Many professional athletes go on to achieve even greater financial success in their lives after sports through pro-active financial planning and capitalizing on post-career opportunities.

Having the right financial advisory team is crucial for transitioning athletes to make smart money decisions across areas like investments, business ventures, taxes, estate planning, and risk management.

With proper guidance, athletes can turn their playing careers into lifelong financial stability and growth through entrepreneurship, investments, and other lucrative second careers.

~

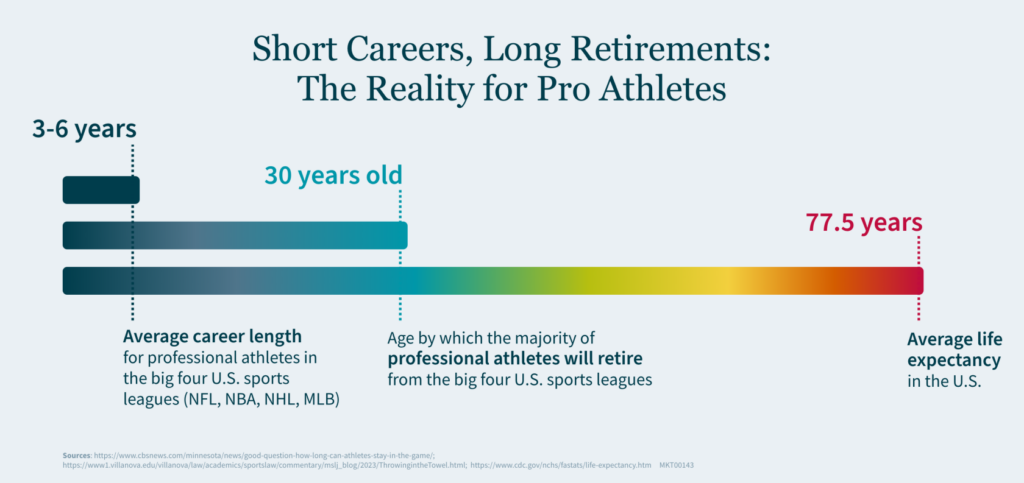

As a professional athlete, you’ve spent years honing your skills, building your career, and making a name for yourself. But what happens when the final whistle blows and your playing days are behind you?

The good news is many athletes move on to highly successful and lucrative ventures after their time in sports — some even making more money than they did during their athletic careers. With the right financial support and strategic planning, you can be one of them.

From Athlete to Entrepreneur: Maximizing Post-Career Opportunities

The transition to life after sports can be incredibly rewarding, opening doors to new and exciting opportunities. Many professional athletes have not only avoided the financial pitfalls often associated with post-career life but have also thrived financially.

Here are a few notable examples of athletes who’ve achieved significant financial success with their second careers:

Kenny Smith

Kenny “The Jet” Smith played 10 years in the National Basketball Association (NBA), winning back-to-back championships with the Houston Rockets in 1994 and 1995. While Smith made just under $12 million over his playing years, as an analyst on the Inside the NBA alongside Ernie Johnson, Charles Barkley, and Shaquille O’Neal, Smith reportedly takes home $16 million per year.

Maria Sharapova

While Sharapova earned over $300 million during a career where she became just the tenth woman to win all four major championships, she retired at the young age of 32 in 2020. Since that time, she has established herself as an investor and entrepreneur — working with health and wellness brands like Therabody and Tonal — while also serving on the board of directors for luxury fashion house Moncler Group.

Derek Jeter

Jeter played 20 seasons at shortstop for the New York Yankees, winning 5 World Series titles before retiring in 2014. After earning over $265 million in MLB salary, Jeter went on to found Jeter Publishing with Simon & Schuster and the media company The Players’ Tribune in 2014, which publishes first-person stories from athletes. From 2017, he became part-owner and CEO of the Miami Marlins.

David Beckham

Playing 21 seasons of professional soccer for teams like Manchester United, Real Madrid, the LA Galaxy, Beckham racked up league titles and millions in contract dollars. Retiring in 2013, he transitioned into a successful business career — starting the management company DB Ventures and collaborating with brands like HUGO BOSS. In 2018, Beckham brought Major League Soccer to Miami as co-owner of Inter Miami CF.

