As ESG issues gain prominence, state and local governments must increase oversight, planning, collaboration, and transparency around these topics to maintain public trust and access financing.

Governments should develop, maintain, and regularly update public climate action plans outlining ESG risks, opportunities, impacts, and integration strategies.

Entities should explore green bonds as a growing option to raise ESG-tied funding while increasing related financial disclosures to satisfy investor expectations.

~

Environmental, social, and governance (ESG) issues are taking center stage globally, and U.S. state and local governments — especially those issuing municipal bonds — are facing rising expectations from constituents and investors alike to manage these concerns. To maintain public trust and access to financing, your government should make ESG an increased area of focus, discussion, and disclosure.

Here are a trio of ways your government can bring ESG efforts to the forefront:

1. Prioritize Leadership and Collaboration

The most successful government entities not only have designated ESG leaders (typically the “chief sustainability officer” or “head of environmental affairs”), but they have also established a direct line of oversight and communication with the government entity’s leadership teams (e.g., the mayor’s office, the office of the comptroller, etc.).

While ESG strategy and risk identification will always be owned by the head of the environmental and social functions, collaboration with the finance functions is also vital. Collaboration ensures that financial professionals can contribute their knowledge and experience to assess the financial impact of ESG initiatives and align them with broader strategies of the government.

Collaboratively embedding ESG efforts throughout your entity and not just siloing them to one specific department or group of individuals will give ESG the attention and investment it needs to make an impact.

2. Develop and Maintain a Climate Action Plan

At present, most medium-to-large government entities have formally documented “climate action plans” available on their websites — indicating this type of transparency will be considered “table stakes” moving forward.

Within the climate action plan, a clear strategy to identify and prioritize risks and opportunities is critical. A robust plan should specifically measure both the actual and potential impacts of ESG-related opportunities and risks on the government entity (such as on its financial planning and budgeting) and its stakeholders (e.g., investors and the communities the entity serves). Establishing and publicly communicating these on the entity’s website — or attached in the climate action plan — is key for accountability and understanding of these aspects of sustainability integration.

Additionally, a subset of government entities with climate action plans are also proactively updating their plans — effectively recognizing the plan should be a living and breathing document that continues to evolve with the emergence of new risks and the shifting interest of investors, regulators, and the public at large.

3. Explore the Potential of Green Bonds

Due to the increasing importance of sustainability and ESG for state and local governments, the issuance of green bonds by government entities will also continue to grow. Investors are expecting more financial disclosures to help them make decisions and track both opportunity and risk.

A green bond is a fixed income debt instrument occurring when an issuer (in this case, a state or local government) borrows a large amount of money from investors to use in projects focused solely on sustainability. They are similar in function to traditional bonds, except the funds acquired through them can only be dedicated to projects dedicated to energy efficiency or sustainability requirements and frameworks.

Because investors face risk when it comes to investing in municipal securities (like green bonds), it is crucial for these municipalities to have dedicated ESG leaders, offices, and transparent budgets.

Embracing ESG Principles and Building Positive Public Perception

With intensifying investor and community demands, state and local governments can no longer view ESG as an afterthought. Implementing robust oversight frameworks with designated leadership, continually updated climate action plans, and increased financial disclosures can help you meet expectations, mitigate risks, and contribute to long-term fiscal sustainability.

Need assistance implementing and managing your government’s ESG efforts? Our State and Local Government Practice offers ESG materiality and benchmark assessment, reporting and disclosure, data lineage and integrity, and net zero strategy development and monitoring. Reach out to our team today to learn how we can help you achieve your goals.

Environmental, social, and governance (ESG) information helps investors, regulators, and the public-at-large understand and interpret a government entity’s risk profile and its ability to drive positive impact.

To present this information publicly, government entities are developing robust “Climate Action Plans,” which are reviewed and refreshed on a periodic basis.

As disclosing ESG-related information to the public becomes more common, government entities are also expanding ESG-related disclosures within annual financial reports.

Coined in a 2004 United Nations report, the term “environmental, social, and governance” (and its accompanying acronym “ESG”) is less than 20 years old. Yet, you would be hard-pressed to find a boardroom today where ESG is not top of mind. It is not just businesses either — ESG is also an increasingly important topic of discussion within government organizations.

