the tax framework discussed.

Despite bipartisan support, there have been no revisions to the Internal Revenue Code (IRC) Section 174 rules requiring that research and experimentation (R&E) expenditures be capitalized and amortized. Although a policy change that would have postponed this requirement to the 2026 tax year was proposed in last year’s Build Back Better Act (BBBA), that change was never enacted due to the BBBA stalling in the Senate. Subsequent to the BBBA, no other bills – including the Consolidated Appropriations Act (CAA), the final large legislation of 2022 – has been successful in incorporating Section 174 changes into their final versions.

What is the policy now? Well, the Tax Cuts and Jobs Act (TCJA) of 2017 changed the treatment of R&E costs so that taxpayers must capitalize all R&E costs incurred after December 31, 2021, and amortize them over either a five-year period (domestic costs) or a 15-year period (foreign costs). Previously, taxpayers could either (1) immediately deduct R&E expenditures, or (2) elect to amortize those costs over a period of five or more years, which gave the taxpayer the ability to choose the option that would be the most beneficial for them.

While it is still possible for the legislative process to postpone or repeal mandatory capitalization of Section 174 costs (including retroactively applying any changes to the 2022 tax year), such legislation would need to have bipartisan support due to the currently divided Congress.

In this article, we review what it would mean for your business if the much-anticipated revisions to Section 174 do not occur, and what kind of planning you should do to prepare on the front end. A number of these recommendations will be further refined once additional IRS guidance is provided.

