Tax Partner Michael Silvio shares how MGO helped a client save upwards of $1.6M in taxes, along with an additional $2.2M in depreciable assets. By conducting a thorough cost segregation study and reducing the property’s land value from 40% to 15%, the MGO team went beyond the standard approach, assessing the land vs. building value and using insights from the county assessor. Michael explains how MGO’s attention to detail sets them apart from other firms in delivering substantial tax savings.

‘We took the time to really assess the need and then also go a little further and not just do the cost segregation study, but look at the land versus building value, go out to the county assessor website, see what the value is and see if there are any ways we could reduce it. And that’s where I think we add more value than other companies that do cost segregation studies.’

The $1.5 trillion new tax law represents the most sweeping change to tax code in a generation. Tax reform of this magnitude will have broad implications for government contractors. While accountants and tax departments wade through the 185-page legislation, here are the top 10 things government contractors need to know:

1. The corporate tax rate was permanently reduced from 35 percent to 21 percent.

The top corporate tax rate has been permanently reduced from 35 percent to a flat rate of 21 percent, beginning in 2018. Unlike all other provisions in the new law, including tax breaks for individuals, the new corporate tax rate provision does not expire.

2. There’s a tax break for owners of pass-through entities.

The new law provides owners of pass-through businesses — which include individuals, estates, and trusts — with a deduction of up to 20 percent of their domestic qualified business income, whether it is attributable to income earned through an S corporation, partnership, sole proprietorship, or disregarded entity. Without the new deduction, taxpayers would pay 2018 taxes on their share of qualified earnings at rates up to 37 percent. With the new 20 percent deduction, the tax rate on such income could be as low as 29.6 percent. It should again be noted that certain service industries are excluded from the preferential rate, unless taxable income is below $207,500 (for single filers) and $415,000 (for joint filers), under which the benefit of the deduction is phased out.

3. There might be huge tax benefits to changing your company’s current choice of entity.

Taxpayers should consider evaluating the choice of entity used to operate their businesses. The 21 percent reduced corporate tax rate may increase the popularity of corporations. However, factors such as the new 20 percent deduction for pass-through income, expected use of after-tax cash earnings, and potential exit values will significantly complicate these analyses. The potential after-tax cash benefits ultimately realized by owners could make choice-of-entity determinations one of the most important decisions taxpayers will now make.

4. There have been significant changes to the international tax system.

In connection with these changes, some U.S. shareholders who own stock in certain foreign corporations will have to pay a one-time “transition tax” on their share of accumulated overseas earnings. Other changes include a “participation exemption,” which is a 100 percent dividend-received deduction that permits certain domestic C corporations to receive dividends from their foreign subsidiaries without being taxed on such dividends when certain conditions are satisfied. There is also a new requirement that certain U.S. shareholders of controlled foreign corporations (CFCs) include in income their share of the “global intangible low-taxed income” of such CFCs. Finally, there are new measures to deter base erosion and promote U.S. production.

5. The corporate AMT and DPAD are dead, but Research Tax Credits live on.

The law repeals the Section 199 Domestic Production Activities Deduction (DPAD) and the corporate Alternative Minimum Tax (AMT) for tax years beginning after 2017. The Research Tax Credit was retained and is now more valuable given the reduction of the corporate tax rate from 35 percent to 21 percent.

6. They’ve scrapped NOL carrybacks and limited the use of carryforwards.

Previously, businesses were able to offset current taxable income by claiming net operating losses (NOLs), generally eligible for a two-year carryback and 20-year carryforward. Now NOLs for tax years ending after 2017 cannot be carried back, but can be indefinitely carried forward. In addition, NOLs for tax years beginning in 2018 will be subject to an 80 percent limitation. Companies will have to track their NOLs in different buckets and consider cost-recovery strategy on depreciable assets in applying the 80 percent limitation.

7. Tax reform’s impact on accounting methods may change when revenue is recognized, but new provisions could also lead to temporary and permanent tax benefits.

Under the new law, accrual basis taxpayers must now recognize income no later than the taxable year in which such income is taken into account as revenue in an applicable financial statement.

However, new provisions also provide favorable methods of accounting that were not previously available. That, coupled with the reduction in tax rates, creates a favorable and unique environment for filing accounting method changes.

There are many method changes still available for the 2017 tax year. Taxpayers should evaluate current accounting methods to identify any actionable opportunities to accelerate deductions and defer income for the 2017 tax year, which could result in significant tax savings.

8. There are new rules for bonus depreciation and full expensing on new and used property.

The new tax law allows a 100 percent first-year deduction — up from 50 percent — for the adjusted basis of qualifying assets placed in service after Sept. 27, 2017, and before Jan. 1, 2023, with a gradual phase down in subsequent years before sunsetting after 2026. The definition of qualifying property was also expanded to include used property purchased in an arm’s-length transaction. Businesses should pay close attention to any qualifying asset acquisitions made during the fourth quarter of 2017, as the full expensing can be taken on the 2017 return if the property was acquired and placed in service after Sept. 27, 2017.

Additionally, under new tax law, taxpayers may now deduct up to $1 million under Section 179 for properties placed in service beginning in 2018 — double the previous allowable amount. The phase-out threshold is increased to $2.5 million and will be indexed for inflation in future years and the types of qualifying property has been expanded.

