Rescheduling cannabis could unlock new merger and acquisition opportunities that companies need to strategically prepare for.

Sellers should focus on optimizing financials, tax implications, and valuation to maximize exit outcomes.

Buyers must conduct thorough diligence, structure tax-efficient deals, and plan for post-acquisition integration.

~

The potential rescheduling of cannabis from Schedule I to Schedule III could open up increased opportunities for mergers and acquisitions (M&A) in the industry. Navigating this new M&A landscape will require strategic preparation.

Whether you are looking to sell your company or acquire new assets and operations, you will need to position your business to properly capitalize on this wave of investment activity. Careful planning is critical to maximizing outcomes.

Preparing for M&A in a Post-Rescheduling World

As you anticipate this regulatory change, it is crucial to prepare for the complexities of the M&A process. Here is how you can position your company to take full advantage of upcoming opportunities.

Exit Strategies: Key Steps for Sellers

1. Books and Records Remediation

To attract investors, your financial records need to be in order. Focus on preparing your financial statements and building a comprehensive data room that investors can easily review. Solid financial reporting will not only boost investor confidence but also help you stand out in the marketplace.

2. Tax Optimization

Understanding the tax implications of a transaction is essential. Structure your deals to minimize tax liabilities and maximize financial outcomes. Engage with tax professionals early in the process to help you achieve the best possible financial results.

3. Audits and Reviews

Depending on the size and nature of the transaction, having audited or reviewed financial statements may be necessary. Even if not required, these statements can increase the likelihood of closing a deal, improve pricing, and reduce the time needed to finalize the transaction.

Acquisition Strategies: Essential Considerations for Buyers

1. Diligence

Conducting thorough diligence is crucial for identifying potential risks associated with an acquisition. This includes financial and tax diligence to uncover any issues that could impact deal terms, pricing, or strategy. Understanding these risks upfront will enable you to make more informed decisions.

2. Structuring

Designing a tax-efficient acquisition structure is key to the transaction’s success and the long-term health of the combined entity. Work with advisors to develop structures that optimize tax outcomes and operational efficiency.

3. Post-Deal Integration

Post-acquisition integration is critical for realizing the anticipated benefits of the deal. Strategic guidance and practical support during this phase will help you optimize both operational and financial performance, leading to a smooth transition and better overall outcomes.

Smart M&A Moves for Buyers and Sellers Alike

1. Quality of Earnings (Q of E) Assessments

A Q of E assessment provides a comprehensive evaluation of a company’s financial performance. For buyers, a Q of E offers valuable insights into the target company’s financial health, facilitating informed decision-making and risk mitigation. For sellers, this detailed analysis helps you identify key negotiation points, leading to better pricing and more favorable deal terms.

2. Strategic Guidance

Both buyers and sellers can benefit from strategic M&A advice tailored to your specific business goals. Engaging with experienced advisors can provide you valuable insights and help you navigate the complex M&A landscape, positioning your company to take full advantage of any opportunities that arise from rescheduling.

How MGO Can Help

With a dedicated Cannabis team and a comprehensive suite of services, MGO is here to help you navigate the complexities of M&A — both now and in a post-rescheduling world. Reach out to our team today for support at every stage of the M&A process.

The potential rescheduling of cannabis presents an opportunity to reevaluate your company’s tax structure and increase deductions, reduce income, and simplify accounting.

Rescheduling may open up access to previously unavailable tax credits, incentives, and deductions at various government levels.

With anticipated increased investment and cash flow after rescheduling, companies should prepare for potential mergers and acquisitions by seeking support in areas like financial due diligence and post-acquisition planning.

~

The rescheduling of cannabis from Schedule I to Schedule III will unlock new opportunities for cannabis businesses. Is your company positioned to capitalize?

Tax Restructuring

If your existing operating structure was optimized for Section 280E mitigation, now is the time to evaluate whether it will still be tax-efficient after rescheduling.

MGO’s dedicated cannabis tax team can analyze your current structure and identify opportunities to increase deductions, reduce income, simplify accounting, and eliminate unnecessary tax exposures. We will help you develop a strategy specific to your business needs that aligns with your operational goals and any regulatory considerations.

Tax Credits, Incentives, and Deductions

Rescheduling should open cannabis operators to a world of previously unavailable tax benefits.

Our tax professionals can comprehensively review your business operations to uncover tax credits, incentives, and deductions that you may qualify for at the federal, state, and local levels.

Financial and Internal Control Audits

While rescheduling will eliminate the Section 280E tax burden and attract new investors to the cannabis industry, it could also lead to a new regulatory framework.

Our audit services can provide assurance to investors that your company is effectively managing risks, complying with any regulatory changes, and maintaining transparency.

Mergers and Acquisitions (M&A)

The projected wave of investment and increased cash flow resulting from rescheduling means more M&A should be on the horizon.