Background on 174 R&E expenditures

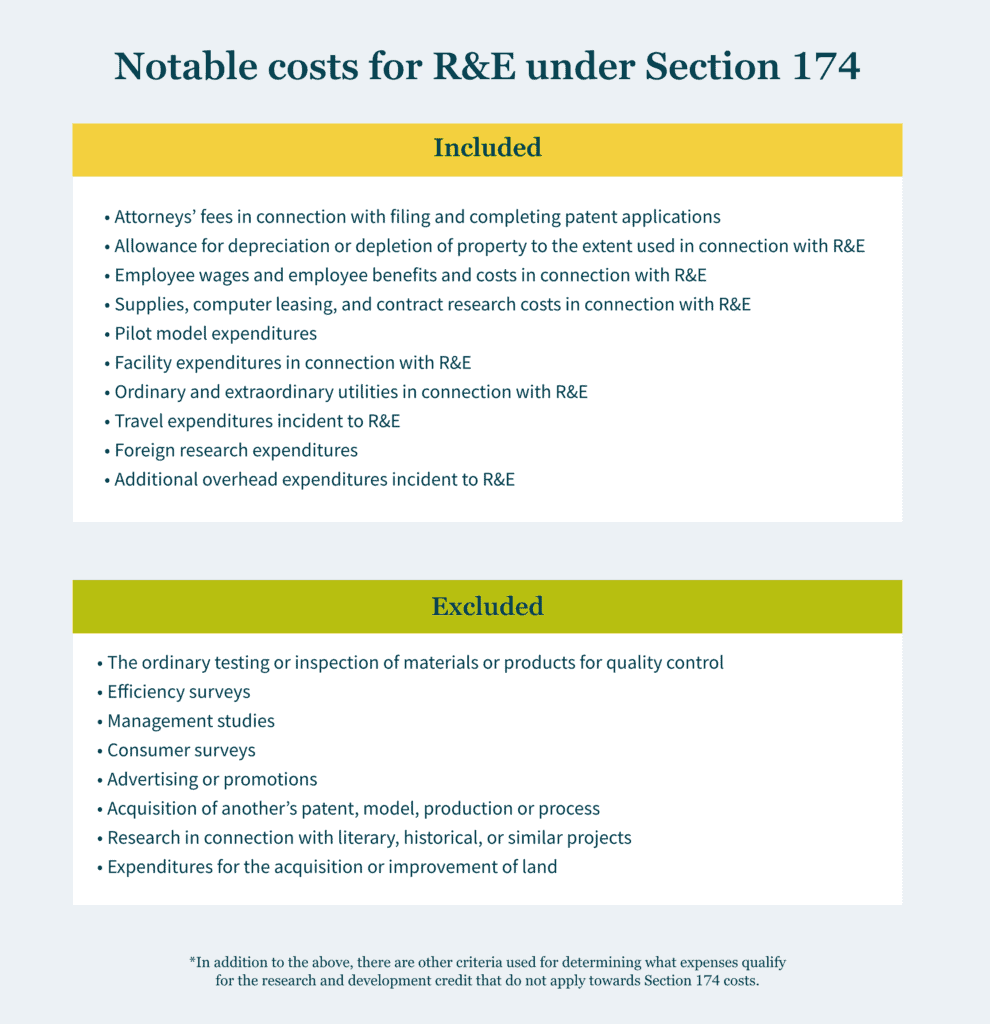

R&E expenses for income tax purposes are defined under Section 174 and its regulations. In Treasury Regulation Section 1.174-2(a), R&E expenditures are described as expenditures incurred by the taxpayer in connection with the taxpayer’s trade or business in the experimental or laboratory sense. Section 174(c)(3) – added by the TCJA – also notes that any amount paid or incurred in connection with the development of any software shall also be an R&E expenditure subject to capitalization. Generally, when determining R&E expenses, not only are direct costs of R&E factored in, but also the indirect costs incident to the development or improvement of a product.

Common expenses included in R&E costs under Section 174 are the following. Many of these expenses are considered for Section 174 specifically and are not qualified research expenses for purposes of the R&D credit.

Attorneys’ fees in connection with filing and completing patent applications.

Allowance for depreciation or depletion of property to the extent used in connection with R&E.

Employee wages and employee benefits and costs in connection with R&E.

Supplies, computer leasing, and contract research costs in connection with R&E.

Pilot model expenditures.

Facility expenditures in connection with R&E.

Ordinary and extraordinary utilities in connection with R&E.

Travel expenditures incident to R&E.

Foreign research expenditures.

Additional overhead expenditures incident to R&E.

*In addition to the above, there are other criteria used for determining what expenses qualify for the R&D credit that do not apply towards determining Section 174 costs.

In contrast, the following are common expenses that are excluded from the expansive definition of R&E costs under Section 174:

the ordinary testing or inspection of materials or products for quality control;

efficiency surveys;

management studies;

consumer surveys;

advertising or promotions;

acquisition of another’s patent, model, production or process;

research in connection with literary, historical, or similar projects; and

expenditures for the acquisition or improvement of land.

The current R&E amortization rule explained

The ability to deduct R&E costs changed for all tax years beginning after December 31, 2021. As previously mentioned, these costs can no longer be deducted in full and must be capitalized and then amortized over five years for domestic costs and over 15 years for foreign costs. This amortization starts at the midpoint of the first year that the expenses were incurred, which results in only 10% of domestic costs (1/2 of 20%) being able to be deducted in their first year.

Per IRS guidance, this mandatory change can be implemented as an automatic accounting method change through attaching a statement to a taxpayer’s first income tax return with a year beginning after 2021, in lieu of filing the much more intricate Form 3115. This change should not have an effect on prior tax years, since the automatic method change is implemented on a “cut-off basis.”

Macro effect of mandatory capitalization

As mentioned above, before the prior rule was changed, every R&E expense could be deducted in full in the year they were incurred. While it is expected that the Section 174 expensing rules will revert to this — to some extent — through pressure from persistent lobbyists, this change has not been incorporated into a bill yet.

Some believe the mandatory R&E capitalization and amortization will adversely affect U.S. innovation, potentially resulting in a detrimental impact on our global competitiveness and jobs. For more than 60 years, businesses were able to immediately deduct their R&D expenses in the year those expenses were incurred (or choose to defer based on what worked for them). Now, the amortization of new R&E costs could cost businesses billions in cash taxes.

Significant considerations

Estimated Tax Payments: For taxpayers making estimated tax payments utilizing current year taxable income, consideration should be given to R&E expenditures and how the capitalization of those expenditures may impact taxable income and timing of cash tax payments. A closer look at refining the various accounts in a taxpayer’s books may be needed for this.