9. The availability of the cash method of accounting expanded for small businesses.

Beginning in 2018, the average annual gross receipts threshold for businesses to use the cash method increases from $5 million to $25 million. Additionally, small businesses who meet the $25 million gross receipts threshold are not required to account for inventories and are exempt from the uniform capitalization rules. The $25 million is indexed for inflation for tax years beginning after 2018.

10. Now is the time to assess total rewards strategies.

Tax reform significantly impacts various components of an employer’s total compensation program — namely the expansion of the $1 million deduction cap on pay to covered employees; disallowed deductions for transportation fringe benefits provided to employees; income inclusion for employer-paid moving expenses; further deduction limitations on certain meal and entertainment expenses; and a two-year tax credit for employer-paid family and medical leave programs. As the IRS releases guidance, employers must immediately modify their payroll systems to reflect tax reform changes impacting individual taxpayers.

For more information about the impact of tax reform on the Government Contracting industry, please reach out to us.

Is your organization getting the most from your procurement department? Public sector procurement has more demands to meet than other sectors – deliver products/projects on budget, to specifications, adhering to government policies and regulations, while delivering quality products/performance that will benefit its citizens. Purchasing is no longer considered a clerical function. Today, purchasing agents are subject to emerging technologies, increasing product diversity and choice, environmental concerns, and a new emphasis on quality and best value, not just lowest price. The top ten issues in the procure to pay cycle are:

Insufficient outreach to vendors

Lowering of bonding requirements

Burdensome administrative requirements

Insufficient segregation of procurement approval and receiving duties

Lack of cross-department evaluation of vendor proposals

Inconsistent management and designated authority levels

Organizations are unaware of procurement process times – from start of requisition until vendors are paid

Procurement activities are not aligned with overall organizational activities

Too many sign offs/approvals

If any of these issues sound familiar, or your organization has not reviewed its procurement function in a while, you run the risk that your procurement strategies are inconsistent with organizational needs, which can result in paying higher prices for the goods and services required to run your agency, insufficient number of competitive bids, or worse, violating your grant or service agreements.

IntelliBridge Partners has the expertise to improve the procure to pay cycle through business process reviews, risk assessments, and performance audits. If you would like help with your procurement department, please contact Greg Matayoshi at [email protected].

10 Preliminary Implementation Steps That Will Supercharge Your Action Plan

GASB 87 readiness

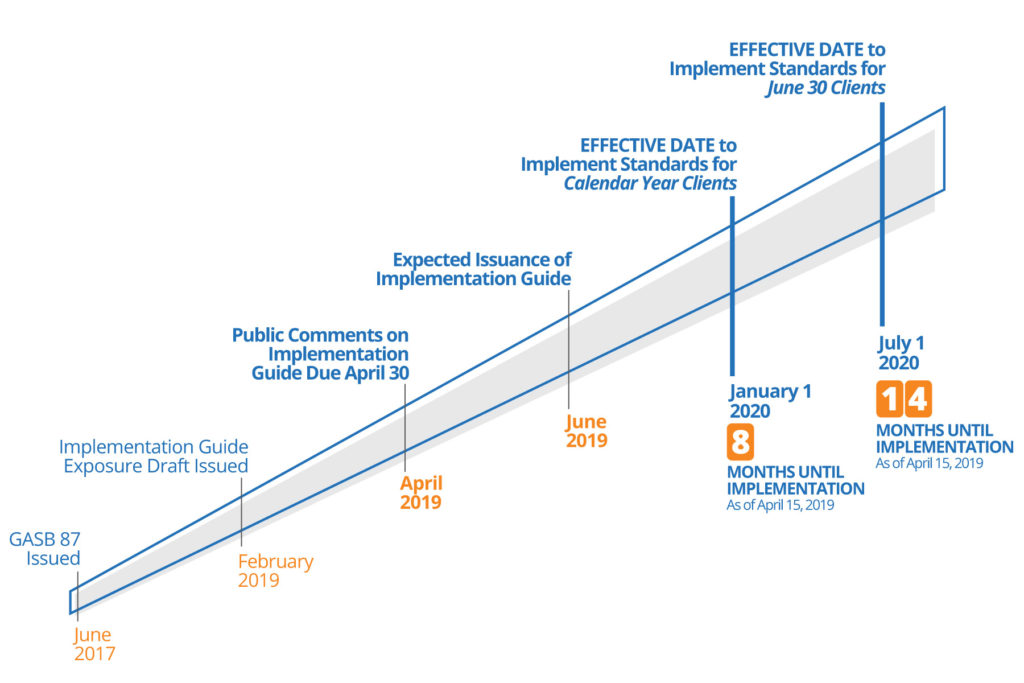

With an effective date within the next year for some governments (i.e., as soon as January 1, 2020, for governments with a calendar year ending December 31, 2020) – the countdown has begun for planning for the impending changes to accounting and reporting for leases.

Under these new rules, the recording of leases, including assumptions, will significantly impact financial statement amounts and disclosures. Because governments use a variety of leasing arrangements to stabilize cash flows and reduce risk and uncertainty, the new requirements have strong accounting and financial reporting implications requiring a readiness plan. But first, why are these changes occurring?