State and local governments use ESG-related information as a mechanism to measure and track priorities, footprints, and targets. As governments have matured, ESG reporting and presented information more consistently with year-to-year comparability, investors*, regulators, and the public-at-large have sought out this reporting to help them understand risk and the government entity’s ability to drive positive impact.

*Note: The term “investors” refers to those who are exploring and/or holding investments in government-issued securities (e.g., hedge funds, institutions, individuals, etc.).

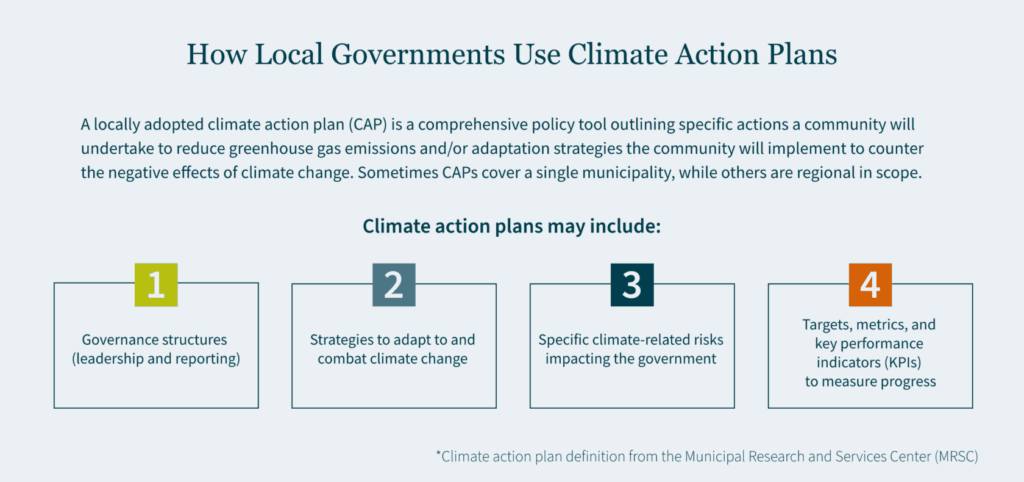

The Increasing Importance of “Climate Action Plans”

To present ESG-related information to the public, many government entities develop and communicate robust “Climate Action Plans”. These plans highlight a myriad of information, including (but not limited to):

Governance structures (e.g., communication and reporting lines from environmental leadership into the mayor’s office)

Strategies to adapt to and combat climate change

Specific climate-related risks, which impact the government entity

Targets, metrics, and key performance indicators (KPIs) used to measure progress

As Climate Action Plans continue to evolve, governments are commanding and allocating more financial resources to activate these plans. With the increased focus on climate-related initiatives presented in Climate Action Plans, we are seeing an expansion of ESG-related information disclosed within “Annual Comprehensive Financial Reports” across the country — a sign that financial disclosures are maturing to meet growing interests from investors, regulators, and the public-at-large.

