Companies face tax burden challenges related the classification of cannabis as a Schedule I controlled substance and IRC 280E.

To navigate this, companies may be able to utilize vertical integration strategies and incorporate transfer pricing best practices to minimize tax exposure.

A transfer pricing study will help identify and risks or opportunities for improvement.

As the cannabis market continues to grow, in the United States cannabis operators continue to face difficulties related to an excessive tax burden due to IRC 280E. One of the most effective strategies for mitigating tax exposure under 280E has been to leverage the benefits of vertical integration.

Since IRC 280E affects the various verticals differently, some cannabis companies are able to isolate activities within distinct business units and maximize Cost of Goods Sold (COGS) calculation to mitigate the impact of IRC 280E.

The potential downside is two-fold. First, IRS tax court cases have made it clear that isolating business units is not a universal solution. And secondly, if not optimally established and documented, transactions between the business units can be problematic and create issues with the IRS.

This article breaks down the impact of IRC 280E, demonstrates the potential benefits of vertical integration, and describes how a proactive transfer pricing strategy can help you maneuver the specific tax and regulatory considerations that affect the industry.

What IRC 280E means for your tax liability

Section 280E penalizes traffickers of Schedule I or II drugs by prohibiting the deduction of “ordinary and necessary” business expenses after reducing gross receipts by COGS, essentially resulting in your federal income tax liability being calculated based on gross income, not net income. For a cannabis operator, COGS typically consist of the cost of acquiring inventory by purchase or production.

Not only are these cannabis companies facing high federal taxes, but there is now an intense level of scrutiny in both federal and state tax audits on intercompany arrangements.

Impact of vertical integration on IRC 280E calculations

Many cannabis companies have become vertically integrated, i.e., combining production function (i.e., cultivation and manufacturing) of cannabis with retail or resale (i.e., distribution) or sometimes all three. Since Section 280E is directly related to selling or the “trafficking” of cannabis-related products, it has the biggest potential impact on retail operations. This means that if a producer can support a higher selling price to its retailer, the retailer will have more COGS from the producer, and the producer will have more costs to deduct because of the allowance of indirect costs.

The business motivation for vertical integration is to better control the supply chain and the end user’s experience. From a tax perspective, cannabis taxpayers want to dis-integrate activities subject to 280E from those for which a position can be argued that they are non-280E activities, such as management services. The Internal Revenue Service (IRS) uses transfer pricing to challenge such segregation and to make allocations between or among the members of a controlled group.

How a transfer pricing study can help your cannabis business

Whether its receives the recent budget infusion or not, the IRS is likely to conduct more transfer pricing audits of the cannabis industry, compared to other industries. These audits frequently result in much higher tax adjustments and significant penalties. In addition, since several states have had budgetary shortfalls due to COVID-19 and other factors, multistate businesses are more frequently being audited by individual states’ tax authorities. If your business has international or domestic intercompany transactions, you’re facing a difficult and uphill battle amid current local, state, and federal tax regulations. The best defense against an IRS transfer pricing audit is a comprehensive transfer pricing study.

A robust transfer pricing study provides the basis with which a company can refute and push back against federal and state claims that their intercompany transactions have no economic or operational substance. As part of a transfer pricing study we will work with you to identify key classes of intercompany transactions, document the pricing of such transactions and reference comparable benchmark data sets to support qualifying transactions. Where transactions fall outside norms, we will work with you to identify differentiating characteristics and seek other data if available, or recommend policy and pricing changes, along with an assessment of the potential exposure.

Taxpayers with inadequate or out of date transfer pricing policies risk an increased likelihood of controversy and transfer pricing adjustments. Thus, even if you have had a transfer pricing study performed in the past, it is important to have it reviewed and updated.

While a transfer pricing study directly reduces a company’s risk of tax assessments and liabilities resulting from tax audits, they also indirectly reduce execution risk when a company is considering an M&A transaction, a capital raise, or go public transaction.

How MGO can help you integrate transfer pricing for the cannabis industry

MGO’s transfer pricing practice has significant experience with the various transfer pricing concerns of the cannabis industry. We also work closely with our federal and state tax practices to assist many cannabis companies with their specific tax and regulatory considerations, which include:

Section 280E disallowance of ordinary business expense deductions;

Common supply chain concerns for operators, like state restrictions on inventory and separation of cannabis and industrial hemp;

Non-plant-touching structures that operate independently from the 280E-affected business lines; and

Sales and excise taxes specific to the cannabis industry.

To learn more about how we can help support establishing, optimizing, and documenting transfer pricing policies so your business can grow in this dynamic industry, contact us.

The IRS and the Franchise Tax Board (FTB) have granted California taxpayers affected by winter storms who reside or have a principal place of business in a county where a federal disaster declaration was made more time to file tax returns and to make tax payments. Taxpayers not in a covered disaster area, but whose records necessary to meet a deadline are in one, also qualify for relief.

The tax relief postpones tax filing and payment deadlines occurring between January 8, 2023, and May 15, 2023, to a new due date of October 15, 2023.

Some of the filings and payments postponed include:

Individual income tax returns due on April 18

Business tax returns normally due on March 15 and April 18

2022 contributions to IRAs and health savings accounts

Quarterly estimated tax payments normally due January 17 and April 18

Quarterly payroll and excise tax returns normally due on January 31 and April 30

The current list of counties that qualify for this relief can be found here.

If you qualify for this postponement, you generally do not need to contact the IRS or FTB to obtain relief. Relief is automatically granted for affected taxpayers who have an address of record located in one of the designated counties. However, if you still receive a late filing or late payment notice and the notice shows the original or extended filing, payment, or deposit due date falling within the postponement period, you should call the number on the notice to have the penalty abated.

On August 16th, 2022, President Biden signed the Inflation Reduction Act (IRA) of 2022 into law. The Act is a slimmed down version of the Biden Administration’s proposed Build Back Better legislation and addresses several key areas including:

Increasing Internal Revenue Service (IRS) budget

Implementing a corporate tax minimum

Instituting and increasing tax credits focused on investing in green technologies

Notable items that were not addressed in the IRA include removing the $10,000 SALT cap and mandatory capitalization of research and development (R&D) expenses, both provisions of the Tax Cuts and Jobs Act of 2017.