If your company is considering an M&A deal (either as a buyer or seller), MGO can support your efforts with structuring, financial & tax due diligence, Quality of Earnings (QoE) assessments, accounting integration, strategic guidance, and post-acquisition planning.

Internal controls, especially around fraud prevention, are essential for limiting losses, driving efficiency, improving accountability, and boosting company value during investments or M&A deals.

The “tone at the top” from leadership in fostering an ethical environment, along with proper segregation of duties, are key elements for fraud prevention and strong internal controls.

Well-established policies and procedures, like Delegation of Authority rules and restricted system access protocols, are also vital for maintaining adequate controls to enable company growth.

~

As the economy stands on shaky legs, private equity and venture capital firms are necessarily careful and strategic when assessing potential investment opportunities. Whether your long-term plan includes acquiring another company, selling your business, or seeking new capital, strengthening your internal control environment — with a focus on preventing fraud — is a powerful way to increase actual and perceived value.

In the following, we will lay out the reasons why fraud prevention is an essential element to proper corporate governance and illustrate key areas to examine whether your internal control environment is built to help your operation succeed.

The Importance of Internal Controls in Fraud Prevention

A robust internal control system is the first step toward managing, mitigating, and uncovering fraud. A strong internal control environment will:

Protect your company’s assets by reducing the risk of theft or misappropriation of cash, inventory, equipment, and intellectual property.

Detect fraudulent activities or irregularities early on and deter employees from attempting fraud in the first place.

Provide cost savings by limiting opportunities for financial losses, costly investigations, and legal expenses associated with fraud.

Drive operational efficiency by providing clear processes and guidelines that reduce the risk of errors or inefficiencies in day-to-day operations.

Improve employee accountability by implementing checks and balances that discourage unethical behavior.

When seeking an investment or undertaking a significant M&A deal, you should have a firm grasp of the strength and quality of your internal control environment. Not only will you reduce the risk of fraud in the near term, but you will also cultivate confidence with potential investors and M&A partners.

Fraud Prevention Starts with the “Tone at the Top”

The first key element to look for in measuring the strength of your internal controls is ensuring a clear and proactive “tone at the top”, meaning an ethical environment fostered by the board of directors, audit committee, and senior management. A good tone at the top encourages positive behavior and helps prevent fraud and other unethical practices.

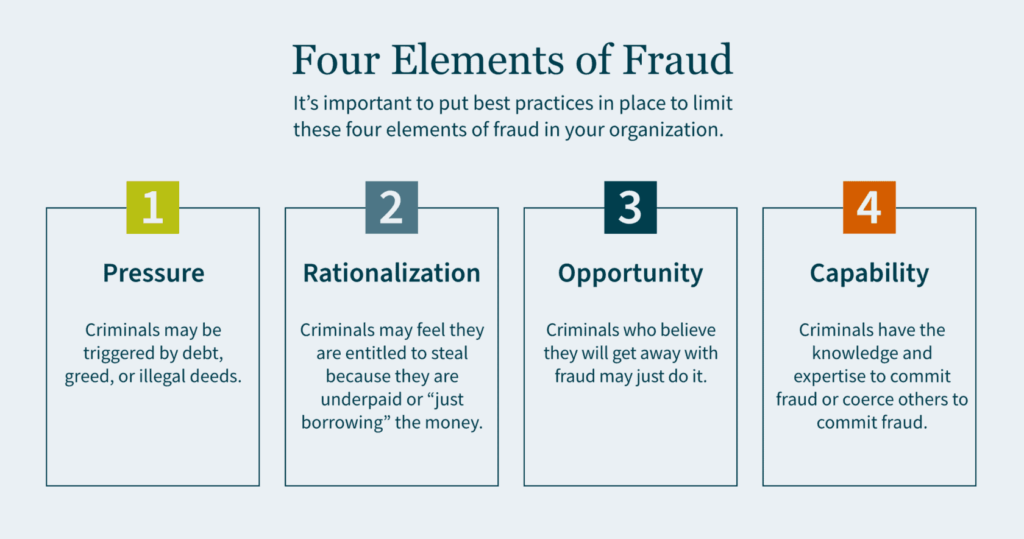

There are four elements to fraud: pressure, rationalization, opportunity and capability.

Pressure motivates crime. This could be triggered by debt, greed, or illegal deeds. Individuals who have financial problems and commit financial crimes tend to rationalize their actions. Criminals may feel that they are entitled to the money they are stealing, because they believe they are underpaid. In some cases, they simply rationalize to themselves that they are only “borrowing” the money and have every intention of paying it back.

Criminals who can commit fraud and believe they will get away with it may just do it. Capability means the criminal has the expertise as well as the intelligence to coerce others into committing fraud. The board of directors is responsible for selecting and monitoring executive management to ensure best practices are in place to limit the motivations of all four elements of fraud.