Tax Accounting / ASC 740: Taxpayers should be mindful of whether a new deferred tax asset is created, if any adjustment of existing deferred taxes may be necessary, or if a full or partial valuation allowance may be needed.

Other Areas Affected: The amortization requirement also affects other areas of taxable income, including the following:

increases the deductibility of business interest under Section 163(j),

increases the deductibility of the QBI (Qualified Business Income) deduction,

increases the amount of GILTI (global intangible low-taxed income) for controlled foreign corporations,

potentially adjusts the amount of FDII (foreign derived intangible income) deduction that can be taken,

changes the amount of R&E expenses allocable for purposes of the foreign tax credit, and

impacts state taxable income for the few states that do not conform to the capitalization requirement (e.g., California).

R&D credit considerations

The Section 174 capitalization requirements should not directly impact the amount of expenses that can be used for the R&D Tax Credit under Section 41, since the research credit is calculated using a much smaller subset of R&E expenditures than Section 174 and is not limited by the capitalization requirement. As Section 174 is much broader in scope, it applies to expenditures both eligible and ineligible for the research credit.

Another consideration for tax planning is that the research credit will be even more important to assist with reducing the additional tax liability that will be generated by the R&E treatment change, since the credit can help offset some of the tax liability increase. Moreover, the analysis & processes used to determine the R&D credit can be leveraged to identify Section 174 R&E expenses, which helps create some efficiencies in quantifying the overall effect of the mandatory capitalization and amortization requirement.

Extend impacted returns where possible

Tax return extensions are highly recommended for tax returns that have their due dates coming up. Not only is there the pending IRS guidance that may significantly change R&E expense calculations, but also the act of extending tax returns should allow more time for tax returns to be superseded (rather than amended) and should allow for R&D credit claims to be made on originally filed returns.

This is echoed by a September 2021 Chief Counsel Memorandum issued by the IRS, which made the process for claiming a refund under the R&D credit far more stringent. The memorandum relayed that taxpayers must provide more information on business components, identify the research activities performed, and name the individuals who performed each research activity. Given the additional amount of detail needed, taxpayers making R&D credit claims on amended returns — especially small businesses — have a heavier burden than those who make the claim on an originally filed returns.

How will it affect you?

If the mandatory R&E capitalization requirement is not changed, you should consider how the 174 capitalization rules will affect your business and how claiming the R&D credit will help offset the increase in tax liability. If you currently have an R&D credit analysis and/or an ASC 730 financial statement analysis, those studies can be used as starting points to determine the overall effect of Section 174 — keeping in mind that neither analysis includes all the costs included in Section 174.

If the requirement is changed, there are several ways that the R&E expense landscape could turn out for taxpayers. Ideally, Congress will revert to the prior rule regarding R&D expenses. In that situation, you should be able to choose what is best for you — immediately deducting or deferring.

Our perspective

As experienced advisors, MGO can help model the best R&E position for you, through the 2022 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors not only the direct effects of the R&E capitalization requirement, but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state, and local tax) and what potential savings you can obtain by claiming the R&D credit. Please feel free to reach out to any of our R&E costing professionals below to get the experienced insight that you deserve.

About the author

Danielle Bradley is a senior manager in MGO’s National Tax Credits and Incentives practice. She focuses on helping businesses identify, substantiate, and defend federal and state tax credits and incentives. She has helped hundreds of companies monetize and defend over $100 million in various tax credits and incentives, such as the Research and Development (R&D) Tax Credit, Orphan Drug Credit, Employee Retention Credit, meals and entertainment deduction, and the current Research and Experimental (R&E) amortization calculations. Danielle has extensive experience in various industries, including software and technology, life sciences, manufacturing, aerospace and defense, and food, beverage and agriculture businesses.

Contact Danielle to further discuss the R&E amortization or other credits and incentives at Danielle Bradley or Michael Silvio (Tax Partner).

Recent events in the media have shone a spotlight on issues surrounding bad practices when it comes to tax credits and incentives. This increased attention is likely to result in an influx of audits by the Internal Revenue Service (IRS) as they crack down on the Research and Development (R&D) tax and the Employee Retention Tax Credit (ERTC) in the coming years.