These examples demonstrate the wealth creation potential that exists long after an athletic career ends. Of course, it’s not just about what you do after your playing days are over; it’s also about what you do with your money.

The Role of Financial Advisors in Your Post-Career Success

The right financial advisors can help you navigate the complex financial landscape, assisting you to make smart decisions that will benefit you in the long term. Here are some key areas where advisors can support you:

Investment Planning

Post-career, it’s essential to make your money work for you. Financial advisors can help you develop a diversified investment portfolio tailored to your risk tolerance and long-term goals. This could include stocks, bonds, real estate, and business ventures.

Business Ventures

Many athletes transition into entrepreneurship. Advisors can provide invaluable support in evaluating business opportunities, developing business plans, and managing your ventures. Whether you’re interested in starting a restaurant, a retail chain, or a tech startup, having the right guidance can make all the difference.

Tax Planning

High earnings often come with complex tax obligations. A financial advisor can help you navigate these complexities, enabling you to take advantage of tax-saving opportunities and stay compliant with regulations.

Estate Planning

Protecting your wealth for future generations is crucial. Advisors can assist you in creating an estate plan that distributes your assets according to your wishes, minimizing tax liabilities and providing for your loved ones.

Retirement Planning

Even if you’re transitioning into a second career, planning for retirement is essential. Advisors can help you set up retirement accounts, plan for long-term care, and establish a steady income stream throughout your retirement years.

Risk Management

Life is unpredictable, and managing risk is a crucial part of any financial plan. Advisors can help you select the right insurance policies and develop strategies to protect your assets against unforeseen events.

Taking the Next Step in Your Post-Playing Journey

Transitioning from a professional athlete to a successful entrepreneur, broadcaster, coach, or executive is not just a dream; it’s a reality for many who have walked in your shoes. With strategic planning and the right financial support, you can turn your athletic success into lifelong financial stability and growth.

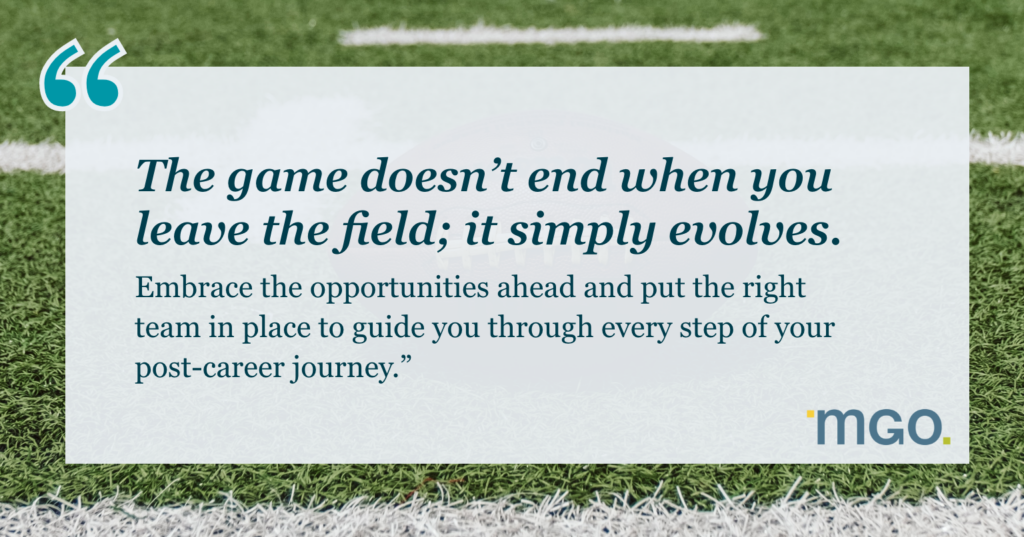

Remember, the game doesn’t end when you leave the field; it simply evolves. Embrace the opportunities ahead and put the right team in place to guide you through every step of your post-career journey.

How We Can Help

Our dedicated Entertainment, Sports, and Media team has extensive experience guiding professional athletes through all phases of their career journeys. We offer comprehensive financial services tailored to help you achieve continued success. Reach out to our team today to discuss how we can support your post-career goals.