The backstory on GASB 87

It is important to have some context for the impending changes. The new statement was created because leasing guidance for state and local governments, as we know it, predates GASB’s existence. Because of this fact, the GASB’s conceptual framework was not taken into consideration, which includes definitions of assets, deferred outflows of resources, liabilities, and deferred inflows of resources. The updated guidance for lease accounting has rectified the situation, which is currently underreporting the economics of a lease transaction.

The new lease accounting standards will replace the current operating and capital lease categories with a single model for lease accounting, based on the concept that leases are a means to finance the right to use an asset.

Lease assessment timeline

With the effective date approaching quickly, the time to prepare is NOW!

Taking the lead

The MGO GASB 87 Implementation Team has created a readiness assessment tool providing 10 preliminary implementation questions for consideration in your planning. These will not only prepare you for the new lease accounting standards, but may uncover matters that were not previously considered or identified.

This 10-step Implementation Plan is more of a general guide designed to assist you in identifying issues and help you organize your implementation process, rather than being an all-inclusive plan with specific technical guidance. As you evaluate the leases that are unique to your organization, you will most likely find that further research and analysis is necessary to ensure proper accounting considerations. For example, if you operate an airport and have aviation leases with air carriers regulated by the U.S. Department of Transportation and the Federal Aviation Administration, it will be necessary to understand how the regulated lease provisions affect your contracts, especially in situations where there are multiple lease components.

Preliminary implementation steps

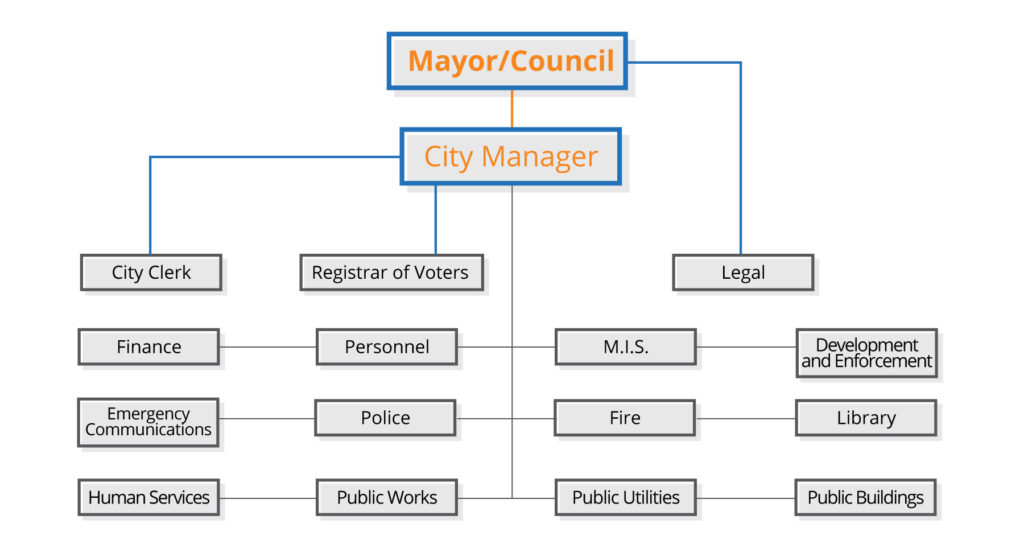

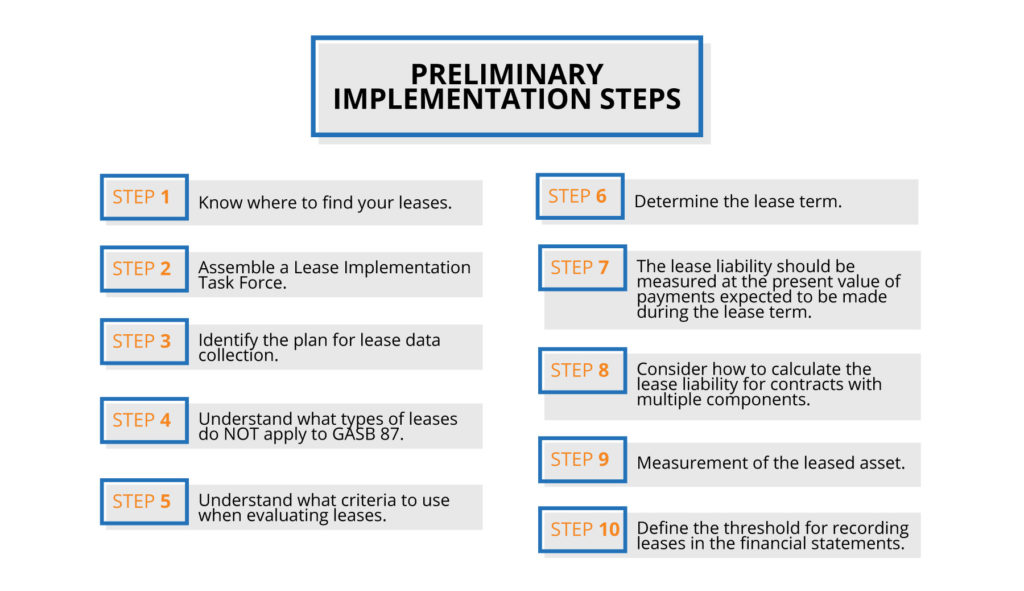

Step 1. Know where to find your leases.