We recently released an article detailing the red flags to look out when dealing with tax credits and incentives providers. If you think you could be at risk for future IRS issues, there is much you can do now to take a proactive approach and mitigate future negative impact. In the following, we break down steps you can take now to better understand and manage your exposure.

An overview of tax credits and incentives

Designed to encourage investment and development, job creation, growth, and certain business activities, tax credits and incentives provide an opportunity to reduce the amount of tax owed for performing certain activities. Credits and incentives are categorically different than tax deductions, which reduce the amount of taxable income.

These incentives often target desirable industries or activities like research and development, job creation for at-risk populations, and expanded growth in underdeveloped areas. When leveraged correctly, credits and incentives can be a powerful tool to funnel back resources into your organization to fuel activities you are already doing. Even more enticing, these credits can often apply retroactively if you determine you qualify for certain credits or incentives after the fact.

There are three basic types of tax credits: nonrefundable, refundable, and partially refundable. A few of the different types of tax credits pertaining to businesses in different classifications, industries, or activities performed include R&D tax credits, the employee retention tax credits, IRC Section 179D, and the work opportunity tax credit. To learn more about their eligibility rules, visit our previous article.

Understanding the risk of IRS tax audits

There is a three-year statute of limitations from the due date of the tax return or the filing date (whatever is later) for the IRS to assess your filings. That means if you think you may be exposed but escaped the IRS’ notice, you could still receive an audit notice for previous years’ returns. And if you do get audited, and the IRS determines you owe back taxes, you will get charged penalties and interest dating back to the infraction itself.

This is even more risky when considering the IRS’s extreme backlog. These IRS tax audits can sometimes take years to complete and if your credit and incentive calculations are the topic of interest, you’ll need to halt any future credit analysis until the situation is resolved. Meanwhile, you’ll be devoting crucial resources, time, and effort working with the IRS for something that yields no financial value and distracts from more conducive business activities.

Reasons to get a head-start and address issues now

Even though there is no guarantee you will get audited, you are still taking a risk if you do not address potential tax credit and incentive exposures in your organization. It may seem easy to “roll the dice” and hope the issue will remain uncovered, but it could come at a cost — especially if you are planning to make some big moves, like engaging in transaction of your business (M&A), going public, or embarking on another major transaction.

During the due diligence period of these transactions, it is almost certain any uncovered tax issues will emerge. You will likely not recover the value of these credits or remain on the hook for potential liability. Even worse, the exposure of these issues reflects negatively on your accounting and control system, potentially lowering the purchase value of your organization or undermining whatever deal you had in place prior to the due diligence. Often your transaction partners will start to question your organization’s trustworthiness, and reputation … due to something that may be no fault of your own.

So, you’ve been exposed … but haven’t received an IRS audit notice

Here is the deal: you know for certain you have been exposed, but you have not been notified by the IRS yet. You probably have a lot of questions — will you get an audit notice? Have you escaped unscathed? Do you need to address the issues preemptively, just in case? It may be overwhelming to decide how to proceed once you realize the exposure.

We suggest working with a qualified CPA firm to review your tax filings. A full-service accounting firm will review your organization holistically at a minimum rate, uncover any exposures, and deliver valuable peace of mind. If the firm does find issues, you have two options:

Update your credit and incentive filings moving forward.

While this will likely decrease the amount you can deduct, it exemplifies transparency.

Issue a Voluntary Disclosure (VA) if the exposure is significant and you do not have a lot of time to fix the issue.

Essentially, you are volunteering to correct your mistakes by recalculating the credits claimed and paying back the difference.

While this may sting a little, the IRS looks favorably upon organizations who are proactive to fix the issue by filing a VA and they are likely to waive any penalties or interest you would have had to pay.

You’ve received an IRS audit notice. Now what?

Well, it happened. You received an audit note from the IRS. Before you panic, here is what you need to do:

Start preparing your documentation right away. The sooner you have your ducks in a row, the sooner you are prepared to handle the audit.

Check the contract you signed with your original provider and verify if they provide controversy support services for situations like these.