Often viewed as a “public company problem,” private organizations may want to consider implementing internal controls similar to Sarbanes-Oxley (SOX) Section 404 requirements. The inherent benefits of a strong control environment may be of significant value to a private company by providing: enhanced accountability throughout the organization, reduced risk of fraud, improved processes and financial reporting, and more effective inclusion of the Board of Directors.

Private organizations, while not always smaller, often have limited resources in specialty areas, including accounting for income tax. This resource constraint —the work being done outside the core accounting team — combined with the complexity of the issues, means private companies are ideal candidates for, and can achieve significant benefit from, internal controls enhancements. Thinking beyond the present, the following are five reasons private companies may want to adopt public-company-level controls:

1. Future Initial Public Offering (IPO) – Walk before you run! If the company believes an IPO may be in its future, it’s better to “practice” before the company is required to be SOX compliant. A phased approach to implementation can drive important changes in company culture as it prepares to become a public organization. Recently published reports analyzing IPO activity reveal that material weaknesses reported by public companies were disproportionately attributable to recent IPO companies. Making a rapid change to SOX compliance can place a heavy burden on a newly public company.

2. Merger and Acquisition Deals – If the possibility of the company being sold to an M&A deal exists, enhanced financial reporting controls can provide the potential buyer with an added layer of security or comfort regarding the financial position of the company. Further, if the acquiring firm has an exit strategy that involves an IPO, the requirement for strong internal controls may be on the horizon.

3. Rapid Growth – Private companies that are growing rapidly, either organically or through acquisition, are susceptible to errors and fraud. The sophistication of these organizations often outpaces the skills and capacity of their support functions, including accounting, finance, and tax. Standard processes with preventive and detective controls can mitigate the risk that comes with rapid growth.

4. Assurance for Private Investors and Banks – Many users other than public shareholders may rely on financial information. The added security and accountability of having controls in place is a benefit to these users, as the enhanced credibility may impact the cost of borrowing for the organization.

5. Peer-Focused Industries – While not all industries are peer-focused, some place significant weight on the leading practices of their peers. Further, some industries require enhanced levels of security and control. For example, cannabis companies with a heavy regulatory burden, industries with sensitive customer data like lifesciences, and tech companies that handle customer data, often look to their peer group for leading practices, including their control environment. When the peer group is a mix of public and private companies, the private company can benefit from keeping pace with the leading practices of their public peers.

Private companies are not immune from the intense scrutiny of numerous stakeholders over accountability and risk. Companies with a clear understanding of the inherent risks that come from negligible accounting practices demonstrate their ability to think beyond the present, and to be better prepared for future growth or change in ownership.

An initial public offering (IPO) of shares to the public is not the end of a journey, but instead the start of a new life for a company. An IPO forever changes the way a company operates and grants access to a deep, consistent pool of capital that serve as a launching pad for achieving lasting, strategic growth.

The trade-off is greater public and regulatory scrutiny, and often, fundamental changes to the way a business operates. We’ve assembled this guide to layout the roadmap for a successful IPO. Utilizing experience gained from years of developing registration statements, auditing and preparing financial statements, and conducting due diligence, we present the core steps and concepts required. The IPO process is complex, resource-intensive, and pocked with pitfalls to the unprepared.