It may seem obvious, but the first step in managing your leases is knowing where they are and, specifically, who is responsible for maintaining them. A good place to begin is with organizational charts. This is an example for a municipal government.

Depending on how your government contracts services, leases may be held centrally within the Finance Department or they may be decentralized in a multitude of departments, and possibly even managed by various entities. Keep in mind that most leases that were previously expensed as operating leases will need to be accounted for as a lease obligation under the new standards, including option years if you are reasonably certain they will be exercised.

After the “where” has been established you can move into the “what” by identifying the universe of leases for your organization. This can be accomplished by evaluating the general ledger, reviewing contract files and surveying purchasing and operating departments, which leads to assembling a task force and formulating a plan for data collection.

Step 2. Assemble a Lease Implementation Task Force.

Identify people who are critical to a successful implementation. Consider including operational and legal staff who are already familiar with existing lease terms and conditions. The Lease Implementation Task Force should remain in place until the action plan for lease implementation is finalized. The benefits are many, including a collective think tank to evaluate and apply appropriate accounting treatment to each class of leases. This task force may also be important to developing internal policies and procedures, such as whether or not a materiality threshold is appropriate, and whether or not lease accounting software should be utilized to manage the lease database. Furthermore, the implementation of the lease accounting standards is only a start, proper accounting treatment, including the remeasurement of the initial lease liability when certain lease changes have occurred and the evaluation of new leases subsequent to implementation, will be an on-going requirement.

Step 3. Identify the plan for lease data collection.

Converting your lease data into an organized structure is not without its challenges. You may encounter incomplete lease files, “hard copy versions only” of certain lease agreements, voluminous amendments, and the need to translate data from lease agreements into databases. This is all part of the process leading to a successful implementation of the new standards. Once you complete the database, you’ll then need to properly classify the leases.

Step 4. Understand what types of leases do NOT apply to GASB 87.

While a multitude of leases will be impacted by the new GASB 87 standards, there are several classifications that are not subject to GASB 87, including: intangible assets (such as computer software licenses); biological assets, including timber, plants and animals; inventories; service concession arrangement contracts; leases in which the underlying asset is financed with outstanding conduit debt; and supply contracts, such as power purchase contracts. Additionally, nonexchange agreements are exempt: for example, in the case of leasing property to a school district for a reduced price of $1/year for 30 years.

In the end, it is all about evaluating the leases subject to GASB 87.

Step 5. Understand what criteria to use when evaluating leases.

After eliminating leases that are not subject to GASB 87, as identified in Step 4, further classification of leases is necessary to ensure that the appropriate accounting treatment is applied. Short-term leases, contracts that transfer ownership, leases of assets that are investments (lessors only), and certain regulated leases (lessors only) all qualify as leases, but have differing accounting treatments than the typical long-term, noncancellable leases.

Step 6. Determine the lease term.

A lease term is defined as the period during which a lessee has a noncancellable right to use an underlying asset, plus any extension periods and options that are reasonably certain to be exercised. The GASB wants organizations to consider extension periods and options, so there is no incentive to structure initial lease terms to avoid meeting the definition of a lease. Since month-to-month leases that continue into a holdover period until a new lease is signed are not part of the noncancellable period or a formal extension, there is no basis in the standard for currently including them. Let’s discuss the calculation of the lease liability.

Step 7. The lease liability should be measured at the present value of payments expected to be made during the lease term.

The lessee should initially measure the lease liability at the present value of payments expected to be made during the lease term, which includes the following elements:

Fixed payments

Variable payments that depend on an index or a rate, initially measured using the index or rate as of the commencement of the lease term

Variable payments that are fixed in substance

Amounts that are reasonably certain of being required to be paid by the lessee under residual value guarantees

The exercise price of a purchase option if it is reasonably certain that a lessee will exercise that option

Payments for penalties for terminating the lease, if the lease term reflects the lessee exercising (1) an option to terminate the lease or (2) a fiscal funding or cancellation clause

Any lease incentives receivable from the lessor

Any other payments that are reasonably certain of being required based on an assessment of all relevant factors

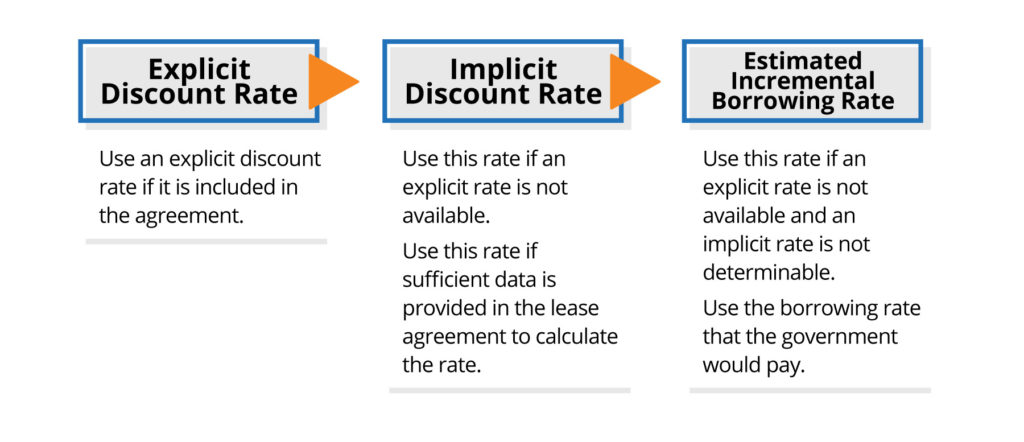

For additional guidance and context to these bulleted items, refer to GASB 87 paragraph 21. In order to determine the present value, you may need to develop the discount rate.