If they do, reexamine the quality of their work. Do they have any of the red flags mentioned in this article? Could something they have done have caused the audit?

Consider engaging a qualified CPA firm as your new provider to handle the subsequent controversy support. Someone you trust can get you ready for any available credits and incentives moving forward, too.

If you used a provider that displays any red flags, you could have some leverage for a reasonable cause defense. Because the “professional” firm handled it for you and made a mistake, you could utilize a first-time penalty abatement, which means you can get relief from a penalty if you:

Did not previously have to file a return or if you do not have any penalties for the three years before the tax year you received a penalty;

Filed all currently required returns or an extension of time to file; and

Paid or have arranged to pay any tax due.

Verify your contract with the original provider to determine if you have any recourse to seek compensation from them. If the IRS does issue any penalties, you will want to ensure you do not have to pay.

Standalone firms vs. full-service accounting firms

Let’s say you haven’t received an IRS notice, and you do not think you are in danger of receiving one. How can you ensure you will not in the future? It comes down to choosing a firm to help you maximize the potential of these tax credits and incentives.

The bottom line: it is imperative you work with a certified public accounting (CPA) firm instead of a standalone firm. Because standalone firms often use lower-cost, less-experienced recent graduates who are not certified public accountants, there is a distinct lack of knowledge and background in the accounting fundamentals, causing you to be misled by those unequipped to help with complex tax matters. You also run the risk of being oversold benefits by aggressive firms that not only exaggerate the amount you are receiving from the tax credits and incentives, but also behave in a way that attracts IRS attention and jeopardizes your firm.

A full-service accounting firm, on the other hand, knows how to look at an organization holistically — and it has many more capabilities and professionals with experience. It looks at things through various lenses and can advise how certain positions will impact current and future tax positions. Full-service firms also likely have an in-house controversy team that has handled hundreds of audits successfully—so you will be in good hands.

Our perspective

Tax credits and incentives provide plenty of benefits you do not want to miss out on, and their often-complex application and qualification processes are reason enough to hire a professional accountant to help you maximize your returns. Unfortunately, we often see organizations placing their trust in the wrong providers and they end up suffering the consequences of an IRS audit. For many, it is simply easier and safer to cut off the relationship with the initial provider and start fresh with a professional firm you know you can trust.

At MGO, our dedicated Tax Credits and Incentives team brings more than 30 years of experience fixing these types of issues and working with the IRS to limit the damage. We provide cleanup in the event you are being audited by the IRS (or could be audited in the future), and help you identify areas where you can claim tax credits and incentives for next time. If you are concerned, our best advice is to get ahead of it with an opinion you can trust — before the IRS decides to investigate themselves.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

On October 15, 2021, the Chief Counsel’s office released memorandum number 20214101F in response to questions from IRS officials in the Large Business & International division and the Small Business/Self-Employed division about what information taxpayers should provide with their claims for refunds or tax credits and what format they should use.

What qualifies a taxpayer for the R&D refund claim?

In short, the IRS stated that for a taxpayer’s R&D refund claim to be valid, the taxpayer must, at a minimum:

Identity all the business components to which the I.R.C. § 41 research credit claim relates for that year.

For each business component:

identify all research activities performed,

identify all individuals who performed each research activity, and

identify all the information each individual sought to discover through the activities performed.

Provide the total qualified employee wage expenses, total qualified supply expenses, and total qualified contract research expenses for the claim year (this may be done using Form 6765, Credit for Increasing Research Activities).

These statements reconfirm the standard that a business components list (often referred to as a project list) is a fundamental necessity for filing research credit claims. For each business component taxpayers need to identify all the research activities they’ve performed, name the individuals who performed each research activity, and include the information each individual sought to discover. In other words, each business component must satisfy the elements set forth in I.R.C. § 41.

What’s new: the Specificity Requirement

The memorandum also includes a new requirement referred to as the specificity requirement. This is a jurisdictional prerequisite to filing a suit for refund, entailing taxpayers to provide the facts in a written statement to support any refund claims. For the claim or refund to be considered, the statement of the grounds and facts must be verified by a written declaration stating it is made under the penalties of perjury. The taxpayer’s signature on the amended return constitutes the declaration under the penalties of perjury for what is contained in the claim and what is attached to it.