The bill is over 300 pages in length with a number of wide-ranging components. In the following summary we’ll provide the key points that will be affecting taxpayers in the coming years.

Additional funding to the IRS for tax enforcement

One of the most talked-about provisions involves increased funding for the IRS.

Key details:

Approximately $80 billion in funding over the next 10 years for tax services, operations support, business system modernization, and enforcement

Enforcement – $46 billion

Operations support – $25 billion

Business systems modernization – $5 billion

Taxpayer services – $3 billion

An estimated $124 to $200 billion will be generated from enforcement and compliance efforts

Enforcement is focused on taxpayers – both corporate and non-corporate – with income greater than $400,000

Extension of the business loss limitation of noncorporate taxpayers

The IRA extends the excess business loss limitation for noncorporate taxpayers.

Key details:

Two year extension on IRC Sec. 461(l) until December 31, 2028

IRC Sec. 461(l) limits noncorporate taxpayers from deducting business losses above thresholds that are annually indexed for inflation

These limits are $540,000 for married filing jointly and $270,000 for single and married filing single for the 2022 tax year

Suspended amounts are converted to net operating losses and may be able to be used in subsequent years

Excise tax on repurchases of corporate stock

The IRA includes a 1% excise tax on stock repurchases by domestic public companies listed on an established securities market. The tax applies to repurchases executed after December 31st, 2022.

Key details:

1% excise tax on the full market value (FMV) of stock repurchased by publicly traded US corporations

Will impact redemptions and certain acquisitions and repurchases of publicly traded foreign corporation stock

Not an income tax for purposes of ASC 740

Includes special rules for “applicable foreign corporations” and “surrogate foreign corporations”

Notable exceptions:

Stock is contributed to employer sponsored retirement plan

Stock repurchase is part of a corporate reorganization

Total value of stock repurchased during the taxable year does not exceed $1 million

Repurchase by securities dealer in ordinary course of business

If the repurchase qualifies as a dividend

If the repurchase is by a regulated investment company (RIC) or a real estate investment trust (REIT)

15% corporate alternative minimum tax

The IRA reinstates the corporate alternative minimum tax (AMT) for large corporations, which had been previously eliminated by the Trump Administration’s Tax Cuts and Jobs Act.

Two key elements to note is that this revised AMT only impacts corporations with annual profits exceeding $1 billion, and includes carve-outs for certain manufacturers and subsidiaries of private equity firms.

Key details:

15% tax on adjusted financial statement income (i.e., this would be a book minimum tax)

Affects tax years beginning after December 31, 2022

Applies to corporations with profits over $1 billion based off adjusted financial income

For US corporations with foreign parents, it would apply to income earned in the US of $100 million or more of average annual earnings in three prior years and where the overall international financial reporting group has income of $1 billion or more

Treatment of split offs remains uncertain. Even though these are tax-free reorganizations for tax purposes, gain is recorded for financial accounting purposes

Joint Committee on Taxation expects that this new tax would apply to only about 150 corporate taxpayers, approximately equal to 30% of the Fortune 500

Tax credit additions and modifications

A significant number of provisions add or enhance credits and incentives that pertain to domestic research and green energy initiatives. Noteworthy changes include:

Increased small business payroll tax credits for research activities:

Qualified payroll tax credit for increasing research activities raised from $250,000 to $500,000

First $250,000 will be applied against the FICA payroll tax liability. Second $250,000 will be applied against the employer portion of Medicare payroll tax.

Applies for taxable years beginning after December 31, 2022

Limited to tax imposed for calendar quarter with unused amounts being carried forward

Qualifying small businesses are required to have less than $5 million in gross receipts in current year and no gross receipts prior to the 5 year period ending with the current year

Green initiative tax credits and incentives:

Credits for purchasing new and previously-owned clean vehicles

Extension of IRC Sec. 45L – New Energy Efficient Home Credit – extended to qualified new energy efficient homes acquired before January 1, 2033. Increase value of available credit for single-family homes to $2,500 and modified the credit available for multi-family homes.

Extension, increase, and modifications to IRC Sec. 25C nonbusiness energy property credit

Extension and modification of IRC Sec. 25D residential clean energy credit

IRC Sec. 48 energy credit for businesses and investors

Expansion of qualifying property, extension of credit including phasedown and phaseout rules, and introduction of incentives

Credit for producing energy from renewable sources (IRC Sec. 45)

Retroactive for facilities placed in service after December 31, 2021

Extends beginning of construction deadline to projects beginning construction before January 1, 2025 including solar energy facilities

Increased energy credit for solar and wind facilities in certain low-income communities

New credit for clean hydrogen production

New credit for zero-emission nuclear power

Extension of incentives for biodiesel, renewal diesel, and alternative fuels

Extension of biofuel producer credit

New income and excise tax credits allowed for sustainable aviation fuel

Modification of IRC Sec. 179D – Energy Efficient Commercial Buildings Deductions

Modification of building qualifications

Deduction increased from $1.88 per square foot to up to $5 per qualified square foot

Changes in depreciation for certain green energy properties

Final thoughts

The Inflation Reduction Act should have wide-ranging impacts on taxpayers, especially large corporations and high-net-worth individuals. In the coming weeks our tax leaders will dive into the specifics of the legislation, outline immediate and long-term impacts, and provide tax-planning strategies and considerations.

Recent events in the media have shone a spotlight on issues surrounding bad practices when it comes to tax credits and incentives. This increased attention is likely to result in an influx of audits by the Internal Revenue Service (IRS) as they crack down on the Research and Development (R&D) tax and the Employee Retention Tax Credit (ERTC) in the coming years.

We recently released an article detailing the red flags to look out when dealing with tax credits and incentives providers. If you think you could be at risk for future IRS issues, there is much you can do now to take a proactive approach and mitigate future negative impact. In the following, we break down steps you can take now to better understand and manage your exposure.

An overview of tax credits and incentives

Designed to encourage investment and development, job creation, growth, and certain business activities, tax credits and incentives provide an opportunity to reduce the amount of tax owed for performing certain activities. Credits and incentives are categorically different than tax deductions, which reduce the amount of taxable income.

These incentives often target desirable industries or activities like research and development, job creation for at-risk populations, and expanded growth in underdeveloped areas. When leveraged correctly, credits and incentives can be a powerful tool to funnel back resources into your organization to fuel activities you are already doing. Even more enticing, these credits can often apply retroactively if you determine you qualify for certain credits or incentives after the fact.