Step 8. Consider how to calculate the lease liability for contracts with multiple components.

Proper classification of leases is not always straightforward when both lease and nonlease components are included in the same contract. What if a building lease has utilities and common area maintenance costs? The answer can be found in guidance covering contracts with multiple components, which identifies maintenance services as a nonlease component. What if a lease involves multiple assets and those assets have different lease terms? The answer can also be found in guidance covering contracts with multiple components, which provides that each asset should be accounted for as a separate lease component. Many rental leases embed the cost of utilities and common area maintenance into the lease payment. Contract components should be separated using the best estimate available based on observable information. If it is not practicable to estimate these separate costs, then account for the contract as a single lease unit (see GASB 87 paragraph 67).

Step 9. Measurement of the leased asset.

The initial measurement of the leased asset should be based on the measurement of the associated lease liability. In the case of contracts with multiple components, the value of the underlying leased asset is not always clearly stated in the agreements, and many lease agreements will not cover the life of the leased asset. Some leased assets may involve proprietary information that lessors are not willing to share. Therefore, determining the value of the underlying asset is not always straightforward in these cases. Whenever possible, identifying comparable assets that are sold in a market transaction is an important part of the process. You can then utilize the knowledge of internal or external experts who can provide a basis for an estimate.

You are now ready for the final step.

Step 10. Define the threshold for recording leases in the financial statements.

Unfortunately, while GASB provides explicit guidance on capitalization thresholds for capital assets, it does not specify any such consideration for lease obligations. Using a threshold may help you avoid recording leases that are immaterial and avoid a mismatch with leased assets that are too small to capitalize. A good starting point may be to use the capitalization thresholds that are already established for your organization. Once you determine your initial criteria for establishing leases, verify that it does not exclude significant leases from application of the new standard. You can revise these thresholds as needed. Now that we have provided you with our 10-step GASB 87 readiness plan, you should have a fairly good idea what your next steps will be.

So you can plan for compliance, this is an excellent time for the MGO GASB 87 Implementation Team to review your leases. This will ensure that you are ready to take the most important step: Implementation. In addition, we have put together an online readiness assessment that helps you evaluate where you stand in the implementation process.

About the Author:

David Bullock is a thought leader in MGO’s State and Local Government practice. An Assurance and Government Advisory Services Partner with 25 years of professional experience, he currently oversees numerous audits and other services to governmental organizations throughout California. In 2018, David was appointed to the AICPA State and Local Government Expert Panel. He is also on the Governmental Accounting Standards Board’s (GASB) Financial Reporting Model Reexamination Task Force. In 2018, he was appointed to the California Society of CPAs’ Governmental Accounting and Auditing Committee. His numerous presentations cover topics related to generally accepted accounting principles promulgated by the GASB, and auditing standards, promulgated by the AICPA and the GAO.

The legal, legislative, and regulatory landscape of cannabis in North America is dynamic and if there has been one constant since pioneering states implemented a legal ‘seed-to-sale’ adult-use market in 2014, it is change. And it is unrelenting.

To help cannabis entrepreneurs and investors keep up with the fast pace of change in the cannabis industry we will be providing monthly summaries of the latest regulatory and legislative news to provide a snapshot of latest happenings while also highlighting matters of interest looking forward.

This month the focus is on prominent federal legislative activity (e.g. the SAFE Act and the STATES Act), state legalization measures (e.g. NJ, NY, IL, and others), and two bills in Colorado that have the potential to attract out-of-state investment to that market.

Changes in federal cannabis legislation

With control of the House of Representatives being transferred to the Democratic party, several bills that have the potential to profoundly impact the cannabis landscape have advanced in Congress. For example, the last week of March saw the House Financial Services Committee move forward the Secure And Fair Enforcement (SAFE) Banking Act to a full House vote, reportedly “within weeks.” Following the momentum of the House bill, U.S. Sens. Jeff Merkley (D-OR) and Cory Gardner (R-CO) have introduced the companion bill in the Senate.

The latest SAFE iteration addresses the cannabis banking crisis and includes amendments that offer protection to insurance companies and other financial services companies.

The banking issue is long-standing and predates even the implementation of recreational cannabis in the US. The lack of straight forward access to fundamental banking services for the cannabis industry creates a multitude of challenges, most notably the operational and financial difficulties of a multi-billion-dollar industry operating almost entirely in cash. This has obvious implications for public safety and potential diversion to the black market, among other concerns.

The inability to access banking services is often identified as a major hindrance to market entry for large and well-resourced corporations and removal of this barrier could herald a seismic shift in investment into the cannabis industry. At time of writing the House Bill had 152 cosponsors, including 12 Republicans, whereas the Senate bill has 20 co-sponsors.