10 Preliminary Implementation Steps That Will Supercharge Your Action Plan

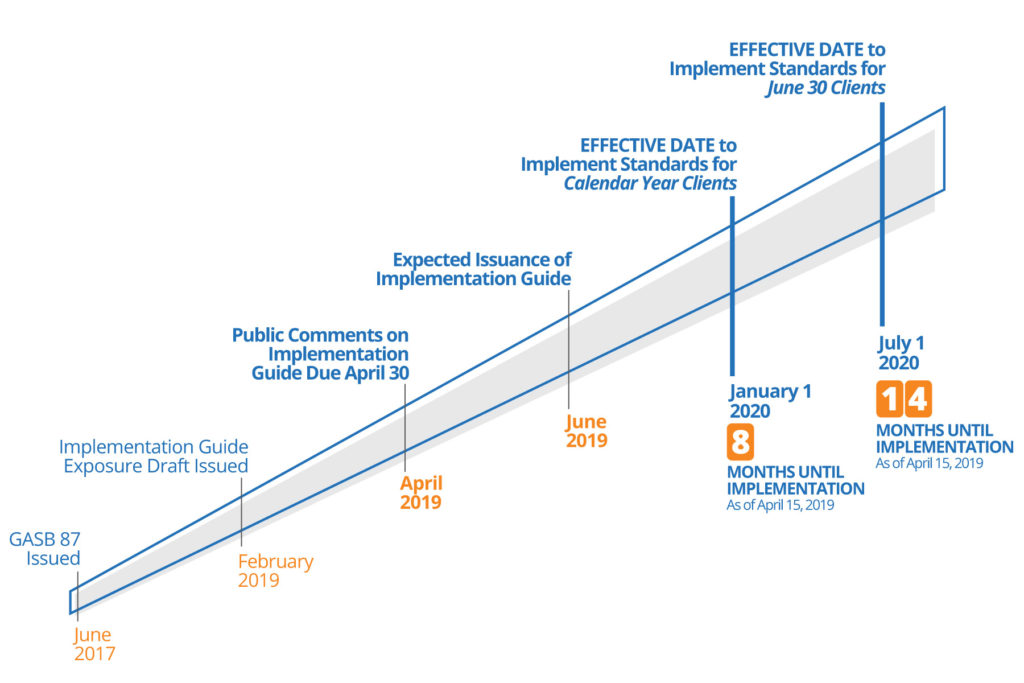

GASB 87 readiness

With an effective date within the next year for some governments (i.e., as soon as January 1, 2020, for governments with a calendar year ending December 31, 2020) – the countdown has begun for planning for the impending changes to accounting and reporting for leases.

Under these new rules, the recording of leases, including assumptions, will significantly impact financial statement amounts and disclosures. Because governments use a variety of leasing arrangements to stabilize cash flows and reduce risk and uncertainty, the new requirements have strong accounting and financial reporting implications requiring a readiness plan. But first, why are these changes occurring?

The backstory on GASB 87

It is important to have some context for the impending changes. The new statement was created because leasing guidance for state and local governments, as we know it, predates GASB’s existence. Because of this fact, the GASB’s conceptual framework was not taken into consideration, which includes definitions of assets, deferred outflows of resources, liabilities, and deferred inflows of resources. The updated guidance for lease accounting has rectified the situation, which is currently underreporting the economics of a lease transaction.

The new lease accounting standards will replace the current operating and capital lease categories with a single model for lease accounting, based on the concept that leases are a means to finance the right to use an asset.

Lease assessment timeline

With the effective date approaching quickly, the time to prepare is NOW!