There are three basic types of tax credits: nonrefundable, refundable, and partially refundable. A few of the different types of tax credits pertaining to businesses in different classifications, industries, or activities performed include R&D tax credits, the employee retention tax credits, IRC Section 179D, and the work opportunity tax credit. To learn more about their eligibility rules, visit our previous article.

Understanding the risk of IRS tax audits

There is a three-year statute of limitations from the due date of the tax return or the filing date (whatever is later) for the IRS to assess your filings. That means if you think you may be exposed but escaped the IRS’ notice, you could still receive an audit notice for previous years’ returns. And if you do get audited, and the IRS determines you owe back taxes, you will get charged penalties and interest dating back to the infraction itself.

This is even more risky when considering the IRS’s extreme backlog. These IRS tax audits can sometimes take years to complete and if your credit and incentive calculations are the topic of interest, you’ll need to halt any future credit analysis until the situation is resolved. Meanwhile, you’ll be devoting crucial resources, time, and effort working with the IRS for something that yields no financial value and distracts from more conducive business activities.

Reasons to get a head-start and address issues now

Even though there is no guarantee you will get audited, you are still taking a risk if you do not address potential tax credit and incentive exposures in your organization. It may seem easy to “roll the dice” and hope the issue will remain uncovered, but it could come at a cost — especially if you are planning to make some big moves, like engaging in transaction of your business (M&A), going public, or embarking on another major transaction.

During the due diligence period of these transactions, it is almost certain any uncovered tax issues will emerge. You will likely not recover the value of these credits or remain on the hook for potential liability. Even worse, the exposure of these issues reflects negatively on your accounting and control system, potentially lowering the purchase value of your organization or undermining whatever deal you had in place prior to the due diligence. Often your transaction partners will start to question your organization’s trustworthiness, and reputation … due to something that may be no fault of your own.

So, you’ve been exposed … but haven’t received an IRS audit notice

Here is the deal: you know for certain you have been exposed, but you have not been notified by the IRS yet. You probably have a lot of questions — will you get an audit notice? Have you escaped unscathed? Do you need to address the issues preemptively, just in case? It may be overwhelming to decide how to proceed once you realize the exposure.

We suggest working with a qualified CPA firm to review your tax filings. A full-service accounting firm will review your organization holistically at a minimum rate, uncover any exposures, and deliver valuable peace of mind. If the firm does find issues, you have two options:

Update your credit and incentive filings moving forward.

While this will likely decrease the amount you can deduct, it exemplifies transparency.

Issue a Voluntary Disclosure (VA) if the exposure is significant and you do not have a lot of time to fix the issue.

Essentially, you are volunteering to correct your mistakes by recalculating the credits claimed and paying back the difference.

While this may sting a little, the IRS looks favorably upon organizations who are proactive to fix the issue by filing a VA and they are likely to waive any penalties or interest you would have had to pay.

You’ve received an IRS audit notice. Now what?

Well, it happened. You received an audit note from the IRS. Before you panic, here is what you need to do:

Start preparing your documentation right away. The sooner you have your ducks in a row, the sooner you are prepared to handle the audit.

Check the contract you signed with your original provider and verify if they provide controversy support services for situations like these.

If they do, reexamine the quality of their work. Do they have any of the red flags mentioned in this article? Could something they have done have caused the audit?

Consider engaging a qualified CPA firm as your new provider to handle the subsequent controversy support. Someone you trust can get you ready for any available credits and incentives moving forward, too.

If you used a provider that displays any red flags, you could have some leverage for a reasonable cause defense. Because the “professional” firm handled it for you and made a mistake, you could utilize a first-time penalty abatement, which means you can get relief from a penalty if you:

Did not previously have to file a return or if you do not have any penalties for the three years before the tax year you received a penalty;

Filed all currently required returns or an extension of time to file; and

Paid or have arranged to pay any tax due.

Verify your contract with the original provider to determine if you have any recourse to seek compensation from them. If the IRS does issue any penalties, you will want to ensure you do not have to pay.

Standalone firms vs. full-service accounting firms

Let’s say you haven’t received an IRS notice, and you do not think you are in danger of receiving one. How can you ensure you will not in the future? It comes down to choosing a firm to help you maximize the potential of these tax credits and incentives.

The bottom line: it is imperative you work with a certified public accounting (CPA) firm instead of a standalone firm. Because standalone firms often use lower-cost, less-experienced recent graduates who are not certified public accountants, there is a distinct lack of knowledge and background in the accounting fundamentals, causing you to be misled by those unequipped to help with complex tax matters. You also run the risk of being oversold benefits by aggressive firms that not only exaggerate the amount you are receiving from the tax credits and incentives, but also behave in a way that attracts IRS attention and jeopardizes your firm.

A full-service accounting firm, on the other hand, knows how to look at an organization holistically — and it has many more capabilities and professionals with experience. It looks at things through various lenses and can advise how certain positions will impact current and future tax positions. Full-service firms also likely have an in-house controversy team that has handled hundreds of audits successfully—so you will be in good hands.

Our perspective

Tax credits and incentives provide plenty of benefits you do not want to miss out on, and their often-complex application and qualification processes are reason enough to hire a professional accountant to help you maximize your returns. Unfortunately, we often see organizations placing their trust in the wrong providers and they end up suffering the consequences of an IRS audit. For many, it is simply easier and safer to cut off the relationship with the initial provider and start fresh with a professional firm you know you can trust.

At MGO, our dedicated Tax Credits and Incentives team brings more than 30 years of experience fixing these types of issues and working with the IRS to limit the damage. We provide cleanup in the event you are being audited by the IRS (or could be audited in the future), and help you identify areas where you can claim tax credits and incentives for next time. If you are concerned, our best advice is to get ahead of it with an opinion you can trust — before the IRS decides to investigate themselves.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

Tax credits and incentives are an often underutilized, yet powerful tool to help you improve your bottom line and reinvest in your business – all while substantially reducing your tax exposure.

In recent years, a number of firms have emerged specializing in credits and incentives and building large businesses by over-promising and under-delivering these tax consulting services. While credits and incentives are enticing, they must be handled with extreme care, as the consequences of getting it wrong can be serious.