Adding further momentum to the SAFE bill, last week Last week, Secretary Steve Mnuchin offered his support for a legislative fix for the banking issues facing the cannabis industry. “There is not a Treasury solution to this. There is not a regulator solution to this,” he said. “If this is something that Congress wants to look at on a bipartisan basis, I’d encourage you to do this.”

Another potentially substantial piece of legislation is the Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act), which aims to reduce conflict between federal and state laws as they relate to cannabis. The STATES Act is a potential gamechanger for the cannabis industry, allowing legal certainty for companies seeking to operate in dozens of jurisdictions across the US.

Although this legislation stalled in December, it was reintroduced on April 4th, alongside other measures, which include:

the Ending Federal Marijuana Prohibition Act that would effectively legalize marijuana at the federal level by removing it from the Controlled Substances Act.

The Marijuana Justice Act of 2019

The extent to which these bills have bipartisan support may be crucial if they are move beyond the House.

Four steps forward and two steps back in state legalization efforts

It has been a mixed month in terms of advancing cannabis legalization measures at the state level. On the one hand, there has been progress in multiple states, such as Connecticut, Illinois, and New Hampshire. While on the other hand there was a couple of snags holding up the implementation of recreational markets in New Jersey and New York.

The New Jersey cannabis legalization bill was pulled due to lack of support although Gov. Murphey (D) reportedly stated he remained committed to getting the bill passed.

New York dropped cannabis legalization from its budget bill where it was viewed as more likely to pass, however, regulators remain optimistic of progress later in the year. The New York City Council also voted to ban cannabis testing for job applicants.

A General Law Committee in the Connecticut Legislature approved a bill that would legalize an adult-use cannabis market in the state.

A bill to legalize retail cannabis in Illinois was introduced and passed to a subcommittee for further consideration.

Governor of Guam signed a bill legalizing cannabis, becoming the first US territory to do so.

Despite the hiccups outlined above, there is a clear trend towards legal cannabis across the US. Moreover, several states took steps towards expansion or liberalization of their medical cannabis markets. Certainly in the long term, the outlook is optimistic for the cannabis industry on a number of fronts.

Back to the future as Colorado looks to position itself as an investment hub for cannabis

When Colorado became the first state to implement an adult-us cannabis framework in 2014, out of state investment was restricted. This allowed the state to build upon its existing medical cannabis market.

The understandable caution has since been questioned, however, and a Bill offering more flexibility in investment passed both the Colorado House and Senate in 2018, only for then Gov. Hickenlooper to veto it. In 2019, a replacement Bill was introduced and has recently passed its third reading in the House unamended.

As an established market with mature regulations and market stability, Colorado has low-risk potential when compared to emerging markets in other states – although competition is likely to be strong, with ever-thinning margins as prices continue to drop in the state.

Out-of-state investors exploring options in Colorado may be interested in acquiring social consumption licenses in Denver, or seek opportunities for market expansion in the delivery segment of the market. If passed, HB19-1234 would allow licensed dispensaries to offer these services for the first time.

Alternative Engagement Types: Consulting Services, Agreed-Upon Procedures, and Performance Audits

By Scott P. Johnson, CPA, CGMA Partner, Macias Gini & O’Connell LLP State and Local Government Advisory Services

I have spent most of my professional career over the past 35 years serving government agencies and focusing on performance improvement, accountability, and transparency. I recognize the need for continuous monitoring and oversight in the public sector to ensure performance, public accountability, and stewardship of public resources. While participating on a number of professional panels and presentations throughout my career, I have often stated that I embraced the auditor and have welcomed them with open arms into the organizations that I had responsibility over. Why? Because I see auditors as an independent and objective lens, adding value to review and evaluate performance and to make recommendations for improvement. The organizations I have had the pleasure to work for took public accountability very seriously and supported performance improvement as a means to better serve their communities and stakeholders.

Much like a traditional CPA firm can provide different types of services related to an entity’s financial statements, i.e., audit, review, or compilation, based on need, when government agencies are considering an independent evaluation of performance of their programs or operations, the CPA firm’s advisory or consulting arm can step in and offer a number of engagement types based on the agency’s unique needs: consulting services engagements, attestation engagements (e.g., agreed-upon procedures), and performance audits. It all depends on if, and at what level, assurance is needed. The primary driver of what type of product should be considered is typically based on, for instance, issue complexity, taxpayer concerns or expectations, statute requirements, or increased need for transparency on the efficiency and effectiveness of operations. While the driver of the engagement may differ, time constraints and budget are also determining factors.

This is the first article in a three-part series focusing on performance audits. The primary focus of this article is to discuss the differences of the three aforementioned types of engagements – consulting services, agreed-upon procedures, and performance audits – and to provide guidance when a performance audit might be an option.