The written statement must be submitted when a refund claim is filed. Otherwise, the refund claim should be rejected as deficient.

This new requirement is said to enable the Service to determine if a refund should be paid immediately based on the information provided or if an examination is needed to verify the taxpayer’s entitlement to the refund. This information helps the Service avoid paying refunds to taxpayers who have no factual support for their claim and allows the Service to effectively allocate its limited resources to determining which procedurally compliant claims to examine.

What’s the timing of this new requirement?

The additional information will now be required for all research credit claims made after a grace period ending January 10, 2022. A one-year transition period will be provided following this grace period to allow taxpayers 30 days to perfect a research credit claim before the IRS makes a final decision.

Generally, taxpayers are expected to file valid claims within three years of the date that the tax return was filed—or two years from the time the tax was paid, whichever is later. All additional requirements must be met.

How we can help

R&D credit claims often result in examinations, a process that is costly and burdensome to both the Service and taxpayers. MGO is here to help taxpayers determine their eligibility for R&D tax credits and develop and implement procedures to document R&D activities before claims are made, to ensure a smooth filing process.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology s

During the pandemic, telemedicine services provided important solutions to a system in crisis. They helped ease the burden on health care facilities and staff and offered individuals the care they needed. While in-person visits may have been a preference in the past, COVID-19 demonstrated the convenience and effectiveness of telemedicine for both patients and care providers. Though the health crisis has abated in many areas of the United States, caring for patients remotely through telemedicine will continue to provide important health resources, and valuable opportunities for software developers.

Tax incentives for telemedicine tools

Health care professionals are incorporating tablets, chat capabilities, and other mobile solutions to diagnose more patients in a shorter amount of time and across geographical boundaries. This demand for innovation presents opportunities for software companies, and the development of these technologies is being encouraged by Federal and state Research and Development (R&D) Tax Credits.

About the R&D tax credit

Enacted in 1981, the Federal R&D Tax Credit allows a credit of up to 14 percent of eligible spending for new and improved software products.

To qualify as an R&D activity, one must meet each of the following criteria:

• Technological in nature. Activities must be based on hard science. • Qualified purpose. Activities must be intended to develop a new or improved product or process. • Technological uncertainty. Activities must be aimed at eliminating uncertainty with respect to the development of a product or process. • Process of experimentation. Activities must involve a systemic or iterative approach of evaluating different alternatives to eliminate ambiguity.

Software companies developing platforms to enable and improve remote health care may be able to take advantage of the R&D Tax Credit as a dollar-for-dollar tax saving for the work that they are already doing.

Software activities that may qualify for a tax credit If your company is investing in developing telemedicine platforms, you may be able a claim an R&D Tax Credit. Though each situation is unique, development activities for the following products may qualify:

Tools that allow physicians to view medical images and other data on mobile devices such as smartphones, tablets, and other electronic devices

Application programming interfaces and capabilities to transfer information electronically and view electronic medical files

Cloud-based platforms to enable health care providers to directly engage patients in an easy-to-use virtual care environment that is HIPAA compliant

Platforms with the capabilities of linking physicians and pharmacies to allow physicians to submit a prescription electronically

Wearable devices with sensors to provide continuous monitoring of patients and automated treatment for health conditions

Virtual therapy platforms for online counseling

Medical data cloud storage solutions and data security

How we can help

The pandemic put our current telemedicine capabilities to the test, and patients gave these innovations a passing grade. But we have yet to experience the true power of telemedicine. As the innovation continues and popularity grows, we can be certain of even more widespread acceptance of telemedicine. And as the need continues to increase, it appears that the various tax credits for research and development will be available to help support the work of those who develop technology in the health care sector.

MGO professionals bring over 25 years of R&D Tax Credit experience to help you identify, analyze, file, and defend your claim. We provide a no-cost eligibility analysis to determine if these tax incentives are appropriate to your situation.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

When the IRS first came up with the Research and Development (R&D) Tax Credit, the industries it impacted were primarily scientific organizations and lab-based research companies. Today, eligibility has expanded to the point that most businesses in almost every industry can claim the credit, if they are performing research, and importantly, documenting it.

