As ESG issues gain prominence, state and local governments must increase oversight, planning, collaboration, and transparency around these topics to maintain public trust and access financing.

Governments should develop, maintain, and regularly update public climate action plans outlining ESG risks, opportunities, impacts, and integration strategies.

Entities should explore green bonds as a growing option to raise ESG-tied funding while increasing related financial disclosures to satisfy investor expectations.

~

Environmental, social, and governance (ESG) issues are taking center stage globally, and U.S. state and local governments — especially those issuing municipal bonds — are facing rising expectations from constituents and investors alike to manage these concerns. To maintain public trust and access to financing, your government should make ESG an increased area of focus, discussion, and disclosure.

Here are a trio of ways your government can bring ESG efforts to the forefront:

1. Prioritize Leadership and Collaboration

The most successful government entities not only have designated ESG leaders (typically the “chief sustainability officer” or “head of environmental affairs”), but they have also established a direct line of oversight and communication with the government entity’s leadership teams (e.g., the mayor’s office, the office of the comptroller, etc.).

While ESG strategy and risk identification will always be owned by the head of the environmental and social functions, collaboration with the finance functions is also vital. Collaboration ensures that financial professionals can contribute their knowledge and experience to assess the financial impact of ESG initiatives and align them with broader strategies of the government.

Collaboratively embedding ESG efforts throughout your entity and not just siloing them to one specific department or group of individuals will give ESG the attention and investment it needs to make an impact.

2. Develop and Maintain a Climate Action Plan

At present, most medium-to-large government entities have formally documented “climate action plans” available on their websites — indicating this type of transparency will be considered “table stakes” moving forward.

Within the climate action plan, a clear strategy to identify and prioritize risks and opportunities is critical. A robust plan should specifically measure both the actual and potential impacts of ESG-related opportunities and risks on the government entity (such as on its financial planning and budgeting) and its stakeholders (e.g., investors and the communities the entity serves). Establishing and publicly communicating these on the entity’s website — or attached in the climate action plan — is key for accountability and understanding of these aspects of sustainability integration.

Additionally, a subset of government entities with climate action plans are also proactively updating their plans — effectively recognizing the plan should be a living and breathing document that continues to evolve with the emergence of new risks and the shifting interest of investors, regulators, and the public at large.

3. Explore the Potential of Green Bonds

Due to the increasing importance of sustainability and ESG for state and local governments, the issuance of green bonds by government entities will also continue to grow. Investors are expecting more financial disclosures to help them make decisions and track both opportunity and risk.

A green bond is a fixed income debt instrument occurring when an issuer (in this case, a state or local government) borrows a large amount of money from investors to use in projects focused solely on sustainability. They are similar in function to traditional bonds, except the funds acquired through them can only be dedicated to projects dedicated to energy efficiency or sustainability requirements and frameworks.

Because investors face risk when it comes to investing in municipal securities (like green bonds), it is crucial for these municipalities to have dedicated ESG leaders, offices, and transparent budgets.

Embracing ESG Principles and Building Positive Public Perception

With intensifying investor and community demands, state and local governments can no longer view ESG as an afterthought. Implementing robust oversight frameworks with designated leadership, continually updated climate action plans, and increased financial disclosures can help you meet expectations, mitigate risks, and contribute to long-term fiscal sustainability.

Need assistance implementing and managing your government’s ESG efforts? Our State and Local Government Practice offers ESG materiality and benchmark assessment, reporting and disclosure, data lineage and integrity, and net zero strategy development and monitoring. Reach out to our team today to learn how we can help you achieve your goals.

Environmental, social, and governance (ESG) information helps investors, regulators, and the public-at-large understand and interpret a government entity’s risk profile and its ability to drive positive impact.

To present this information publicly, government entities are developing robust “Climate Action Plans,” which are reviewed and refreshed on a periodic basis.

As disclosing ESG-related information to the public becomes more common, government entities are also expanding ESG-related disclosures within annual financial reports.