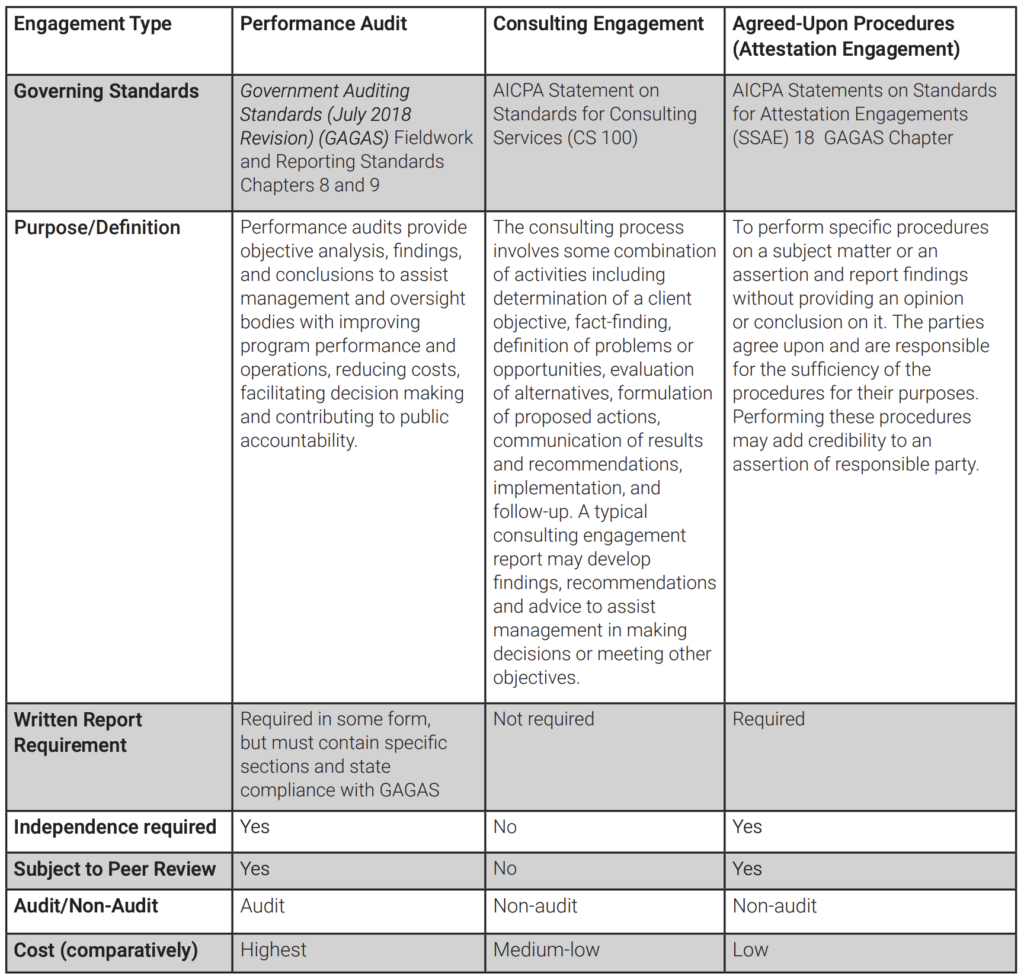

It is important to identify the differences between (1) performance audits, (2) consulting services engagements, and (3) agreed-upon procedures attestation engagements. On numerous occasions throughout my government service career and also while serving clients, questions have come up regarding the objectives sought, the scope of the engagement, and the engagement type when considering an evaluation of performance for a particular program or area of operations. Each of these engagements differ in purpose and reporting requirements, as well as potential cost, as shown below in Figure 1.0. These engagements are governed by different standards, formal reports are not always required for each, and independence is not always required (i.e., consulting services).

Performance Audits Defined

Performance audits are defined as engagements that provide objective analysis, findings, and conclusions to assist management and those charged with governance and oversight to, among other things, improve program performance and operations, reduce costs, facilitate decision making by parties with responsibility to oversee or initiate corrective action, and contribute to public accountability. *1

Furthermore, GAGAS states that management and officials of government programs are responsible for providing reliable, useful, and timely information for transparency and accountability of these programs and their operations. Legislators, oversight bodies, those charged with governance, and the public need to know whether (1) management and officials manage government resources and use their authority properly and in compliance with laws and regulations; (2) government programs are achieving their objectives and desired outcomes; and (3) government services are provided effectively, efficiently, economically, ethically, and equitably. *2

Agreed-Upon Procedures (AUP)

Based on my experience, it usually comes down to identifying a few factors that determine the engagement. First, the agency must determine the purpose and scope of the work, specifically what questions they would like to have answered. These questions can be broad or very narrow. For example, in an AUP, management may make an assertion about whether a subject matter is in accordance with, or based on, established criteria that is the responsibility of a third party and hires a CPA to add credibility to that assertion by performing specific procedures to test compliance with the criteria. If an agency needs to know something very specific and wants an independent party to perform specific procedures and tell them what was found, then an AUP is appropriate. However, an AUP report does not provide recommendations, an opinion, or conclusion about whether the subject matter is in accordance with, or based on, the criteria, or state whether the assertion is fairly stated. While the agency may want to use an AUP, some key steps that are taken in consulting engagements and performance auditing, such as planning, are not required in an AUP engagement. Also, risk is not assessed in developing the scope, nor does the auditor use a risk-based approach, which is required in a performance audit. Finally, in an AUP, auditors do not perform sufficient work to be able to develop elements of a finding or provide recommendations.