Taking the lead

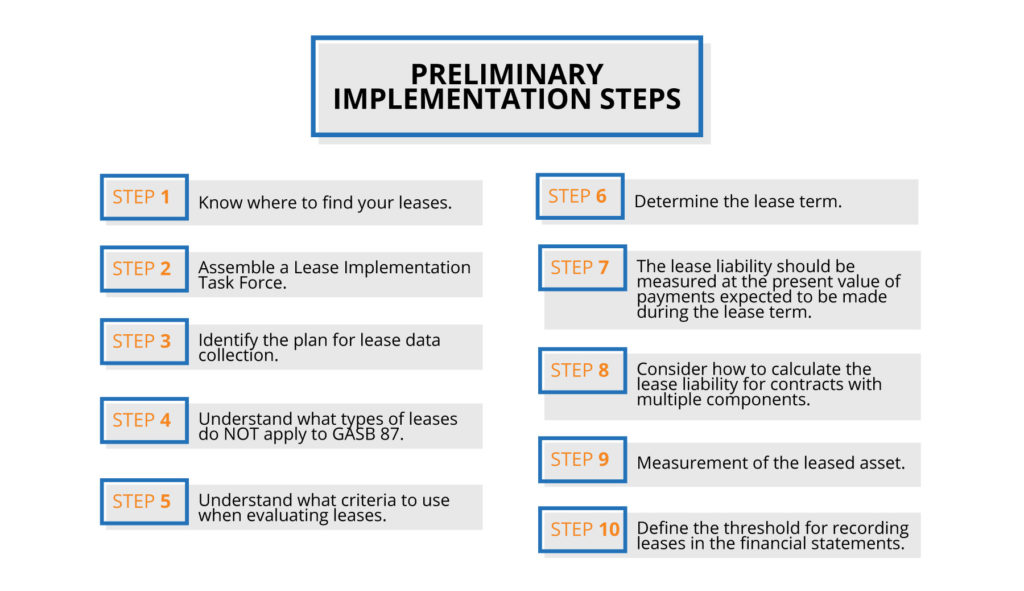

The MGO GASB 87 Implementation Team has created a readiness assessment tool providing 10 preliminary implementation questions for consideration in your planning. These will not only prepare you for the new lease accounting standards, but may uncover matters that were not previously considered or identified.

This 10-step Implementation Plan is more of a general guide designed to assist you in identifying issues and help you organize your implementation process, rather than being an all-inclusive plan with specific technical guidance. As you evaluate the leases that are unique to your organization, you will most likely find that further research and analysis is necessary to ensure proper accounting considerations. For example, if you operate an airport and have aviation leases with air carriers regulated by the U.S. Department of Transportation and the Federal Aviation Administration, it will be necessary to understand how the regulated lease provisions affect your contracts, especially in situations where there are multiple lease components.

Preliminary implementation steps

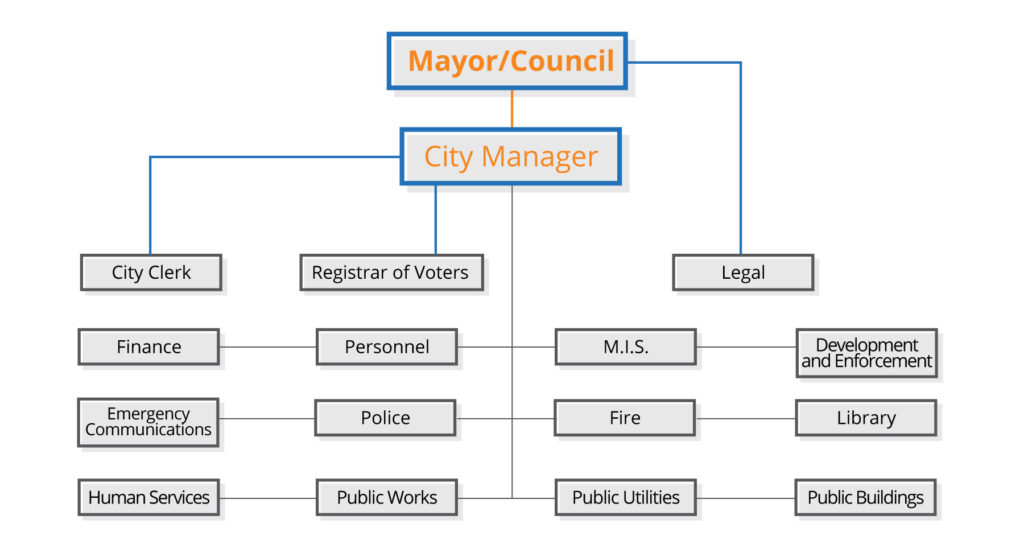

Step 1. Know where to find your leases.

It may seem obvious, but the first step in managing your leases is knowing where they are and, specifically, who is responsible for maintaining them. A good place to begin is with organizational charts. This is an example for a municipal government.

Depending on how your government contracts services, leases may be held centrally within the Finance Department or they may be decentralized in a multitude of departments, and possibly even managed by various entities. Keep in mind that most leases that were previously expensed as operating leases will need to be accounted for as a lease obligation under the new standards, including option years if you are reasonably certain they will be exercised.

After the “where” has been established you can move into the “what” by identifying the universe of leases for your organization. This can be accomplished by evaluating the general ledger, reviewing contract files and surveying purchasing and operating departments, which leads to assembling a task force and formulating a plan for data collection.

Step 2. Assemble a Lease Implementation Task Force.