A Growing Push from Investors and Regulators

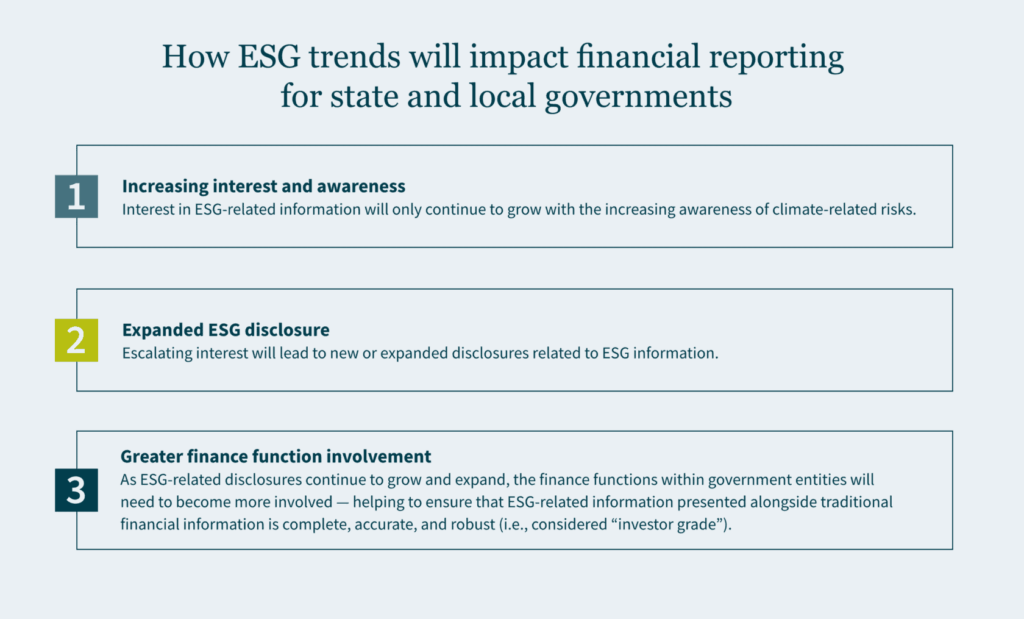

The focus on non-financial risks (including, but not limited to, ESG-related risks) by investors and regulators continues to intensify. When we take a step back to analyze the trend, a few things become clear:

Interest in ESG-related information will only continue to grow with the increasing awareness of climate-related risks.

Escalating interest will lead to new or expanded disclosures related to ESG information.

As ESG-related disclosures continue to grow and expand, the finance functions within government entities will need to become more involved — helping to ensure that ESG-related information presented alongside traditional financial information is complete, accurate, and robust (i.e., considered “investor grade”).

To dive deeper into that last point, where would a finance function start? The short answer is by increasing the integration and collaboration between a government entity’s environmental leaders and the finance functions. The longer answer is that government entities need to develop holistic approaches to collecting and reporting robust ESG-related information to meet the expectations of investors, regulators, and the public-at-large.

The bottom line: As the issuance of and investment in municipal securities continues to grow, the quality of ESG-related information disclosed to the public will need to be enhanced to meet the demands of investors.

Transparency in Budgets and Financial Reporting

With an increase in ESG-related disclosures in annual financial reports by government entities, recent interpretive guidance from the Governmental Accounting Standards Board (GASB) indicates that government entities can expect further scrutiny and regulation as these types of disclosures become more commonplace.

Essentially, it is important for your government to have a robust, well-communicated ESG “story” within a Climate Action Plan — but you also must provide investor-grade transparency within audited financial statements. Government entities are already beginning to meet this challenge. Two examples of local governments with a growing presence of ESG-related information in their Annual Comprehensive Financial Reports are the City and County of San Francisco and the City of Fremont.

The City and County of San Francisco transparently discloses both environmental and social initiatives, capturing details related to its Environmental Protection Fund, as well as specific details related to revenues received from state, federal, and other sources for the preservation of the environment.

The City of Fremont — which is much smaller in terms of population (~230,000) and financial resources (roughly $1.5 billion in total primary government assets from “government activities”) — depicts ESG-related information throughout its annual report, including but not limited to qualitative information in the “management discussion and analysis” section, as well as quantitative information related to “community development and environmental services.”

The Path Forward: Enhancing Your ESG Reporting

With ESG-related information becoming more integrated into investor decision-making, your government needs to focus on enhancing its Climate Action Plans and developing “investor grade” disclosures related to ESG risks and opportunities for inclusion within your traditional financial reporting. These initiatives will require additional financial resources and human capital to create and maintain — and further collaboration between environmental, social, and financial leaders will be needed to drive the change.

How MGO Can Help

Incorporating ESG disclosures into financial reporting can pose challenges to states and local governments unfamiliar with ESG reporting standards. With experience providing ESG solutions, our State and Local Government Practice will work with your team to meet requirements and make information “investor-ready,” while also ensuring accountability and transparency.

As of January 1, 2022, New York employers must report new hires who are listed as independent contractors and have contracts worth more than $2,500 to the New York State Department of Taxation and Finance.

Previously, you were not mandated to include independent contractors under the state’s new hire reporting requirement; now you’ll have to add them to the list of other new hires or rehires to report.

If your organization falls into one of the following categories, you’re required to report your new hires for tax purposes:

Labor organizations, including union-operated placement offices (I.e., hiring halls),

Employers of individuals performing domestic services,

Government entities excluding federal agencies.

Your organization will have to report those new hires or rehires, including independent contractors, within 20 calendar days from the date hired. The hiring date is defined as the first day the employee or contractor:

Is eligible to collect commissions for any job performed based only on commissions,

Completes the services for which they will be paid (collecting tips, wages, commissions, or another agreed-upon compensation).