Proper Segregation of Duties for Internal Controls

The second key element to look for in your internal controls is a well-established segregation of duties. The idea is to establish controls so that no single person has the ability that would allow them the opportunity to commit fraud. Companies must make it extremely difficult for any single employee to have the opportunity to perpetrate a crime and subsequently cover it up.

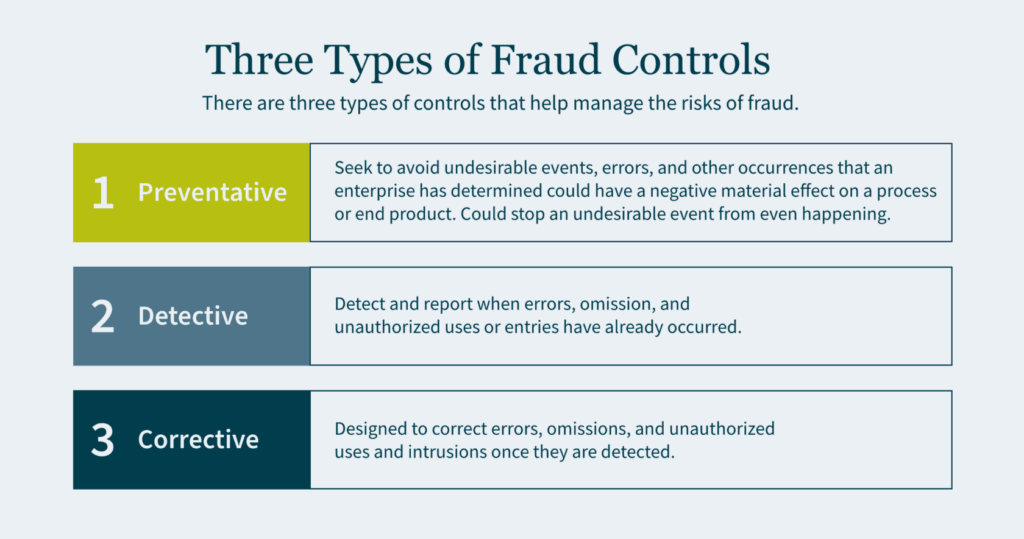

Fraud Controls

There are three types of controls that help manage the risks of fraud: preventative, detective, and corrective.

Preventative controls seek to avoid undesirable events, errors, and other occurrences that an enterprise has determined could have a negative material effect on a process or end product. Preventative controls are the best of the three as they are the first line of defense and a backstop to fraud. If designed correctly, preventative controls stop an undesirable event from even happening.

Detective controls exist to detect and report when errors, omission, and unauthorized uses or entries have already occurred. Although it is important to identify these adverse events, you are doing so after the fraud has already been committed.

Corrective (also referred to as compensating) controls are designed to correct errors, omissions, and unauthorized uses and intrusions once they are detected.

Preventing Misappropriation of Assets

An important component of segregation of duties is to prevent the misappropriation of assets and reduce fraud risk. Below are some examples of best practices for various types of assets:

Cash Receipt: segregate the receipt of cash/checks and the recording of the journal entry in the accounting system into two roles.

Accounts Receivable: segregate the responsibilities of recording cash received from customers and providing credit memos to customers. (If one person performs both functions, it creates the opportunity to divert payments from the customer to the employee and then cover the theft with a matching credit to the customer’s account).

Cash Reconciliation: the individuals who authorize, process, or record cash should not perform the bank reconciliation to the general ledger.

Inventory: individuals who order goods from the suppliers should not have the ability to log the goods received in the accounting system.

Payroll: segregate the responsibilities of compiling gross and net pay for payroll, with the responsibilities of verifying the calculation. (If a single individual performs both functions, it allows for the opportunity to increase personal compensation and the compensation of others without authorization. It also provides an opportunity to create a fictitious payee and make corresponding payroll checks).

The Importance of Policies and Procedures

The third key element to look for in your investees is well-established policies and procedures. Make sure that any company you consider acquiring has basic policies and procedures in place, such as Delegation of Authority (DOA).

The DOA is a policy where the executive team delegates authority to the management of the company. Individuals should be considered appropriate to fulfill delegated roles and responsibilities. The DOA should be reviewed at least annually. Subsequently, it is important to ensure that the DOA is being followed, and that approvals do not deviate from it. Any such anomalies should be rare and, when they do occur, they need to be reviewed and approved. Constant deviations from the DOA may be a sign that the DOA needs to be restructured.

A second essential policy and procedure is restricted computer and application access. This is to protect sensitive company financials and proprietary data. The company should have a robust control environment and maintain computer logins and password access on a need-to-know basis. Access should only be granted by the owner of the application or system and subsequently logged by the administrator. Now more than ever companies are hiring remote employees. This shift in the dynamic workspace further emphasizes the need for a quality IT controls environment.