Identify people who are critical to a successful implementation. Consider including operational and legal staff who are already familiar with existing lease terms and conditions. The Lease Implementation Task Force should remain in place until the action plan for lease implementation is finalized. The benefits are many, including a collective think tank to evaluate and apply appropriate accounting treatment to each class of leases. This task force may also be important to developing internal policies and procedures, such as whether or not a materiality threshold is appropriate, and whether or not lease accounting software should be utilized to manage the lease database. Furthermore, the implementation of the lease accounting standards is only a start, proper accounting treatment, including the remeasurement of the initial lease liability when certain lease changes have occurred and the evaluation of new leases subsequent to implementation, will be an on-going requirement.

Step 3. Identify the plan for lease data collection.

Converting your lease data into an organized structure is not without its challenges. You may encounter incomplete lease files, “hard copy versions only” of certain lease agreements, voluminous amendments, and the need to translate data from lease agreements into databases. This is all part of the process leading to a successful implementation of the new standards. Once you complete the database, you’ll then need to properly classify the leases.

Step 4. Understand what types of leases do NOT apply to GASB 87.

While a multitude of leases will be impacted by the new GASB 87 standards, there are several classifications that are not subject to GASB 87, including: intangible assets (such as computer software licenses); biological assets, including timber, plants and animals; inventories; service concession arrangement contracts; leases in which the underlying asset is financed with outstanding conduit debt; and supply contracts, such as power purchase contracts. Additionally, nonexchange agreements are exempt: for example, in the case of leasing property to a school district for a reduced price of $1/year for 30 years.

In the end, it is all about evaluating the leases subject to GASB 87.

Step 5. Understand what criteria to use when evaluating leases.

After eliminating leases that are not subject to GASB 87, as identified in Step 4, further classification of leases is necessary to ensure that the appropriate accounting treatment is applied. Short-term leases, contracts that transfer ownership, leases of assets that are investments (lessors only), and certain regulated leases (lessors only) all qualify as leases, but have differing accounting treatments than the typical long-term, noncancellable leases.

Step 6. Determine the lease term.

A lease term is defined as the period during which a lessee has a noncancellable right to use an underlying asset, plus any extension periods and options that are reasonably certain to be exercised. The GASB wants organizations to consider extension periods and options, so there is no incentive to structure initial lease terms to avoid meeting the definition of a lease. Since month-to-month leases that continue into a holdover period until a new lease is signed are not part of the noncancellable period or a formal extension, there is no basis in the standard for currently including them. Let’s discuss the calculation of the lease liability.

Step 7. The lease liability should be measured at the present value of payments expected to be made during the lease term.

The lessee should initially measure the lease liability at the present value of payments expected to be made during the lease term, which includes the following elements:

Fixed payments

Variable payments that depend on an index or a rate, initially measured using the index or rate as of the commencement of the lease term

Variable payments that are fixed in substance

Amounts that are reasonably certain of being required to be paid by the lessee under residual value guarantees

The exercise price of a purchase option if it is reasonably certain that a lessee will exercise that option

Payments for penalties for terminating the lease, if the lease term reflects the lessee exercising (1) an option to terminate the lease or (2) a fiscal funding or cancellation clause

Any lease incentives receivable from the lessor

Any other payments that are reasonably certain of being required based on an assessment of all relevant factors

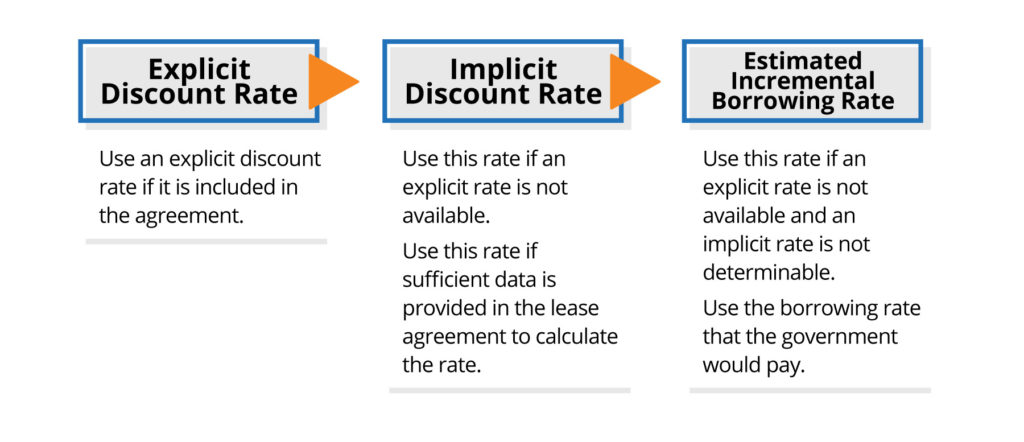

For additional guidance and context to these bulleted items, refer to GASB 87 paragraph 21. In order to determine the present value, you may need to develop the discount rate.