At MGO, we not only help you determine if you are eligible for these valuable tax credits and incentives, but we also perform damage control and clean-up following bad actors’ broken promises and sloppy work. We have seen firsthand the fallout from their poor performance and how it affects clients. In this article, we will help you understand what to look for in a tax credits and incentives provider and recognize and avoid IRS red flags so you can safely capitalize on these opportunities.

An overview of tax credits and incentives

Designed to encourage investment and development, job creation, growth, and certain business activities, tax credits and incentives provide an opportunity to reduce the amount of tax owed for performing certain activities. Credits and incentives are categorically different than tax deductions, which reduce the amount of taxable income.

These incentives often target desirable industries or activities like research and development, job creation for at-risk populations, and expanded growth in underdeveloped areas. When leveraged correctly, credits and incentives can be a powerful tool to funnel back resources into your organization to fuel activities you are already doing. Even more enticing, these credits can often apply retroactively if you determine you qualify for certain credits or incentives after the fact.

There are three basic types of tax credits: nonrefundable, refundable, and partially refundable. Here, we break down just a few of the different types of tax credits pertaining to businesses in different classifications, industries, or activities performed:

Designed to incentivize innovation, this dollar-for-dollar tax savings has both Federal and State-level implications and can save you up to 15% on qualifying activities. To claim an R&D tax credit, your company must pass a four-part test and be involved in the technical development of new or improved products or processes. This can apply to product enhancements, product development, software development, process improvements, and more.

The ERTC was created to provide much-needed financial relief for businesses affected by the COVID-19 pandemic. With complex eligibility requirements, the refundable tax credit awards qualifying employers with a payroll tax credit of up to $26,000 per employee as an incentive to retain them on payroll through potential closures, quarantines, and other hardships. Since its rollout, the ERTC has been expanded to continue providing relief to an even larger group of employers, even retroactively (albeit with a smaller maximum amount per employee for 2021).

IRC Section 179D

This popular tax incentive gives designers, builders, and building owners the opportunity to obtain a tax deduction of up to $1.80 per square foot if they install eligible energy efficient buildings and systems that reduce the power and energy costs by 50% or more compared to the minimum standard requirements. Tenants are eligible if they make the construction changes, and the deduction can be claimed on both retrofits and new construction projects. Buildings that qualify include commercial buildings like parking garages and warehouses, government-owned buildings like universities and libraries, and apartment buildings with four stories or more.

Work Opportunity Tax Credit

A federal tax credit for employers looking to invest in American job seekers who face barriers to acquiring employment, the WOTC is claimable if the employer 1) meets their business needs, and 2) does so by hiring an employee from a WOTC targeted group (which include veterans, ex-felons, and qualified long-term unemployment recipients, among others). An employer interested in claiming this credit must verify the new hire is a member by applying and receiving a certification.

Risks associated with claiming tax credits and incentives

While there are many benefits to tax credits and incentives, there are a few risks attached to claiming them on your tax return.

One risk is exposing your organization to an IRS audit. An audit does not always mean trouble — at least, not if you are doing everything right — but having to go through the process of complying means you are devoting time and effort to something that yields no financial value, ultimately draining resources from more conducive business activities. Working with IRS representatives and organizing and submitting documentation is labor-intensive.

A significant issue to note is that if you overstate your credits, the IRS’s software may flag the subsequent higher score for the return, sparking an audit — so claim succinctly and accurately. Then, of course, there is the issue of an audit exposing issues unrelated to your tax credits, making you vulnerable to even bigger problems.

Another risk is payback. Tax credits do not have payback requirements, but some tax incentives do, and along with them come penalties for failing to pay in a timely manner. You may also then accrue interest, which can add up quickly. This negates the incentives in the first place, only causing a bigger headache.

Red flags to look for in tax credit and incentive providers

To maximize the potential of the credits, working with a certified public accounting (CPA) firm is absolutely essential. Non-CPA firms do not have to adhere to strict accounting guidelines. Additionally, they may not have the requisite experience or perspective to assess your situation holistically. A trained and licensed professional will examine your operations, uncover missed opportunities, and help you capitalize on a lower tax liability. But choosing unwisely can have major ramifications and increase your chances of being audited by the IRS.

Here are some of the most important red flags to look for when selecting a provider:

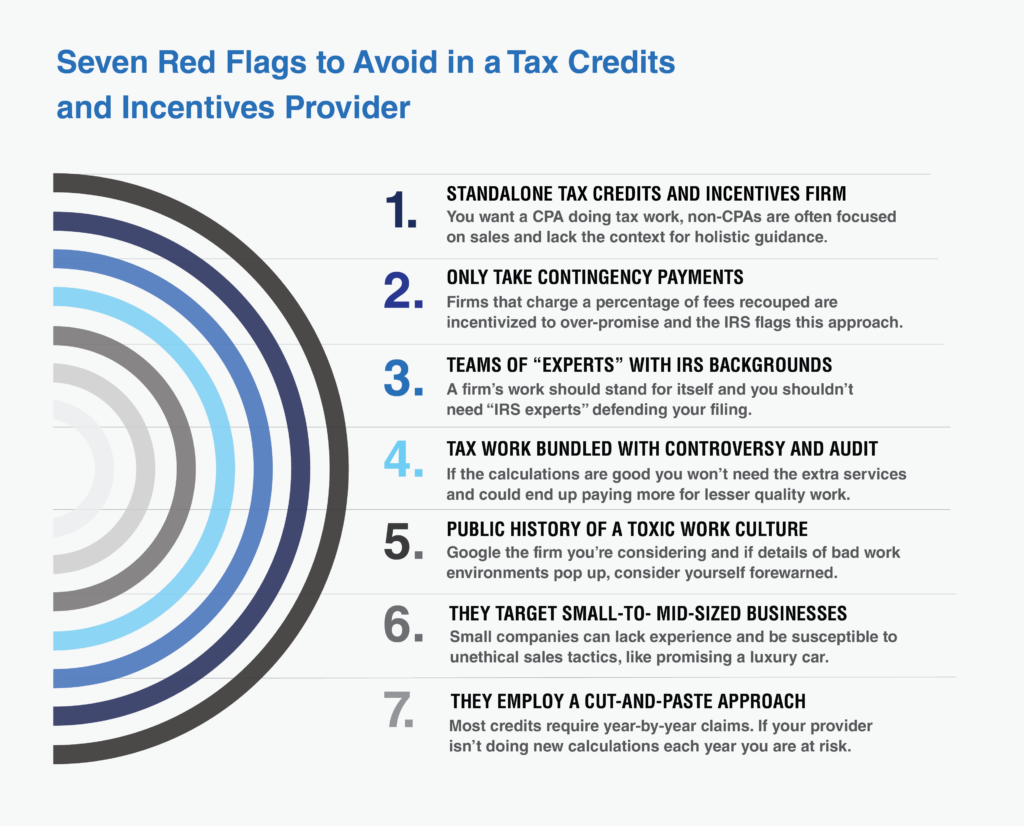

1. Standalone tax credits and incentives firm

Firms that do not utilize CPAs often use lower-cost, less-experienced recent graduates who act more in a sales-focused capacity than as an accountant. This lack of knowledge and background in accounting fundamentals can result in you being misled by someone who is not equipped to help with complex tax matters.

2. They only take contingency-based payments

Stay away from firms that take 25-35% of the savings recouped in fees. This is a sales approach that is commission-based by maximizing your credit, and you can assume they are being incentivized by these fees to over-promise — which means they will almost certainly underdeliver. Another negative? If an auditor sees your tax provider takes contingency-based payments, they will automatically assume they are acting in bad faith and then comb through your past credits to verify their accuracy. And they can look through your last three tax returns, making you even more vulnerable.

3. They market a team of “experts” with IRS or legislative backgrounds

Look out for firms that tout their employees as experts who have specialized backgrounds tailored to helping you get your tax credits. Whether or not they actually have IRS or legislative backgrounds, at the end of the day, a firm’s work should speak for itself. There is no need for flashy marketing collateral that boasts expertise without proof.

4. They bundle tax work with controversy and audit support

A combo deal is great when it is a burger, fries, and a Coke, but when it comes to your tax work, you should be looking for individualized support. Firms that package tax work with controversy and audit support are trying to catch your eye, saying, “Look at everything we can offer you!” If the tax assessment they provide is strong, these packages are not necessary and you’re paying for something you shouldn’t need in the first place.

5. There is a history (often public) of a toxic work culture

Do not be afraid to Google the firm you are considering. If several articles pop up detailing sordid work environments that include sexual harassment; lawsuits against former clients and employees; and obviously fake Glassdoor reviews, you can assume the firm itself is a red flag.

6. Targeting of less-sophisticated businesses as clients

Be aware of firms that go after mid-market and below businesses that are less “sophisticated” than other potential clients. They will usually peddle less-than-legitimate sales tactics, like promising a Porsche or other luxury vehicle, as an incentive to lure these businesses into hiring them. Red flag firms know less refined companies will not catch on to these “scummy” offers because they do not have the experience to know any better.

7. They employ a “cut-and-paste” approach

Many tax credits, like the R&D tax credit, require year-by-year claims, and in order to qualify, your tax return must depict work calculated and substantiated independent of years past. If a firm utilizes the “cut-and-paste” approach from the year before, this indicates sloppy work — and a red flag indicating you should choose a tax provider willing to perform the work necessary year after year without cutting corners and risking an IRS audit.

Keys to selecting a reliable tax credits and incentives provider

Now that you know what to avoid, here are some things a tax provider should have in order to best assist you with tax credits:

1. They are a full-service accounting firm.

A full-service accounting firm knows how to look at an organization holistically, providing the services necessary simply by peering beneath the hood. They will know how things work, and we are happy to tell you how to optimize — including how tax credits can be used or monetized within your business. Look for a firm that provides tax, audit, controversy, and more services, all under one roof.

2. They prioritize the security of your information.

A good tax provider knows your information is sacred and will treat it as such. While cybersecurity risks are never fully eliminated, stick with a firm with SOC or equivalent data protection. This way you are much less likely to have your sensitive financial information exposed in the event of a data breach.

3. They employ quality control

Look for a firm that utilizes multiple levels of internal review, so you know that the work you are getting has been vetted and approved by a strong system of quality control — all with your best interests in mind. When you are dealing with something like tax credits, you cannot take the easy way out or cut corners, so finding a provider that maintains control strength is crucial.

4. They never make a decision for you

While you want to trust your tax provider, at the end of the day, whatever decisions your organization makes regarding your tax credits affects you and only you. A reliable firm will not pressure you into questionable decisions. They will empower you through thorough education so you can feel confident making the right choice yourself.

5. They charge you a fixed rate based on hours worked

Unlike a red-flag firm, the firm you want to hire only charges a fixed rate based on the hours they work for you, rather than contingency-based charges taken from the recoup. This indicates they are focused on the outcome for you, not what that return means for them. A firm like MGO will perform an initial fact-find to determine eligibility and then make a conservative estimate, so you know exactly what to expect.

6. They follow a professional approach

Professional means qualified, and a good firm provides services from specialists with real certifications and strong backgrounds in the industry. Look for a tax provider that regularly publishes news, articles, and thought leadership detailing emerging opportunities and risks. The team you hire is embarking on a journey with you — and to create opportunities, gain competitive advantages, and see your hard work culminate in rewards, you want to work with someone you can trust: someone proactive and well-informed.

Our perspective on ethics in tax credits and incentives

Tax credits and incentives provide plenty of benefits you do not want to miss out on — and their often-complex application and qualification processes are reason enough to hire a tax provider to help you maximize your returns. However, it is important to be aware that not just any tax provider will do. Be aware of red flags and know what specifically to look for in a firm.

At MGO, our dedicated Tax Credits and Incentives team brings over 30 years of experience. We will take a holistic view of your operations and processes to identify areas where you may be able to claim tax credits and incentives.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

The IRS recently issued its 2022 cost-of-living adjustments for more than 60 tax provisions. With inflation up significantly this year, mainly due to the COVID-19 pandemic, many amounts increased considerably over 2021 amounts. As you implement 2021 year-end tax planning strategies, be sure to take these 2022 adjustments into account.