How We Can Help

As you prepare your company for future growth, getting an impartial third-party opinion on your internal control environment can be a powerful tool for finding gaps and inefficiencies, and implementing value-added changes.

Our dedicated Public Company teams offer a deep level of industry experience and technical skills. We can help prepare your company for a major capital raise, including going public via an IPO or RTO. Or we can help optimize value for an M&A deal, whether you are buying or selling. Contact us today to access an external, holistic vision focused on helping you grow and succeed

Welcome to the Cannabis M&A Field Guide from MGO. In this series, our practice leaders and service providers provide guidance for navigating M&A deals in this new phase of the quickly expanding industries of cannabis, hemp, and related products and services. Reporting from the front-lines, our team members are structuring deals, implementing best practices, and magnifying synergies to protect investments and accrete value during post-deal integration. Our guidance on market realities takes into consideration sound accounting principles and financial responsibility to help operators and investors navigate the M&A process, facilitate successful transactions, and maximize value.

In the cannabis and hemp industries, capturing the true value of real estate holdings in an M&A deal can be both elusive and central to the overall success of the transaction. Difficult-to-acquire licenses and permits are essential for operating, which often drives up the “ticket price” of property, ignoring operational and market realities that suppress value in the long run. On the flip side, real estate holdings are sometimes considered “throw-ins” during a large M&A deal. These properties can hold risks and exposures, or, in many cases, are under-utilized and present an opportunity to uncover hidden value.

Both Acquirers and Target companies must take specific steps toward understanding the varied layers of risk and opportunity presented by real estate holdings. In the following, we will address some common scenarios and provide guidance on the best way to ensure fair value throughout an M&A deal.

Real estate as a starting point for enterprise value

Leaders of cannabis and hemp enterprises must understand that real estate should be a focus of the M&A process from the very beginning. All too often, c-suite executives are well-acquainted with detailed financial analyses for other parts of the business, but have a limited or out-of-date idea of their enterprise’s square footage, details of lease agreements, or comparable values in shifting real estate markets. Oftentimes it takes a major business event, like an M&A deal, to spur leadership to reexamine and understand real estate holdings and strategy. Regrettably, and all too often, principals come to that realization post-closing and realize they may have left money on the table.

In an M&A deal, the party that takes a proactive approach to real estate considerations gains an upper-hand in negotiations and calculating value. Real estate holdings can provide immediate opportunities for liquidity, cost-reduction, or revenue generation. At the same time, detailed due diligence can reveal redundant properties, costly debt obligations, unbreakable leases, and other red flags that would undermine value post-closing.

For both sides of the M&A transaction, real estate strategy and valuation should be a core consideration of the overall goals and value drivers of the deal. A direct path to this mindset is to place real estate holdings on the same level of importance as other assets that drive value – human capital, technology, intellectual property, etc. Ensuring that real estate strategy aligns with business goals and objectives will save considerable headaches and potential liabilities in the later stages of negotiating and closing the deal. Qualify and confirm all real estate data

One of the harmful side-effects of a laissez-faire attitude toward real estate in M&A is that the entire deal can be structured around data that is simply inaccurate or incomplete. This inconsistency is not necessarily the result of an overt deception, but too often it is simply an oversight. Valuations can also be based upon pride and ego, without supporting market data.

Let’s visit a very common M&A scenario: The Target company has real estate data on file from when they purchased or leased the property (which may have been years ago), and that data says headquarters is 20,000 sq. ft. of office space. Perhaps they invested heavily into improvements like custom interiors that did nothing to add value to the real estate. The Target includes that number in the valuation process and the Acquirer assumes it is accurate. Following the deal, the Acquirer moves in and, in the worst case, realizes there is actually only 15,000 sq. ft. of useable space. Or it is equally common that the Acquirer learns the space is actually 25,000 sq. ft. Either way, value has been misrepresented or underreported. M&A deals involve a multitude of figures and calculations, and sometimes things are simply missed. But those small things can have a major impact on value and performance in the long run.

The only solution to this problem is to dedicate resources to qualifying and quantifying data related to real estate holdings. When preparing to sell, Target companies should review all assumptions – square footage, usage percentage, useful life, etc. – and conduct field measurements and physical condition assessments (“PCA’s”). This will help your team understand the value of your holdings and set realistic expectations, and perhaps just as importantly, it saves you from the embarrassment of providing inaccurate numbers exposed during Acquirer’s due diligence—and getting re-traded on price and terms. That reputation will ripple through the marketplace.