Step 8. Consider how to calculate the lease liability for contracts with multiple components.

Proper classification of leases is not always straightforward when both lease and nonlease components are included in the same contract. What if a building lease has utilities and common area maintenance costs? The answer can be found in guidance covering contracts with multiple components, which identifies maintenance services as a nonlease component. What if a lease involves multiple assets and those assets have different lease terms? The answer can also be found in guidance covering contracts with multiple components, which provides that each asset should be accounted for as a separate lease component. Many rental leases embed the cost of utilities and common area maintenance into the lease payment. Contract components should be separated using the best estimate available based on observable information. If it is not practicable to estimate these separate costs, then account for the contract as a single lease unit (see GASB 87 paragraph 67).

Step 9. Measurement of the leased asset.

The initial measurement of the leased asset should be based on the measurement of the associated lease liability. In the case of contracts with multiple components, the value of the underlying leased asset is not always clearly stated in the agreements, and many lease agreements will not cover the life of the leased asset. Some leased assets may involve proprietary information that lessors are not willing to share. Therefore, determining the value of the underlying asset is not always straightforward in these cases. Whenever possible, identifying comparable assets that are sold in a market transaction is an important part of the process. You can then utilize the knowledge of internal or external experts who can provide a basis for an estimate.

You are now ready for the final step.

Step 10. Define the threshold for recording leases in the financial statements.

Unfortunately, while GASB provides explicit guidance on capitalization thresholds for capital assets, it does not specify any such consideration for lease obligations. Using a threshold may help you avoid recording leases that are immaterial and avoid a mismatch with leased assets that are too small to capitalize. A good starting point may be to use the capitalization thresholds that are already established for your organization. Once you determine your initial criteria for establishing leases, verify that it does not exclude significant leases from application of the new standard. You can revise these thresholds as needed. Now that we have provided you with our 10-step GASB 87 readiness plan, you should have a fairly good idea what your next steps will be.

So you can plan for compliance, this is an excellent time for the MGO GASB 87 Implementation Team to review your leases. This will ensure that you are ready to take the most important step: Implementation. In addition, we have put together an online readiness assessment that helps you evaluate where you stand in the implementation process.

About the Author:

David Bullock is a thought leader in MGO’s State and Local Government practice. An Assurance and Government Advisory Services Partner with 25 years of professional experience, he currently oversees numerous audits and other services to governmental organizations throughout California. In 2018, David was appointed to the AICPA State and Local Government Expert Panel. He is also on the Governmental Accounting Standards Board’s (GASB) Financial Reporting Model Reexamination Task Force. In 2018, he was appointed to the California Society of CPAs’ Governmental Accounting and Auditing Committee. His numerous presentations cover topics related to generally accepted accounting principles promulgated by the GASB, and auditing standards, promulgated by the AICPA and the GAO.

The legal, legislative, and regulatory landscape of cannabis in North America is dynamic and if there has been one constant since pioneering states implemented a legal ‘seed-to-sale’ adult-use market in 2014, it is change. And it is unrelenting.

To help cannabis entrepreneurs and investors keep up with the fast pace of change in the cannabis industry we will be providing monthly summaries of the latest regulatory and legislative news to provide a snapshot of latest happenings while also highlighting matters of interest looking forward.

This month the focus is on prominent federal legislative activity (e.g. the SAFE Act and the STATES Act), state legalization measures (e.g. NJ, NY, IL, and others), and two bills in Colorado that have the potential to attract out-of-state investment to that market.