Also, keep in mind that, under the Tax Cuts and Jobs Act (TCJA), annual inflation adjustments are calculated using the chained consumer price index (also known as C-CPI-U). This increases tax bracket thresholds, the standard deduction, certain exemptions and other figures at a slower rate than was the case with the consumer price index previously used, potentially pushing taxpayers into higher tax brackets and making various breaks worth less over time. The TCJA adopts the C-CPI-U on a permanent basis.

Individual income taxes

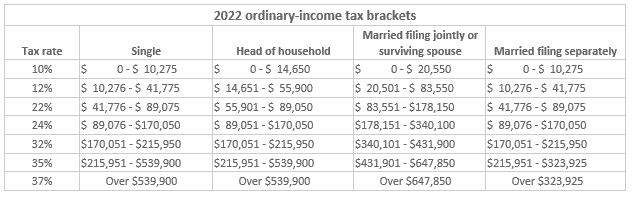

Tax-bracket thresholds increase for each filing status but, because they’re based on percentages, they increase more significantly for the higher brackets. For example, the top of the 10% bracket increases by $325 to $650, depending on filing status, but the top of the 35% bracket increases by $16,300 to $19,550, again depending on filing status.

The TCJA suspended personal exemptions through 2025. However, it nearly doubled the standard deduction, indexed annually for inflation through 2025. For 2022, the standard deduction is $25,900 (married couples filing jointly), $19,400 (heads of households), and $12,950 (singles and married couples filing separately). After 2025, standard deduction amounts are scheduled to drop back to the amounts under pre-TCJA law unless Congress extends the current rules or revises them.

Changes to the standard deduction could help some taxpayers make up for the loss of personal exemptions. But it might not help taxpayers who typically used to itemize deductions.

Alternative minimum tax

The alternative minimum tax (AMT) is a separate tax system that limits some deductions, doesn’t permit others and treats certain income items differently. If your AMT liability is greater than your regular tax liability, you must pay the AMT.

Like the regular tax brackets, the AMT brackets are annually indexed for inflation. For 2022, the threshold for the 28% bracket increased by $6,200 for all filing statuses except married filing separately, which increased by half that amount.

The AMT exemptions and exemption phaseouts are also indexed. The exemption amounts for 2022 are $75,900 for singles and heads of households and $118,100 for joint filers, increasing by $2,300 and $3,500, respectively, over 2021 amounts. The inflation-adjusted phaseout ranges for 2022 are $539,900–$843,500 (singles and heads of households) and $1,079,800–$1,552,200 (joint filers). Amounts for separate filers are half of those for joint filers.

Education and child-related breaks

The maximum benefits of certain education and child-related breaks generally remain the same for 2022. But most of these breaks are limited based on a taxpayer’s modified adjusted gross income (MAGI). Taxpayers whose MAGIs are within an applicable phaseout range are eligible for a partial break — and breaks are eliminated for those whose MAGIs exceed the top of the range.

The MAGI phaseout ranges generally remain the same or increase modestly for 2022, depending on the break. For example:

The American Opportunity credit. For tax years beginning after December 31, 2020, the MAGI amount used by joint filers to determine the reduction in the American Opportunity credit isn’t adjusted for inflation. The credit is phased out for taxpayers with MAGI in excess of $80,000 ($160,000 for joint returns). The maximum credit per eligible student is $2,500.

The Lifetime Learning credit. For tax years beginning after December 31, 2020, the MAGI amount used by joint filers to determine the reduction in the Lifetime Learning credit isn’t adjusted for inflation. The credit is phased out for taxpayers with MAGI in excess of $80,000 ($160,000 for joint returns). The maximum credit is $2,000 per tax return.

The adoption credit. The phaseout ranges for eligible taxpayers adopting a child will also increase for 2022 — by $6,750 to $223,410–$263,410 for joint, head-of-household and single filers. The maximum credit increases by $450, to $14,890 for 2022.

(Note: Married couples filing separately generally aren’t eligible for these credits.)

These are only some of the education and child-related breaks that may benefit you. Keep in mind that, if your MAGI is too high for you to qualify for a break for your child’s education, your child might be eligible to claim one on his or her tax return.

Gift and estate taxes

The unified gift and estate tax exemption and the generation-skipping transfer (GST) tax exemption are both adjusted annually for inflation. For 2022, the amount is $12.060 million (up from $11.70 million for 2021).

The annual gift tax exclusion increases by $1,000 to $16,000 for 2022.

Retirement plans

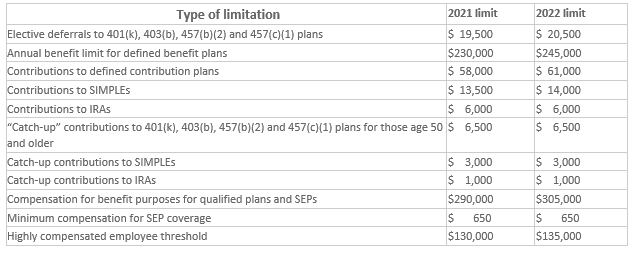

Not all of the retirement-plan-related limits increase for 2022. Thus, depending on the type of plan you have, you may have limited opportunities to increase your retirement savings if you’ve already been contributing the maximum amount allowed.

Your MAGI may reduce or even eliminate your ability to take advantage of IRAs. Fortunately, IRA-related MAGI phaseout range limits all will increase for 2022:

Traditional IRAs. MAGI phaseout ranges apply to the deductibility of contributions if a taxpayer (or his or her spouse) participates in an employer-sponsored retirement plan:

For married taxpayers filing jointly, the phaseout range is specific to each spouse based on whether he or she is a participant in an employer-sponsored plan:

For a spouse who participates, the 2022 phaseout range limits increase by $4,000, to $109,000–$129,000.

For a spouse who doesn’t participate, the 2022 phaseout range limits increase by $6,000, to $204,000–$214,000.

For single and head-of-household taxpayers participating in an employer-sponsored plan, the 2022 phaseout range limits increase by $2,000, to $68,000–$78,000.

Taxpayers with MAGIs in the applicable range can deduct a partial contribution; those with MAGIs exceeding the applicable range can’t deduct any IRA contribution.

But a taxpayer whose deduction is reduced or eliminated can make nondeductible traditional IRA contributions. The $6,000 contribution limit (plus $1,000 catch-up if applicable and reduced by any Roth IRA contributions) still applies. Nondeductible traditional IRA contributions may be beneficial if your MAGI is also too high for you to contribute (or fully contribute) to a Roth IRA.