From the Acquirer’s side, the details of real estate holdings should come under the same level of scrutiny as financials, control environment, etc. Your due diligence team should commission its own field measurements and PCA, and also seek out market comparables to confirm appraisals. It is simply unsafe and unwise to assume the accuracy of any of these details. Performing your own assessments could reveal a solid basis to re-negotiate the M&A, and will help shape post-merger integration planning.

Tax analysis will reveal risks and opportunities

The maze of tax regimes and regulatory requirements cannabis and hemp operators navigate naturally creates opportunities to maximize efficiencies. This is particularly the case when it comes to enterprise restructuring to navigate the tax burden of 280E.

For example, it may be possible to establish a real estate holding company that is a distinct entity from any “plant-touching” operations. By restructuring the real estate holdings and contributing those assets to this new entity it may be possible to take advantage of additional tax benefits not afforded to the group if owned directly by the “plant-touching” entity. This all assumes a fair market rent is charged between the entities.

Recently, operators have looked to sale/leaseback transactions to help with cash flow needs and thus these types of transactions have gained prominence for cannabis and hemp operators. It is important that these transactions be carefully reviewed prior to execution to ensure they can maintain their tax status as a true sale and subsequent lease, instead of being considered a deferred financing transaction. If a Target company has a sale/leaseback deal established but under audit the facts and circumstances do not hold up, this could open up major tax liabilities for the Acquirer.

When entering into an M&A transaction, it is important that the Acquirer look at the historical and future aspects of the Target’s assets, including the real estate, to maximize efficiencies of these potentially separate operations. It is also equally important to review pre-established agreements/transactions to ensure the appropriate tax classification has been made and that the appropriate facts and circumstances that gave rise to the agreements/transactions have been documented and followed to limit any potential negative exposure in the future.

Contract small print could make or break a deal

An area of particular focus during due diligence should be a review, and close read, of the Target company’s existing property leases and other contracts. There are any number of clauses and agreements that seem harmless and inconsequential on the surface, but can have disastrous effects in difficult situations. In many cases the lease/contract of a property is more important than the details of the property itself. For example, if the non-negotiable rent on a retail location is too high (and scheduled to go higher), there may be no way to ever turn a profit.

The financial distress resulting from the COVID-19 pandemic has brought these issues to the forefront in the real estate industry. Rent payment and occupancy issues are shifting the fundamental economics of many property deals and contracts. If, for example, you are acquiring a commercial location that is under-utilized because of market demand or governmental mandate, you must confirm whether sub-leases or assignments are allowed at below the contract price. If not, you could be stuck with a costly, underperforming asset amid quickly shifting commercial real estate demand.

In many leases and contracts there are Tenant Improvement Allowance conditions that require the landlord to fund certain property improvement projects. If utilizing these terms is part of the Acquirer’s plans, you may need to have frank and open conversations with landlords about whether the funds for these projects are still available, and if those contract obligations will be met. Details like these are often penned during times of financial comfort without consequences to the non-performing party, but a landlord struggling with cash flow may not have the capability to meet contract standards.

These are just a few examples from a multitude of potential real estate contract issues that can emerge. It is recommended to not only examine these contracts very closely, but have dedicated real estate industry experts perform independent assessments that account for broader social, economic, and market realities. That independent analysis will help your executive team formulate a real estate strategy that better aligns with core business objectives.

Dig deep to uncover real value

There are countless scenarios where issues related to real estate make or break an otherwise solid M&A transaction, whether before or after closing the deal. The only path forward is to treat real estate holdings with the same care and attention paid to the other asset classes driving the deal. The cannabis and hemp industries have recently endured micro-boom-and-bust cycles that have left many assets under-performing. As Target companies offload these assets, and Acquirers seek out good deals, both parties must undertake focused efforts to establish the fair value of complex real estate assets and obligations.

Welcome to the Cannabis M&A Field Guide from MGO. In this series, our practice leaders and service providers provide guidance for navigating M&A deals in this new phase of the quickly expanding industries of cannabis, hemp, and related products and services. Reporting from the front-lines, our team members are structuring deals, implementing best practices, and magnifying synergies to protect investments and accrete value during post-deal integration. Our guidance on market realities takes into consideration sound accounting principles and financial responsibility to help operators and investors navigate the M&A process, facilitate successful transactions, and maximize value.

Imagine a row of dominoes: every block between the first and last must be positioned perfectly, or else the last domino never falls.

Think of M&A transactions in a similar way. The integration of the two entities is both the ultimate goal, and the final phase. But every step between beginning and end must be aligned to facilitate that final result. If there is a failure or distraction at any stage, the whole venture can fail.

This analogy is important because, all too often, we see the integration phase of an M&A deal treated as an afterthought. When, in fact, it is as important as any other stage, and the considerations of integration should play a role throughout the M&A process.