If you are an employer looking for clarification regarding additional reporting requirements in New York State (including how to actually file), please contact MGO’s tax team to talk to an advisor who can comprehensively walk you through the steps and ensure you avoid any missteps that could affect your organization.

Alternative Engagement Types: Consulting Services, Agreed-Upon Procedures, and Performance Audits

By Scott P. Johnson, CPA, CGMA Partner, Macias Gini & O’Connell LLP State and Local Government Advisory Services

I have spent most of my professional career over the past 35 years serving government agencies and focusing on performance improvement, accountability, and transparency. I recognize the need for continuous monitoring and oversight in the public sector to ensure performance, public accountability, and stewardship of public resources. While participating on a number of professional panels and presentations throughout my career, I have often stated that I embraced the auditor and have welcomed them with open arms into the organizations that I had responsibility over. Why? Because I see auditors as an independent and objective lens, adding value to review and evaluate performance and to make recommendations for improvement. The organizations I have had the pleasure to work for took public accountability very seriously and supported performance improvement as a means to better serve their communities and stakeholders.

Much like a traditional CPA firm can provide different types of services related to an entity’s financial statements, i.e., audit, review, or compilation, based on need, when government agencies are considering an independent evaluation of performance of their programs or operations, the CPA firm’s advisory or consulting arm can step in and offer a number of engagement types based on the agency’s unique needs: consulting services engagements, attestation engagements (e.g., agreed-upon procedures), and performance audits. It all depends on if, and at what level, assurance is needed. The primary driver of what type of product should be considered is typically based on, for instance, issue complexity, taxpayer concerns or expectations, statute requirements, or increased need for transparency on the efficiency and effectiveness of operations. While the driver of the engagement may differ, time constraints and budget are also determining factors.

This is the first article in a three-part series focusing on performance audits. The primary focus of this article is to discuss the differences of the three aforementioned types of engagements – consulting services, agreed-upon procedures, and performance audits – and to provide guidance when a performance audit might be an option.