Coined in a 2004 United Nations report, the term “environmental, social, and governance” (and its accompanying acronym “ESG”) is less than 20 years old. Yet, you would be hard-pressed to find a boardroom today where ESG is not top of mind. It is not just businesses either — ESG is also an increasingly important topic of discussion within government organizations.

State and local governments use ESG-related information as a mechanism to measure and track priorities, footprints, and targets. As governments have matured, ESG reporting and presented information more consistently with year-to-year comparability, investors*, regulators, and the public-at-large have sought out this reporting to help them understand risk and the government entity’s ability to drive positive impact.

*Note: The term “investors” refers to those who are exploring and/or holding investments in government-issued securities (e.g., hedge funds, institutions, individuals, etc.).

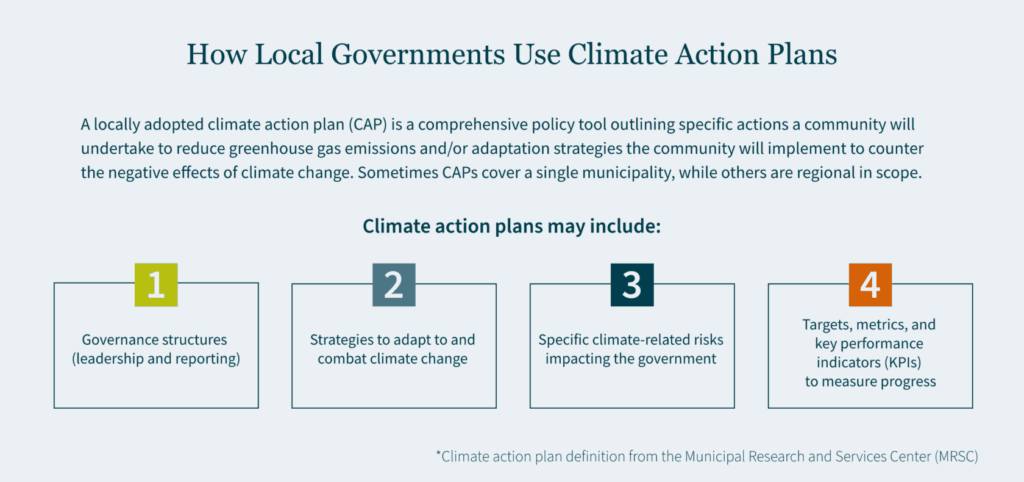

The Increasing Importance of “Climate Action Plans”

To present ESG-related information to the public, many government entities develop and communicate robust “Climate Action Plans”. These plans highlight a myriad of information, including (but not limited to):

Governance structures (e.g., communication and reporting lines from environmental leadership into the mayor’s office)

Strategies to adapt to and combat climate change

Specific climate-related risks, which impact the government entity

Targets, metrics, and key performance indicators (KPIs) used to measure progress

As Climate Action Plans continue to evolve, governments are commanding and allocating more financial resources to activate these plans. With the increased focus on climate-related initiatives presented in Climate Action Plans, we are seeing an expansion of ESG-related information disclosed within “Annual Comprehensive Financial Reports” across the country — a sign that financial disclosures are maturing to meet growing interests from investors, regulators, and the public-at-large.