Many cannabis and hemp industry M&A deals are driven by the desire to become vertically integrated, which in some cases, means an entirely distinct business unit will be brought into the fold (e.g., a retailer acquires cultivation/manufacturing facilities). The greater the fundamental differences between Acquirer and Target company, the greater the task of integration. As always, early planning and focused communication represent the only proven and viable path forward.

Integration planning is unique to every organization, and every M&A deal. In the following we will provide the broad strokes of considerations that both sides of the transaction should have in mind throughout the M&A process.

Integration basics: big picture goals

On its face, integration is simple: two companies are coming together to form a combined entity. When structured and executed properly, the ultimate goal can, and should be, making the final entity greater than the sum of its parts. To achieve this, both parties should focus on four key goals:

1. Maintain Momentum – Acquirer and Target company must not allow the M&A deal to significantly disrupt existing operations. Focus should be on a smooth transition that does not interrupt either party so the whole enterprise gains momentum. 2. Build On Each Other – Synergies and opportunities for value creation are typically the drivers of an M&A deal. Never lose focus on these dynamics and lean into them throughout the integration process. 3. Align Cultures and Optimize Organizational Structure – Often culture integration is an afterthought. However, the deal is just the beginning step, what comes after is integration of two different company styles. Establishing shared values and vision will translate into common organizational goals and ultimately faster success. 4. Leverage Efficiencies to Move Forward – The Acquirer is making the deal for a reason, focus on these strategic and tactical advantages to start maximizing value at the onset.

Dedicated and early integration process planning

The first step for ensuring a successful integration is to create a dedicated integration team that will devise a road map for delivering the synergies and efficiencies that were identified, and drove, the M&A deal. The team, as well as the road map, should be focused on delivering the expected value and transformational opportunities.

The road map should describe key activities and decisions throughout essential stages: pre-acquisition; first day following acquisition; weekly goals and metrics; 100 day goals, etc. This road map should address the following:

Sustaining ongoing operations for both the acquiring and acquired entities;

Satisfying existing customers and business relationships;

Identifying the critical decisions that must be made and including when they must be made;

Steps toward retaining essential employees;

Maintaining labor relations and productivity;

Integrating distinct corporate cultures

Organizing the processes for delivering the expected value to shareholders.

While an integration road map must be followed, it cannot be rigid. There are certain conditions that will only emerge once the deal is closed and the integration process begins in earnest. The integration team must communicate regularly and prepare contingencies and alternate plans to address unexpected issues.

Managing and avoiding personnel issues

A certain amount of personnel turn-over can be expected following any M&A deal. A lack of communication can cause distrust and dismay among Target company staff, and even among the Acquirer’s ranks. That is why a proactive approach to integrating the Human Resources (HR) function, and managing personnel, must be a high priority during the integration process.

The adjustments that occur in an acquisition can be significant, including changes in leadership styles, decision-making practices, organizational structure, and reporting relationships. All of these modifications can disrupt productivity, negatively impact morale, and decrease employee engagement.

To help prevent these negative consequences, an HR integration plan must be established in advance and should include the following steps:

Form a dedicated HR integration team — A component of the integration team should be solely responsible for managing personnel issues. They should be focused on mitigating cultural differences, directly and regularly communicating the change process, and retaining and motivating key employees.

Communicate upcoming events to all affected employees — Rumors spread rapidly and employees are often anxious due to the perceived job insecurity and uncertainty of their position in the acquiring company. Head off any cancerous rumors by communicating upfront with employees about the upcoming changes due to the acquisition.

Address employee concerns regarding retention — The HR integration team must examine the employment contracts of all staff for “change of control” clauses as well as employee stock options. They should then develop and communicate a plan to address these concerns.

Assessing corporate culture — The HR integration team must anticipate cultural challenges and take steps to integrate the two cultures. For example, one company may be driven by a sales mentality while another may be focused on innovation. Also, decisions in one company may be top-down while the other may be used to more participative decision-making. An integrated culture approach should be considered to mitigate the shock effect of the merger on the Target company’s staff.

Blend HR policies and procedures — This task can be resource and time-intensive, and include stages of legal review. But it is important to make sure all staff of the new entity understand the employee handbook, their benefits, and all other HR functions. Areas of focus include updating and communicating performance management procedures, training and development opportunities, and developing a shared intranet site.

Generate a strategy for continuance of benefits — A major point of concern for staff of the Target company will be changes to benefits. In the due diligence stage, the Target company’s benefit packages should be assessed and a pre-integration plan must be put into place that limits disruption of employee health and retirement benefits.

Making systems and processes one

One of the most essential and challenging segments of the integration process will be coordinating and implementing system changes. Particularly, in regard to Information Technology. Technology is pervasive, touching virtually all aspects of a company’s operations, and many of these functions are mission-critical. Because IT is the common denominator among all corporate departments, successful integration is critical to the success of the entire operation.