The R&D credit is a valuable tax tool, but it is complex and has attracted the attention of the IRS from the beginning. As recently as July 2021, the IRS made it clear that it was continuing to focus on those claiming the credit especially as it relates to the substantiation of qualified research. But attention from the IRS shouldn’t dissuade eligible businesses from claiming it.

Qualifying for the R&D credit

There are four requirements to qualify for the R&D credit. The business activities must:

Be intended to eliminate technical uncertainty about the development or improvement of a product or process

Constitute a process of experimentation

Be technical in nature and adhere to the standards of hard science

Relate to the development of a new or improved business component

Of all the qualifying requirements, the one that seems to create the most challenges for small businesses is documenting the process of experimentation (POE) in R&D projects.

Product development process

Having a well-documented product development process is just good business practice, but it also makes an IRS audit considerably smoother. If your business follows regulatory or industry standards on how products should be developed and tested, your documentation work is essentially done. However, even without formal industry standards, outlining how products are created, tested, and released will provide the information required by the IRS to demonstrate that you have a formal POE.

Documenting your POE

So, what does the IRS consider proper documentation of your POE? There are a few basic elements that will help make your case to the IRS. • Project accounting systems that track employee time and project costs provide the level of detail the IRS values. • Technical project documentation that highlights the process. • Technical documentation such as design drawings and revisions, patent applications, regulatory submissions, product tracking, and workflow logs.

The best practice for R&D credit documentation is to compile them systematically as you produce them, so you don’t need to search for them later or recreate them. If you clearly define, document, and allocate costs to the specific business components, claiming the tax credit can be a reasonably smooth process.

How we can help

MGO helps organizations across a wide range of industries develop and implement procedures to document their R&D activities. We help clients demonstrate their eligibility for the R&D credit and claim the credit available.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors. He can be reached at [email protected].

The Research and Development (R&D) tax credit is a commonly underutilized, yet powerful, tax incentive available for companies to substantially reduce their tax liability, improve their bottom-line, and reinvest back into their business. Daily activities performed by companies in a wide range of industries may qualify for federal and state R&D tax savings.

Unfortunately, R&D tax credits are also one of the most misunderstood methods of tax relief because there are many false assumptions about what is needed to qualify. In the following overview we’ll provide a brief description of the R&D tax rules, qualification criteria, and useful tips to maximize potential benefits. This article focuses specifically on federal R&D tax credits but there are also 40 states that provide R&D tax credits, each with its own set of rules and qualification criteria.

You don’t have to be scientists in white lab coats to qualify

For more than 40 years, companies have taken advantage of the R&D tax credit, claiming roughly $10 billion per year in tax savings. This powerful tax credit is not just available to large companies or companies employing hundreds of scientists. Companies of all sizes, in many different industries, may qualify for R&D tax credits including those working in software, manufacturing, aerospace and defense, agriculture, food and beverage, and life sciences. Even startups that have not yet generated taxable income may be able to monetize the R&D tax credit by claiming these R&D credits against their payroll tax liability.

There are many rules to claim an R&D tax credit but simply stated, if your company is involved in the technical development of new or improved products, or processes that require the undertaking of a systematic evaluation of multiple alternatives, to achieve the desired result, you may qualify. This applies to new product development, product enhancements, software development, manufacturing process improvements, and the list goes on…

Benefits of R&D tax credits for startups and small businesses

Unfortunately, many small businesses do not take advantage of this tax benefit because they self-censor, believing that their business will not qualify.

The Protecting Americans from Tax Hikes Act of 2015 opened the door for companies with little to no income tax liability to monetize the R&D tax credit. Eligible small businesses are now able to take the R&D credit against their alternative minimum tax liability. Eligible small businesses are defined as corporations that are not publicly traded, and are corporations, partnerships, or a sole proprietorship with average annual gross receipts not exceeding $50 million for the three taxable years preceding the current taxable year.