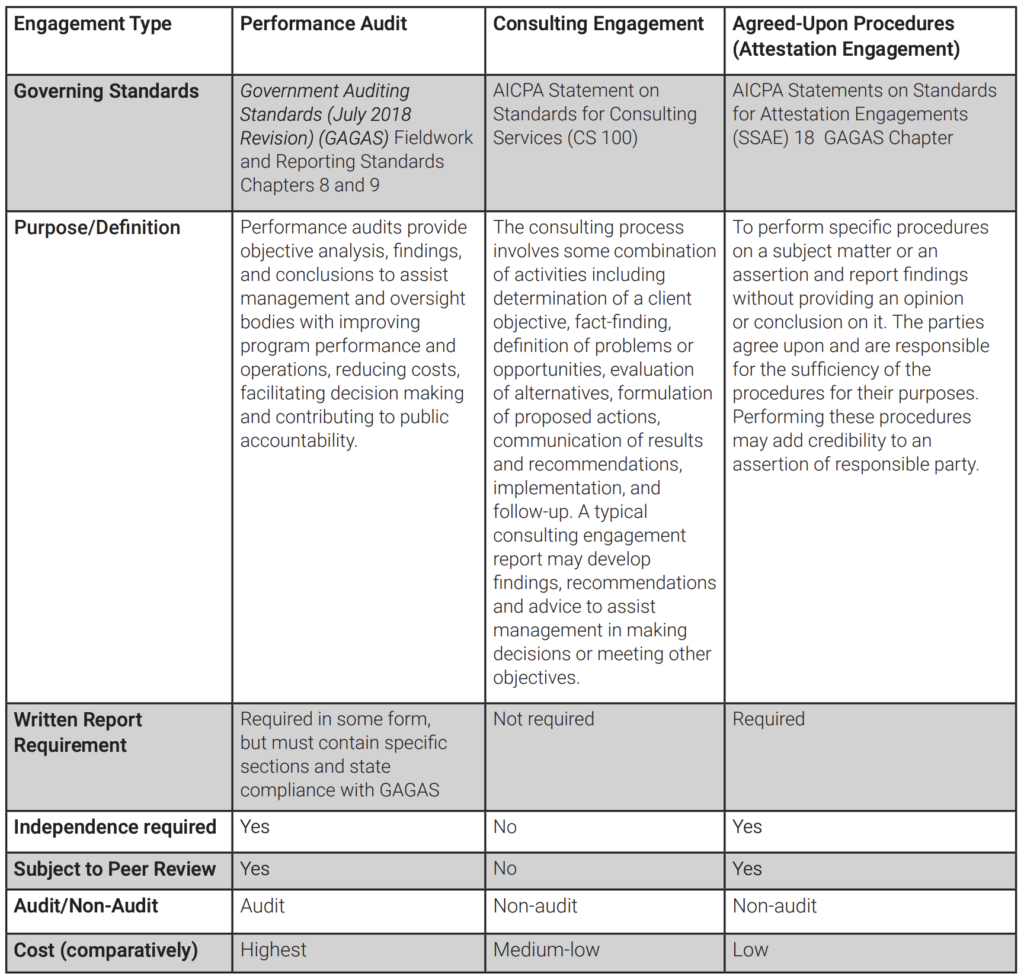

It is important to identify the differences between (1) performance audits, (2) consulting services engagements, and (3) agreed-upon procedures attestation engagements. On numerous occasions throughout my government service career and also while serving clients, questions have come up regarding the objectives sought, the scope of the engagement, and the engagement type when considering an evaluation of performance for a particular program or area of operations. Each of these engagements differ in purpose and reporting requirements, as well as potential cost, as shown below in Figure 1.0. These engagements are governed by different standards, formal reports are not always required for each, and independence is not always required (i.e., consulting services).

Performance Audits Defined

Performance audits are defined as engagements that provide objective analysis, findings, and conclusions to assist management and those charged with governance and oversight to, among other things, improve program performance and operations, reduce costs, facilitate decision making by parties with responsibility to oversee or initiate corrective action, and contribute to public accountability. *1

Furthermore, GAGAS states that management and officials of government programs are responsible for providing reliable, useful, and timely information for transparency and accountability of these programs and their operations. Legislators, oversight bodies, those charged with governance, and the public need to know whether (1) management and officials manage government resources and use their authority properly and in compliance with laws and regulations; (2) government programs are achieving their objectives and desired outcomes; and (3) government services are provided effectively, efficiently, economically, ethically, and equitably. *2

Agreed-Upon Procedures (AUP)

Based on my experience, it usually comes down to identifying a few factors that determine the engagement. First, the agency must determine the purpose and scope of the work, specifically what questions they would like to have answered. These questions can be broad or very narrow. For example, in an AUP, management may make an assertion about whether a subject matter is in accordance with, or based on, established criteria that is the responsibility of a third party and hires a CPA to add credibility to that assertion by performing specific procedures to test compliance with the criteria. If an agency needs to know something very specific and wants an independent party to perform specific procedures and tell them what was found, then an AUP is appropriate. However, an AUP report does not provide recommendations, an opinion, or conclusion about whether the subject matter is in accordance with, or based on, the criteria, or state whether the assertion is fairly stated. While the agency may want to use an AUP, some key steps that are taken in consulting engagements and performance auditing, such as planning, are not required in an AUP engagement. Also, risk is not assessed in developing the scope, nor does the auditor use a risk-based approach, which is required in a performance audit. Finally, in an AUP, auditors do not perform sufficient work to be able to develop elements of a finding or provide recommendations.

1 See Paragraph 1.21 of GAGAS. 2 See Paragraph 1.02 of GAGAS.

Consulting Services Engagement vs. Performance Audit

For a consulting services engagement or performance audit, the initial questions are then turned into the objectives of the engagement. If the agency wants an objective review of operations or a program to assist them in making decisions, for example, to assess the management of specific funds, and wants findings and recommendations to improve operations, then the agency should discuss the options of a consulting services engagement or a performance audit. From here, the decisions are truncated. The agency needs to consider whether the report is for an internal audience, such as governing officials, management, or staff, or an external audience, e.g., a regulatory agency or the public. If the communication is intended for internal use, then a consulting services engagement with observations and recommendations may suffice. For these engagements, findings, recommendations, and a conclusion is provided to assist management in decision making. Or, an independent third party, such as a CPA or an internal auditor, may be asked to answer the engagement’s objectives to an external audience, in which case a performance audit may be more appropriate due to the need for an independent, objective report that can withstand scrutiny and is subject to peer review. Sometimes there isn’t a choice; some agencies are bound by the government code or local ordinance to conduct audits under GAGAS.