Roth IRAs. Whether you participate in an employer-sponsored plan doesn’t affect your ability to contribute to a Roth IRA, but MAGI limits may reduce or eliminate your ability to contribute:

For married taxpayers filing jointly, the 2022 phaseout range limits increase by $6,000, to $204,000–$214,000.

For single and head-of-household taxpayers, the 2022 phaseout range limits increase by $4,000, to $129,000–$144,000.

You can make a partial contribution if your MAGI falls within the applicable range, but no contribution if it exceeds the top of the range.

(Note: Married taxpayers filing separately are subject to much lower phaseout ranges for both traditional and Roth IRAs.)

2022 cost-of-living adjustments and tax planning

With many of the 2022 cost-of-living adjustment amounts trending higher, you have an opportunity to realize some tax relief next year. In addition, with certain retirement-plan-related limits also increasing, you have the chance to boost your retirement savings. If you have questions on the best tax-saving strategies to implement based on the 2022 numbers, please give us a call. We’d be happy to help.

On October 15, 2021, the Chief Counsel’s office released memorandum number 20214101F in response to questions from IRS officials in the Large Business & International division and the Small Business/Self-Employed division about what information taxpayers should provide with their claims for refunds or tax credits and what format they should use.

What qualifies a taxpayer for the R&D refund claim?

In short, the IRS stated that for a taxpayer’s R&D refund claim to be valid, the taxpayer must, at a minimum:

Identity all the business components to which the I.R.C. § 41 research credit claim relates for that year.

For each business component:

identify all research activities performed,

identify all individuals who performed each research activity, and

identify all the information each individual sought to discover through the activities performed.

Provide the total qualified employee wage expenses, total qualified supply expenses, and total qualified contract research expenses for the claim year (this may be done using Form 6765, Credit for Increasing Research Activities).

These statements reconfirm the standard that a business components list (often referred to as a project list) is a fundamental necessity for filing research credit claims. For each business component taxpayers need to identify all the research activities they’ve performed, name the individuals who performed each research activity, and include the information each individual sought to discover. In other words, each business component must satisfy the elements set forth in I.R.C. § 41.

What’s new: the Specificity Requirement

The memorandum also includes a new requirement referred to as the specificity requirement. This is a jurisdictional prerequisite to filing a suit for refund, entailing taxpayers to provide the facts in a written statement to support any refund claims. For the claim or refund to be considered, the statement of the grounds and facts must be verified by a written declaration stating it is made under the penalties of perjury. The taxpayer’s signature on the amended return constitutes the declaration under the penalties of perjury for what is contained in the claim and what is attached to it.

The written statement must be submitted when a refund claim is filed. Otherwise, the refund claim should be rejected as deficient.

This new requirement is said to enable the Service to determine if a refund should be paid immediately based on the information provided or if an examination is needed to verify the taxpayer’s entitlement to the refund. This information helps the Service avoid paying refunds to taxpayers who have no factual support for their claim and allows the Service to effectively allocate its limited resources to determining which procedurally compliant claims to examine.

What’s the timing of this new requirement?

The additional information will now be required for all research credit claims made after a grace period ending January 10, 2022. A one-year transition period will be provided following this grace period to allow taxpayers 30 days to perfect a research credit claim before the IRS makes a final decision.

Generally, taxpayers are expected to file valid claims within three years of the date that the tax return was filed—or two years from the time the tax was paid, whichever is later. All additional requirements must be met.

How we can help

R&D credit claims often result in examinations, a process that is costly and burdensome to both the Service and taxpayers. MGO is here to help taxpayers determine their eligibility for R&D tax credits and develop and implement procedures to document R&D activities before claims are made, to ensure a smooth filing process.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology s

When the IRS first came up with the Research and Development (R&D) Tax Credit, the industries it impacted were primarily scientific organizations and lab-based research companies. Today, eligibility has expanded to the point that most businesses in almost every industry can claim the credit, if they are performing research, and importantly, documenting it.

The R&D credit is a valuable tax tool, but it is complex and has attracted the attention of the IRS from the beginning. As recently as July 2021, the IRS made it clear that it was continuing to focus on those claiming the credit especially as it relates to the substantiation of qualified research. But attention from the IRS shouldn’t dissuade eligible businesses from claiming it.

Qualifying for the R&D credit

There are four requirements to qualify for the R&D credit. The business activities must:

Be intended to eliminate technical uncertainty about the development or improvement of a product or process

Constitute a process of experimentation

Be technical in nature and adhere to the standards of hard science

Relate to the development of a new or improved business component

Of all the qualifying requirements, the one that seems to create the most challenges for small businesses is documenting the process of experimentation (POE) in R&D projects.

Product development process

Having a well-documented product development process is just good business practice, but it also makes an IRS audit considerably smoother. If your business follows regulatory or industry standards on how products should be developed and tested, your documentation work is essentially done. However, even without formal industry standards, outlining how products are created, tested, and released will provide the information required by the IRS to demonstrate that you have a formal POE.

Documenting your POE

So, what does the IRS consider proper documentation of your POE? There are a few basic elements that will help make your case to the IRS. • Project accounting systems that track employee time and project costs provide the level of detail the IRS values. • Technical project documentation that highlights the process. • Technical documentation such as design drawings and revisions, patent applications, regulatory submissions, product tracking, and workflow logs.

The best practice for R&D credit documentation is to compile them systematically as you produce them, so you don’t need to search for them later or recreate them. If you clearly define, document, and allocate costs to the specific business components, claiming the tax credit can be a reasonably smooth process.

How we can help

MGO helps organizations across a wide range of industries develop and implement procedures to document their R&D activities. We help clients demonstrate their eligibility for the R&D credit and claim the credit available.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors. He can be reached at [email protected].

On August 28, 2020, the IRS issued Notice 2020-65 that provides some needed guidance for employers wondering whether and how to comply with the employee payroll tax deferral described in the August 8, 2020 Presidential memorandum (often referred to as an “executive order”). Although many questions remain unanswered, some key items are addressed.