A Growing Push from Investors and Regulators

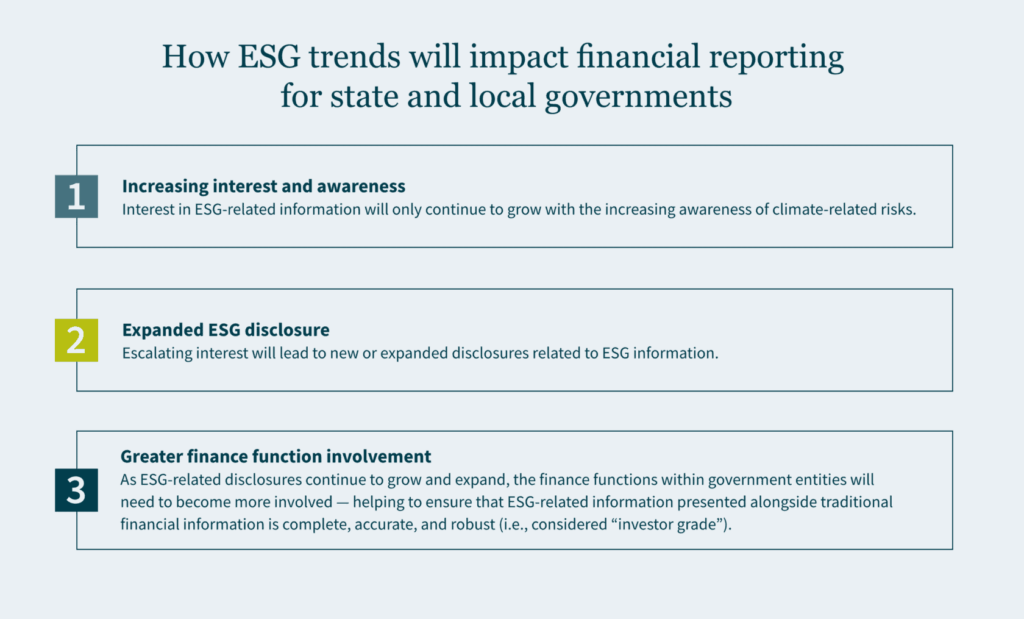

The focus on non-financial risks (including, but not limited to, ESG-related risks) by investors and regulators continues to intensify. When we take a step back to analyze the trend, a few things become clear:

Interest in ESG-related information will only continue to grow with the increasing awareness of climate-related risks.

Escalating interest will lead to new or expanded disclosures related to ESG information.

As ESG-related disclosures continue to grow and expand, the finance functions within government entities will need to become more involved — helping to ensure that ESG-related information presented alongside traditional financial information is complete, accurate, and robust (i.e., considered “investor grade”).

To dive deeper into that last point, where would a finance function start? The short answer is by increasing the integration and collaboration between a government entity’s environmental leaders and the finance functions. The longer answer is that government entities need to develop holistic approaches to collecting and reporting robust ESG-related information to meet the expectations of investors, regulators, and the public-at-large.

The bottom line: As the issuance of and investment in municipal securities continues to grow, the quality of ESG-related information disclosed to the public will need to be enhanced to meet the demands of investors.

Transparency in Budgets and Financial Reporting

With an increase in ESG-related disclosures in annual financial reports by government entities, recent interpretive guidance from the Governmental Accounting Standards Board (GASB) indicates that government entities can expect further scrutiny and regulation as these types of disclosures become more commonplace.

Essentially, it is important for your government to have a robust, well-communicated ESG “story” within a Climate Action Plan — but you also must provide investor-grade transparency within audited financial statements. Government entities are already beginning to meet this challenge. Two examples of local governments with a growing presence of ESG-related information in their Annual Comprehensive Financial Reports are the City and County of San Francisco and the City of Fremont.

The City and County of San Francisco transparently discloses both environmental and social initiatives, capturing details related to its Environmental Protection Fund, as well as specific details related to revenues received from state, federal, and other sources for the preservation of the environment.

The City of Fremont — which is much smaller in terms of population (~230,000) and financial resources (roughly $1.5 billion in total primary government assets from “government activities”) — depicts ESG-related information throughout its annual report, including but not limited to qualitative information in the “management discussion and analysis” section, as well as quantitative information related to “community development and environmental services.”

The Path Forward: Enhancing Your ESG Reporting

With ESG-related information becoming more integrated into investor decision-making, your government needs to focus on enhancing its Climate Action Plans and developing “investor grade” disclosures related to ESG risks and opportunities for inclusion within your traditional financial reporting. These initiatives will require additional financial resources and human capital to create and maintain — and further collaboration between environmental, social, and financial leaders will be needed to drive the change.

How MGO Can Help

Incorporating ESG disclosures into financial reporting can pose challenges to states and local governments unfamiliar with ESG reporting standards. With experience providing ESG solutions, our State and Local Government Practice will work with your team to meet requirements and make information “investor-ready,” while also ensuring accountability and transparency.