1 See Paragraph 1.21 of GAGAS. 2 See Paragraph 1.02 of GAGAS.

Consulting Services Engagement vs. Performance Audit

For a consulting services engagement or performance audit, the initial questions are then turned into the objectives of the engagement. If the agency wants an objective review of operations or a program to assist them in making decisions, for example, to assess the management of specific funds, and wants findings and recommendations to improve operations, then the agency should discuss the options of a consulting services engagement or a performance audit. From here, the decisions are truncated. The agency needs to consider whether the report is for an internal audience, such as governing officials, management, or staff, or an external audience, e.g., a regulatory agency or the public. If the communication is intended for internal use, then a consulting services engagement with observations and recommendations may suffice. For these engagements, findings, recommendations, and a conclusion is provided to assist management in decision making. Or, an independent third party, such as a CPA or an internal auditor, may be asked to answer the engagement’s objectives to an external audience, in which case a performance audit may be more appropriate due to the need for an independent, objective report that can withstand scrutiny and is subject to peer review. Sometimes there isn’t a choice; some agencies are bound by the government code or local ordinance to conduct audits under GAGAS.

Performance audits are typically the more costly engagement type of the three, given the amount of work required to conduct an audit and adhere to stringent standards. As we’ll explore in later articles, performance audits conducted under GAGAS provide the highest level of assurance among the three options, based on the level of work required. These audits involve developing the required elements of a finding and the documentary evidence required for planning, fieldwork, and reporting. The amount of work involved is much greater than in consulting services engagements, where observations and recommendations will suffice. Consulting services engagements are not audits and, therefore, offer no assurance. Similarly, in attestation engagements, where only specific procedures are performed, no assurance is provided. *3

Conclusion

Having been on both sides of deciding what engagement to recommend, either for an agency I worked at or to a client, it’s important to discuss the level of work required for each engagement type, the number of hours required to do the work under the appropriate standard within a reasonable time period, and the available budget. Finally, and most importantly, clients should understand that performance audits and consulting services engagements each have their place and serve unique purposes. A performance audit offers independence and objectivity at a step above a consulting services engagement, and might be the best option if a rigorous audit of a program or agency is needed. This is where the consideration of the agency’s need is paramount. There may not always be the budget or time available to conduct a comprehensive performance audit, nor a need for an in-depth evaluation or a legislative requirement to do so. In these instances, a consulting services engagement is a good option, especially when time and budget are factors. A consulting services engagement can provide a sufficient report with recommendations and advice. However, it’s important to make the agency aware of the limitations of non-audit services. In addition, the audience of the final report product and any regulatory requirements should strongly influence the decision-making process.

Forthcoming articles in this series will drill down and focus in more detail on the professional standards associated with performance audits as compared to other types of engagements, “why” an agency would want a performance audit instead of a consulting engagement or an agreed-upon procedures engagement, when a performance audit would be recommended, what key factors should be considered, and what are the expectations of the audience of the report. The third article in this series will focus on the reporting elements of a performance audit and a sample performance audit report.

*3 Attestation engagement standards are covered in GAGAS Chapter 7, and include agreed-upon-procedures, reviews, and examination engagements. Attestation examinations have the highest level of assurance, as an opinion is given; not so for the others. Auditors may use GAGAS in conjunction with other professional standards such as American Institute of Certified Public Accountants (AICPA), International Auditing and Assurance Standards Board (IAASB), or Public Company Accounting Oversight Board (PCAOB) standards. For financial audits and attestation engagements, GAGAS incorporates by reference for AICPA Statements on Auditing Standards and Statements on Standards for Attestation Engagements. In addition, the AICPA promulgates the consulting standards. AICPA standard committees have taken the position that only the U.S. Government Accountability Office (GAO) sets performance audit standards.

SOURCES OF INFORMATION AND DOCUMENTATION CONSIDERED

Government Auditing Standards, issued by the Comptroller General of the United States – July 2018 Revision (effective for performance audits beginning on or after July 1, 2019; effective for attestation engagements for periods ending on or after June 30, 2020; early implementation is not permitted)

United States General Accounting Office. Best Practices Methodology – A New Approach for Improving Government Operations. May 1995

About the Author

Scott Johnson has 35 years of experience in government administration, with a focus on successfully overseeing internal service operations including; debt management, information technology, human resources, municipal finance, and budget. He has led large and mid-sized operations for California government agencies including the cities of Santa Clara, Milpitas, San Jose, Oakland, and Concord and the County of Santa Clara. Scott is a past president of the California Society of Municipal Finance Officers (CSMFO) and a member of the AICPA Government Performance and Accountability Committee (GPAC). He is currently a partner with Macias Gini & O’Connell LLP (MGO), leading the Advisory Services sector specializing in State and Local Governments, based out of California. He welcomes any questions or comments via email: [email protected].

Greta MacDonald, MPA – Special recognition is given to Ms. MacDonald for her contributions and research for this article. Ms. MacDonald is a Director with MGO in the State and Local Government Advisory Services division. She has over 17 years of experience conducting over 35 performance audits in accordance with GAGAS, which is her specialization area.

Disclaimer: The views expressed in this article are those of the author and do not reflect the official policy or position of the GAO, AICPA, or Macias Gini & O’Connell LLP.