The following are the key steps to take when integrating IT functions:

Form an IT Steering Committee – Like the HR integration team, you should also designate a sub-group of professionals focused solely ensuring the integration of all IT operations.

Align corporate governance – Internal controls are essential in any industry, and cannabis and hemp are no exception. The Acquirer will have their own systems in place and the relative strength and compatibility of the Target company’s own system should be a focus of the due diligence process. The next step will be to combine or update the new entity’s policies, practices, and functions.

Implement applications and data system – In an ideal environment, the Acquirer and the resulting entity from the M&A deal will share a core information system. Achieving this will require a period of aligning processes and controls and consolidating and eliminating redundant functionality and platforms.

IT organization and structure – Key IT functions and responsibilities will need to be combined, assigned, and reorganized to support the mission, vision, and strategy of the combined organization.

Establish security and privacy rules – The new, combined IT environment will need clearly defined policies, standards, and responsibilities for ensuring appropriate handling and protection of company data across the organization.

Integration must be a priority – and not an afterthought

It won’t matter how much time and effort is put into the early stages of the M&A process if the post-merger integration is mishandled. You must keep this ultimate goal in mind throughout all stages and proactively plan for the smoothest integration possible. As with all things, every bit of pre-planning will pay dividends in the end. You want to be launching new products, entering new markets, or engaging in the other value drivers that spurred the deal in the first place. The alterna

Welcome to the Cannabis M&A Field Guide from MGO. In this series, our practice leaders and service providers provide guidance for navigating M&A deals in this new phase of the quickly expanding industries of cannabis, hemp, and related products and services. Reporting from the front-lines, our team members are structuring deals, implementing best practices, and magnifying synergies to protect investments and accrete value during post-deal integration. Our guidance on market realities takes into consideration sound accounting principles and financial responsibility to help operators and investors navigate the M&A process, facilitate successful transactions, and maximize value.

Deal structure can be viewed as the “Terms and Conditions” of an M&A deal. It lays out the rights and obligations of both parties, and provides a roadmap for completing the deal successfully. While deal structures are necessarily complex, they typically fall within three overall strategies, each with distinct advantages and disadvantages: Merger, Asset Acquisition and Stock Purchase. In the following we will address these options, and common alternatives within each category, and provide guidance on their effectiveness in the cannabis and hemp markets.

Key considerations of an M&A structure

Before we get to the actual M&A structure options, it is worth addressing a couple essential factors that play a role in the value of an M&A deal for both sides. Each transaction structure has a unique relationship to these factors and may be advantageous or disadvantageous to both parties.

Transfer of Liabilities: Any company in the legally complex and highly-regulated cannabis and hemp industries bears a certain number of liabilities. When a company is acquired in a stock deal or is merged with, in most cases, the resulting entity takes on those liabilities. The one exception being asset deals, where a buyer purchases all or select assets instead of the equity of the target. In asset deals, liabilities are not required to be transferred.

Shareholder/Third-Party Consent: A layer of complexity for all transaction structures is presented by the need to get consent from related parties. Some degree of shareholder consent is a requirement for mergers and stock/share purchase agreements, and depending on the Target company, getting consent may be smooth, or so difficult it derails negotiations.

Beyond that initial line of consent, deals are likely to require “third party” consent from the Target company’s existing contract holders – which can include suppliers, landlords, employee unions, etc. This is a particularly important consideration in deals where a “change of control” occurs. When the Target company is dissolved as part of the transaction process, the Acquirer is typically required to re-negotiate or enter into new contracts with third parties. Non-tangible assets, including intellectual property, trademarks and patents, and operating licenses, present a further layer of complexity where the Acquirer is often required to have the ownership of those assets formally transferred to the new entity.

Tax Impact: The structure of a deal will ultimately determine which aspects are taxed and which are tax-free. For example, asset acquisitions and stock/share purchases have tax consequences for both the Acquirer and Target companies. However, some merger types can be structured so that at least a part of the sale proceeds can be tax-deferred.

As this can have a significant impact on the ROI of any deal, a deep dive into tax implications (and liabilities) is a must. In the following, we will address the tax implications of each structure in broad strokes, but for more detail please see our article on M&A Tax Implications (COMING SOON).

Asset acquisitions

In this structure, the Acquirer identifies specific or all assets held by the Target company, which can include equipment, real estate, leases, inventory, equipment and patents, and pays an agreed-upon value, in cash and/or stock, for those assets. The Target company may continue operation after the deal. This is one of the most common transaction structures, as the Acquirer can identify the specific assets that match their business plan and avoid burdensome or undesirable aspects of the Target company. From the Target company’s perspective, they can offload under-performing/non-core assets or streamline operations, and either continue operating, pivot, or unwind their company. For the cannabis industry, asset sales are often preferred as many companies are still working out their operational specifics and the exchange of assets can be mutually beneficial.