Background on the Executive Order

In an August 8, 2020 memorandum to the Secretary of the Treasury entitled, “Deferring Payroll Tax Obligations in Light of the Ongoing COVID-19 Disaster,” President Trump directed Treasury Secretary Mnuchin to use his authority to defer the withholding, deposit and payment of employee Social Security tax on wages (i.e., 6.2% of employee wages) or Railroad Retirement tax on compensation paid to certain employees during the period September 1 through December 31, 2020. The memorandum instructed the Treasury Department to issue guidance explaining how to implement the deferral and to explore avenues, including legislation, to eliminate the obligation to pay the deferred taxes. Secretary Mnuchin made comments in an August 10 interview that employers would not be required to offer the deferral.

Drawing a line between mandatory and voluntary tax deferral

One of the most pressing questions following the President’s executive order was whether organizations were required to, or could opt-out, of the payroll tax deferral. Although the IRS Notice does not specifically state whether the employee payroll tax deferral is mandatory, the deferral appears to be voluntary, which lines up with Treasury Secretary Mnuchin’s widely reported comments.

Internal Revenue Code Section 7508A (which is the basis for the memorandum and the Notice) allows the President to postpone certain tax deadlines due to a disaster, such as COVID-19. However, Section 7508A does not give the President authority to require taxpayers to use the extended deadline. In other words, even if a deadline is postponed, a taxpayer could continue to adhere to the normal deadlines. As a result, employers can continue to withhold employee Social Security tax or Railroad Retirement tax from September 1 to December 31, 2020 if they do not wish to avail themselves of the deadline extension.

The Notice clearly places responsibility on employers for withholding and depositing the deferred taxes, and states that penalties generally would apply for any failure to comply (although the Notice states that employers can “make arrangements to otherwise collect the total Applicable Taxes from the employee”). Neither the memorandum nor the Notice eliminates the tax liability.

It appears that the employee payroll tax deferral does not apply to self-employed individuals, since it only applies to Social Security tax and Railroad Retirement tax and does not include Self-Employment Contributions Act (SECA) taxes.

Too late for many employers to benefit from deferral option

Since the guidance was released so close to the first available deferral date (i.e., September 1), employers have very little time to modify payroll procedures and payroll systems to allow employees the deferral on the first pay cycle in September.

Under the current IRS rules, it is not possible to “recover” the tax that already was withheld and remitted, but was eligible for the deferral, without causing issues with the employer tax filings and the imposition of penalties. Retroactive changes generally are not allowed simply because a taxpayer failed to use an available extension. This is consistent with the IRS’s position on employers that failed to timely defer the employer’s share of Social Security taxes (6.2%) as permitted under the CARES Act.

Key insights from the IRS guidance

The following are summaries of key points from the IRS issuance.

Dates and Eligibility

The employee payroll tax deferral applies to wages and compensation paid on a pay date during the period beginning on September 1, 2020 and ending on December 31, 2020.

The employee payroll tax deferral applies only if wages or compensation paid to an employee for a biweekly pay period are less than $4,000, or the equivalent amount with respect to other pay period frequencies. This threshold is determined on a pay period-by-period basis.

What it means: Employees who are paid hourly or whose wages vary from pay period to pay period may not benefit from the payroll tax deferral in every pay period depending on whether the amount of wages exceeds the biweekly threshold of $4,000, or the equivalent. Employers should review with their IT departments or payroll service providers to ensure that the payroll system is configured correctly to determine who is eligible to participate in the employee payroll tax deferral on a pay period-by-pay period basis.

Deferral and Repayment Periods

The due date for the deferred withholding and payment of the employee Social Security tax and Railroad Retirement tax is postponed until the period beginning on January 1, 2021 and ending on April 30, 2021.

Employers are responsible for the deferred taxes and must withhold and pay the deferred taxes ratably from wages and compensation paid between January 1, 2021 and April 30, 2021 or interest, penalties and additions to tax will begin to accrue on May 1, 2021 with respect to any unpaid deferred taxes. If the employee’s wages are not sufficient for the withholdings, the employer can pursue payment from the employee.

What it means: The very short-term deferral and repayment period results in a modest benefit.

For example: An employee who earns the Federal minimum wage would have an increased biweekly paycheck of $36 (or $324 for nine pay periods, from September 1 to December 31, 2020).

For employees that earn the maximum $3,999 every two weeks for nine pay periods, the benefit is $2,231. ($3,999 x 6.2% x 9 pay periods).

Unless something happens to dramatically improve the employee’s household income before January 1, 2021, the repayment of taxes ratably over the first four months of 2021 may create a greater hardship than their current cash flow shortage.

The dilemma facing employers

Many questions remain in terms of how the employee payroll tax deferral will impact employees and employers, how the deferred payroll taxes are to be reported and what changes must be made to an employer’s payroll system. Until the IRS provides further guidance regarding these outstanding questions and concerns, employers that consider implementing the employee payroll tax deferral should exercise care by putting safeguards in place to ensure that they do not fall victim to the IRS penalties.

Since the employee payroll tax deferral takes effect as early as September 1, 2020, employers that consider implementing the tax deferral likely will face a dilemma due to some of the unanswered questions unless the IRS issues additional guidance soon. For example:

Can a participating employer apply the same deferral policy to all employees, or must the employees be allowed to choose?

What are the consequences if an employee unexpectedly leaves the employer before paying the deferred tax?

If the employer cannot collect the taxes from former employees, is the employer liable for the tax or failure to withhold penalties?

What if the employee does not earn enough wages during the period between January and April of 2021 due to disability, leave of absence, etc., to pay for the deferred tax?

Does the employer report the deferred payroll tax as tax withheld on the employer’s quarterly tax returns (i.e., Form 941) and Forms W-2?

What happens if the employer did not defer the payroll tax, but the government later decides to forgive the deferred taxes? Will the employer or the employees be able to recover the tax that would have been forgiven had the tax been deferred?

Will the IRS provide a mechanism (e.g., revising the employer’s Form 941) to allow employers to “recover” the tax that was already withheld and remitted, but was eligible for the deferral, without causing issues with the employer tax filings and incurring penalties?

What if an employee receives a supplemental wage payment (e.g., bonus) outside of a normal pay period, how will that be treated for the purpose of the $4,000 eligibility threshold?

We will continue to provide updates on the Employee Payroll Tax Deferall program as more information becomes available. If you are unclear on the impact on your organization, or you would like a consultation, please reach out to our dedicated tax team: contact us now