Changes in federal cannabis legislation

With control of the House of Representatives being transferred to the Democratic party, several bills that have the potential to profoundly impact the cannabis landscape have advanced in Congress. For example, the last week of March saw the House Financial Services Committee move forward the Secure And Fair Enforcement (SAFE) Banking Act to a full House vote, reportedly “within weeks.” Following the momentum of the House bill, U.S. Sens. Jeff Merkley (D-OR) and Cory Gardner (R-CO) have introduced the companion bill in the Senate.

The latest SAFE iteration addresses the cannabis banking crisis and includes amendments that offer protection to insurance companies and other financial services companies.

The banking issue is long-standing and predates even the implementation of recreational cannabis in the US. The lack of straight forward access to fundamental banking services for the cannabis industry creates a multitude of challenges, most notably the operational and financial difficulties of a multi-billion-dollar industry operating almost entirely in cash. This has obvious implications for public safety and potential diversion to the black market, among other concerns.

The inability to access banking services is often identified as a major hindrance to market entry for large and well-resourced corporations and removal of this barrier could herald a seismic shift in investment into the cannabis industry. At time of writing the House Bill had 152 cosponsors, including 12 Republicans, whereas the Senate bill has 20 co-sponsors.

Adding further momentum to the SAFE bill, last week Last week, Secretary Steve Mnuchin offered his support for a legislative fix for the banking issues facing the cannabis industry. “There is not a Treasury solution to this. There is not a regulator solution to this,” he said. “If this is something that Congress wants to look at on a bipartisan basis, I’d encourage you to do this.”

Another potentially substantial piece of legislation is the Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act), which aims to reduce conflict between federal and state laws as they relate to cannabis. The STATES Act is a potential gamechanger for the cannabis industry, allowing legal certainty for companies seeking to operate in dozens of jurisdictions across the US.

Although this legislation stalled in December, it was reintroduced on April 4th, alongside other measures, which include:

the Ending Federal Marijuana Prohibition Act that would effectively legalize marijuana at the federal level by removing it from the Controlled Substances Act.

The Marijuana Justice Act of 2019

The extent to which these bills have bipartisan support may be crucial if they are move beyond the House.

Four steps forward and two steps back in state legalization efforts

It has been a mixed month in terms of advancing cannabis legalization measures at the state level. On the one hand, there has been progress in multiple states, such as Connecticut, Illinois, and New Hampshire. While on the other hand there was a couple of snags holding up the implementation of recreational markets in New Jersey and New York.

The New Jersey cannabis legalization bill was pulled due to lack of support although Gov. Murphey (D) reportedly stated he remained committed to getting the bill passed.

New York dropped cannabis legalization from its budget bill where it was viewed as more likely to pass, however, regulators remain optimistic of progress later in the year. The New York City Council also voted to ban cannabis testing for job applicants.

A General Law Committee in the Connecticut Legislature approved a bill that would legalize an adult-use cannabis market in the state.

A bill to legalize retail cannabis in Illinois was introduced and passed to a subcommittee for further consideration.

Governor of Guam signed a bill legalizing cannabis, becoming the first US territory to do so.

Despite the hiccups outlined above, there is a clear trend towards legal cannabis across the US. Moreover, several states took steps towards expansion or liberalization of their medical cannabis markets. Certainly in the long term, the outlook is optimistic for the cannabis industry on a number of fronts.

Back to the future as Colorado looks to position itself as an investment hub for cannabis

When Colorado became the first state to implement an adult-us cannabis framework in 2014, out of state investment was restricted. This allowed the state to build upon its existing medical cannabis market.

The understandable caution has since been questioned, however, and a Bill offering more flexibility in investment passed both the Colorado House and Senate in 2018, only for then Gov. Hickenlooper to veto it. In 2019, a replacement Bill was introduced and has recently passed its third reading in the House unamended.

As an established market with mature regulations and market stability, Colorado has low-risk potential when compared to emerging markets in other states – although competition is likely to be strong, with ever-thinning margins as prices continue to drop in the state.

Out-of-state investors exploring options in Colorado may be interested in acquiring social consumption licenses in Denver, or seek opportunities for market expansion in the delivery segment of the market. If passed, HB19-1234 would allow licensed dispensaries to offer these services for the first time.