Advantages/Disadvantages

Transfer of Liabilities: One of the strongest advantages of an asset deal structure is that the process of negotiating the assets for sale will include discussion of related liabilities. In many cases, the Acquirer can avoid taking on certain liabilities, depending on the types of assets discussed. This gives the Acquirer an added line of defense for protecting itself against inherited liabilities.

Shareholder/Third-Party Consent: Asset acquisitions are unique among the M&A transaction structures in that they do not necessarily require a stockholder majority agreement to conduct the deal.

However, because the entire Target company entity is not transferred in the deal, consent of third-parties can be a major roadblock. Unfortunately, as stated in our M&A Strategy article, many cannabis markets licenses are inextricably linked to the organization/ownership group that applied for and received the license. This means that acquiring an asset, for example a cultivation facility, does not necessarily mean the license to operate the facility can be included in the deal, and would likely require re-application or negotiation with regulatory authorities.

Tax Impact: A major consideration is the potential tax implications of an asset deal. Both the Acquirer and Target company will face immediate tax consequences following the deal. The Acquirer has a slight advantage in that a “step-up” in basis typically occurs, allowing the acquirer to depreciate the assets following the deal. Whereas the Target company is liable for the corporate tax of the sale and will also pay taxes on dividends from the sale.

Stock/share purchase

In some ways, a stock/share purchase is a more efficient version of a merger. In this structure, the acquiring company simply purchases the ownership shares of the Target business. The companies do not necessarily merge and the Target company retains its name, structure, operations and business contracts. The Target business simply has a new ownership group.

Advantages/Disadvantages

Transfer of Liabilities: Since the entirety of the company comes under new ownership, all related liabilities are also transferred.

Shareholder/Third Party Consent: To complete a stock deal, the Acquirer needs shareholder approval, which is not problematic in many circumstances. But if the deal is for 100% of a company and/or the Target company has a plenitude of minority shareholders, getting shareholder approval can be difficult, and in some cases, make a deal impossible.

Because assets and contracts remain in the name of the Target company, third party consent is typically not required unless the relevant contracts contain specific prohibitions against assignment when there is a change of control.

Tax Impact: The primary concern for this deal is the unequal tax burdens for the Acquirer vs the Shareholders of the Target company. This structure is ideal for Target company shareholders because it avoids the double taxation that typically occurs with asset sales. Whereas Acquirers face several potentially unfavorable tax outcomes. Firstly, the Target company’s assets do not get adjusted to fair market value, and instead, continue with their historical tax basis. This denies the Acquirer any benefits from depreciation or amortization of the assets (although admittedly not as important in the cannabis industry due to 280E). Additionally, the Acquirer inherits any tax liabilities and uncertain tax positions from the Target company, raising the risk profile of the transaction.

Three types of mergers

1: Direct merger

In the most straight-forward option, the Acquiring company simply acquires the entirety of the target company, including all assets and liabilities. Target company shareholders are either bought out of their shares with cash, promissory notes, or given compensatory shares of the Acquiring company. The Target company is then considered dissolved upon completion of the deal.

2: Forward indirect merger

Also known as a forward triangular merger, the Acquiring company merges the Target company into a subsidiary of the Acquirer. The Target company is dissolved upon completion of the deal.

3: Reverse indirect merger

The third merger option is called the reverse triangular merger. In this deal the Acquirer uses a wholly-owned subsidiary to merge with the Target company. In this instance, the Target company is the surviving entity.

This is one of the most common merger types because not only is the Acquirer protected from certain liabilities due to the use of the subsidiary, but the Target company’s assets and contracts are preserved. In the cannabis industry, this is particularly advantageous because Acquirers can avoid a lot of red tape when entering a new market by simply taking up the licenses and business deals of the Target company.

Advantages/Disadvantages

Transfer of Liabilities: In option #1, the acquirer assumes all liabilities from the Target company. Options #2 and #3, provide some protection as the use of the subsidiary helps shield the Acquirer from certain liabilities.

Shareholder/Third Party Consent: Mergers can be performed without 100% shareholder approval. Typically, the Acquirer and Target company leadership will determine a mutually acceptable stockholder approval threshold.

Options #1 and #2, where the Target company is ultimately dissolved, will require re-negotiation of certain contracts and licenses. Whereas in option #3, as long as the Target company remains in operation, the contracts and licenses will likely remain intact, barring any “change of control” conditions.

Tax Impact: Ultimately, the tax implications of the merger options are complex and depend on whether cash or shares are used. Some mergers and reorganizations can be structured so that at least a part of the sale proceeds, in the form of acquirer’s stock, can receive tax-deferred treatment.

In conclusion

Each deal structure comes with its own tax advantages (or disadvantages), business continuity implications, and legal requirements. All of these factors must be considered and balanced during the negotiating process.