Performance audits are typically the more costly engagement type of the three, given the amount of work required to conduct an audit and adhere to stringent standards. As we’ll explore in later articles, performance audits conducted under GAGAS provide the highest level of assurance among the three options, based on the level of work required. These audits involve developing the required elements of a finding and the documentary evidence required for planning, fieldwork, and reporting. The amount of work involved is much greater than in consulting services engagements, where observations and recommendations will suffice. Consulting services engagements are not audits and, therefore, offer no assurance. Similarly, in attestation engagements, where only specific procedures are performed, no assurance is provided. *3

Conclusion

Having been on both sides of deciding what engagement to recommend, either for an agency I worked at or to a client, it’s important to discuss the level of work required for each engagement type, the number of hours required to do the work under the appropriate standard within a reasonable time period, and the available budget. Finally, and most importantly, clients should understand that performance audits and consulting services engagements each have their place and serve unique purposes. A performance audit offers independence and objectivity at a step above a consulting services engagement, and might be the best option if a rigorous audit of a program or agency is needed. This is where the consideration of the agency’s need is paramount. There may not always be the budget or time available to conduct a comprehensive performance audit, nor a need for an in-depth evaluation or a legislative requirement to do so. In these instances, a consulting services engagement is a good option, especially when time and budget are factors. A consulting services engagement can provide a sufficient report with recommendations and advice. However, it’s important to make the agency aware of the limitations of non-audit services. In addition, the audience of the final report product and any regulatory requirements should strongly influence the decision-making process.

Forthcoming articles in this series will drill down and focus in more detail on the professional standards associated with performance audits as compared to other types of engagements, “why” an agency would want a performance audit instead of a consulting engagement or an agreed-upon procedures engagement, when a performance audit would be recommended, what key factors should be considered, and what are the expectations of the audience of the report. The third article in this series will focus on the reporting elements of a performance audit and a sample performance audit report.

*3 Attestation engagement standards are covered in GAGAS Chapter 7, and include agreed-upon-procedures, reviews, and examination engagements. Attestation examinations have the highest level of assurance, as an opinion is given; not so for the others. Auditors may use GAGAS in conjunction with other professional standards such as American Institute of Certified Public Accountants (AICPA), International Auditing and Assurance Standards Board (IAASB), or Public Company Accounting Oversight Board (PCAOB) standards. For financial audits and attestation engagements, GAGAS incorporates by reference for AICPA Statements on Auditing Standards and Statements on Standards for Attestation Engagements. In addition, the AICPA promulgates the consulting standards. AICPA standard committees have taken the position that only the U.S. Government Accountability Office (GAO) sets performance audit standards.

SOURCES OF INFORMATION AND DOCUMENTATION CONSIDERED

Government Auditing Standards, issued by the Comptroller General of the United States – July 2018 Revision (effective for performance audits beginning on or after July 1, 2019; effective for attestation engagements for periods ending on or after June 30, 2020; early implementation is not permitted)

United States General Accounting Office. Best Practices Methodology – A New Approach for Improving Government Operations. May 1995

About the Author

Scott Johnson has 35 years of experience in government administration, with a focus on successfully overseeing internal service operations including; debt management, information technology, human resources, municipal finance, and budget. He has led large and mid-sized operations for California government agencies including the cities of Santa Clara, Milpitas, San Jose, Oakland, and Concord and the County of Santa Clara. Scott is a past president of the California Society of Municipal Finance Officers (CSMFO) and a member of the AICPA Government Performance and Accountability Committee (GPAC). He is currently a partner with Macias Gini & O’Connell LLP (MGO), leading the Advisory Services sector specializing in State and Local Governments, based out of California. He welcomes any questions or comments via email: [email protected].

Greta MacDonald, MPA – Special recognition is given to Ms. MacDonald for her contributions and research for this article. Ms. MacDonald is a Director with MGO in the State and Local Government Advisory Services division. She has over 17 years of experience conducting over 35 performance audits in accordance with GAGAS, which is her specialization area.

Disclaimer: The views expressed in this article are those of the author and do not reflect the official policy or position of the GAO, AICPA, or Macias Gini & O’Connell LLP.