Startups with no more than five years of gross receipts and less than $5 million in gross receipts can also take advantage of the R&D tax credit incentive to offset up to $1,250,000 (over a five year period) of their Federal Insurance Contributions Act payroll taxes.

Benefits of timely capture of R&D tax credits

Even though a company may not be paying tax and may not be able to utilize the R&D tax credit currently, there are still good reasons to claim the credit. One of these reasons is that it is always easier to identify and document these credits while the supporting information is available and “fresh” in everyone’s minds. Waiting too long or until the company is profitable may be too late to capture the credits effectively, efficiently, and completely.

Another reason to choose to capture these credits in a timely fashion is because these credits can become extremely valuable in a sale transaction. Accumulated research and development credits can impact purchase price in an M&A or other deal, as a buyer may be inclined to pay more for the company if it has accumulated research credits (subject to IRC Sec. 383 limitations) and also if it has infrastructure in place to capture these credits on a “real time” basis.

Additionally, the accumulated credits may also be able to be used to offset the tax as result of a sale transaction. These credits may be able to offset the tax at the corporate level in the event of a C corporation sale or at the shareholder level in the event of pass-through entity sale.

The four-part R&D tax credit test

The criteria established by the following R&D four-part test will help to determine if your business qualifies for the R&D tax credit.

1. Technological in Nature – The activity performed must fundamentally rely on principles of engineering, computer science, physical or biological science.

2. Process of Experimentation – The company must demonstrate that they have undertaken an iterative development process, evaluating alternatives to eliminate uncertainty.

3. Elimination of Uncertainty – The activity must be aimed at eliminating uncertainty with respect to the development of a product or process.

4. Permitted Purpose – The activity must be intended to develop a new or improved business component.

Reviewing the tax code requirements and the company’s eligible activities should be the first step in the process of identifying potential R&D tax credits. Due diligence is required when adhering to the R&D tax credit rules and calculating and documenting the company’s qualified research activities. On the surface the rules may not seem complicated but there are many steps to claiming R&D credits – and many complicated tax court cases and a lot of misinformation that can make R&D claims confusing.

Importance of R&D tax credit documentation

To meet the requirements for the R&D tax credit, a history of the business’ qualifying activities must be documented. Documentation of R&D efforts can be challenging because employees may work on several projects at once and perform different types of duties. To address this, it is important to segment qualified R&D activities from all other work performed. Thankfully, today’s payroll systems can be programmed to track qualified research wages to qualified research projects.

The R&D tax credits may be claimed for both current and prior tax years, so it is recommended that companies document their R&D activities, so they’re well positioned to claim the credit for both situations.

The types of documentation that can be used to substantiate R&D labor expenses include: • Time tracking data • Employee W-2 forms • Project lists • Payroll registers • Time questionnaires • Job descriptions • Meeting minutes • Lab results • Interview notes provided for oral testimony

Common misconceptions about R&D tax credits

Today, more companies than ever are qualified to take advantage of the R&D tax credit. However, many businesses still have reservations and don’t believe they will qualify based on misconceptions about how the tax credit may apply to their business. Some of these misconceptions include:

• They don’t believe they do R&D work – The definition of R&D work is broad. If the business is attempting to develop or improve a new product or process it may qualify for the R&D tax credit.

• They don’t believe they are inventing anything – There is no requirement that product or processes be successful or new to the world.

• They believe the risk of an audit will increase – The R&D tax credit is a permanent incentive intended to promote innovation in the U.S. Claiming R&D credits on timely filed tax returns, whenever possible, is encouraged and in most cases does not trigger an audit. However it is imperative that the taxpayer collect and retain proper documentation to support any R&D tax credit claim.

Claiming the R&D credit

A taxpayer shouldn’t feel intimidated by preconceived notions of what R&D is or what companies can qualify. Across industries, the possibilities for qualifying activities exist, and vital tax savings may be uncovered to be used for future projects.

At MGO, our professionals bring more than 30 years of R&D tax experience to help you file and defend your R&D tax credit claim. We welcome the opportunity to provide your company with a complimentary R&D tax credit eligibility analysis to determine if this tax incentive can help fuel your company’s growth.