President Biden has signed the Inflation Reduction Act of 2022 into law.

This large package contains many new tax credits to incentivize taxpayers to “go green” with energy from renewable resources while simultaneously receiving financial relief.

It also extends or adds to currently existing credits for additional tax-saving opportunities.

These new credits are aimed at motivating taxpayers to use energy from renewable sources, prioritizing options like wind and solar. The IRA also introduces new credits and strengthens or extends existing credits that provide tax relief for purchasing new and used clean-energy vehicles and installing energy efficient heating and cooling systems. Additionally, companies that cut their methane emissions can access certain credits, while those that do not could face penalties.

The rules and regulations around claiming these green credits can be complicated. In this article, our Tax Credits and Incentives team breaks down how individuals and organizations can capitalize on these tax saving opportunities.

Swap gas guzzlers for an electric vehicle

Taxpayers that purchase a new or used “clean car” can qualify for this consumer tax credit. Vehicles considered clean are those that use a battery partly or fully manufactured in North America and built with materials extracted or processed in one of the countries currently in a free-trade agreement with the U.S.

Your income is a factor in how much you can reap in tax credits. If a taxpayer makes less than $150,000 annually (or has a combined family income below $300,000), the taxpayer can get up to $7,500 for new electric vehicles that qualify. Note the money would be applied at the point of sale, so the taxpayer’s monthly payments would be lowered (as opposed to reducing the tax bill months down the line).

Previously, the federal tax credit for electric vehicles did not include cars from manufacturers that already sold at least 200,000 models (GM, Toyota, and Tesla were excluded). This bill unravels that; instead, there is now a price threshold per vehicle. To qualify for the credit, bigger vehicles like SUVs, pickup trucks, and vans would have to cost less than $80,000 to qualify for the credits. Smaller vehicles are capped at $55,000. So, if you have your eye on a super sporty electric vehicle, you may be out of luck.

Taxpayers can also get $4,000 off a used electric vehicle if it is sold by a dealer for $25,000 or less — but only if they individually make up to $75,000 annually or $150,000 jointly. The addition of credits for used electric vehicle purchases is a win for the industry, and advocates of the bill are hopeful that this incentive will encourage an increase in electric vehicle adoption.

Modifying your home to be more energy efficient

To incentivize taxpayers to make their homes more energy efficient, the bill’s $4.28 billion High-Efficiency Electric Home Rebate Program provides rebates for low- and moderate-income households when they replace fossil-fuel boilers, furnaces, water heaters, and stoves with more efficient electric devices powered by renewable energy.

Some taxpayers will need to upgrade their electrical panels before they are able to install the new appliances. They can take advantage of up to $4,000 to do so. Furthermore, if they are interested in making their home generally more energy efficient, they can capitalize on a rebate of up to $1,600 given to seal and insulate their house, as well as up to $2,500 to improve their home’s wiring.

In terms of appliances, taxpayers can get up to $8,000 to install heat pumps that both heat and cool their home, plus as much as $1,750 for a heat-pump water heater. To offset the cost of a heat-pump dryer or electric stove, taxpayers can claim up to $840. It is estimated by making these changes, they can save significantly on their future energy bills.

There are several parameters for these rebates. First, the program runs through September 30, 2031 — so you do have time to implement these changes to your home. The maximum amount taxpayers can collect is $14,000, and to qualify, their household income cannot exceed $150% of the median income in the area they live. For those who do not qualify, there is a tax credit of up to $2,000 available to install heat pumps, plus up to $1,200 annually to install new windows, doors, or an induction stove.

Save when installing solar panels

Lastly, taxpayers can collect a 30% tax credit for installing residential solar panels through December 31, 2034. The credit decreases to 26% if you wait until after December 31, 2032. Taxpayers can also install solar battery systems to qualify for the tax credit.

New “green” tax credits

There are other ways taxpayers can take advantage of going green. Here are some of the new tax credits to capitalize on.

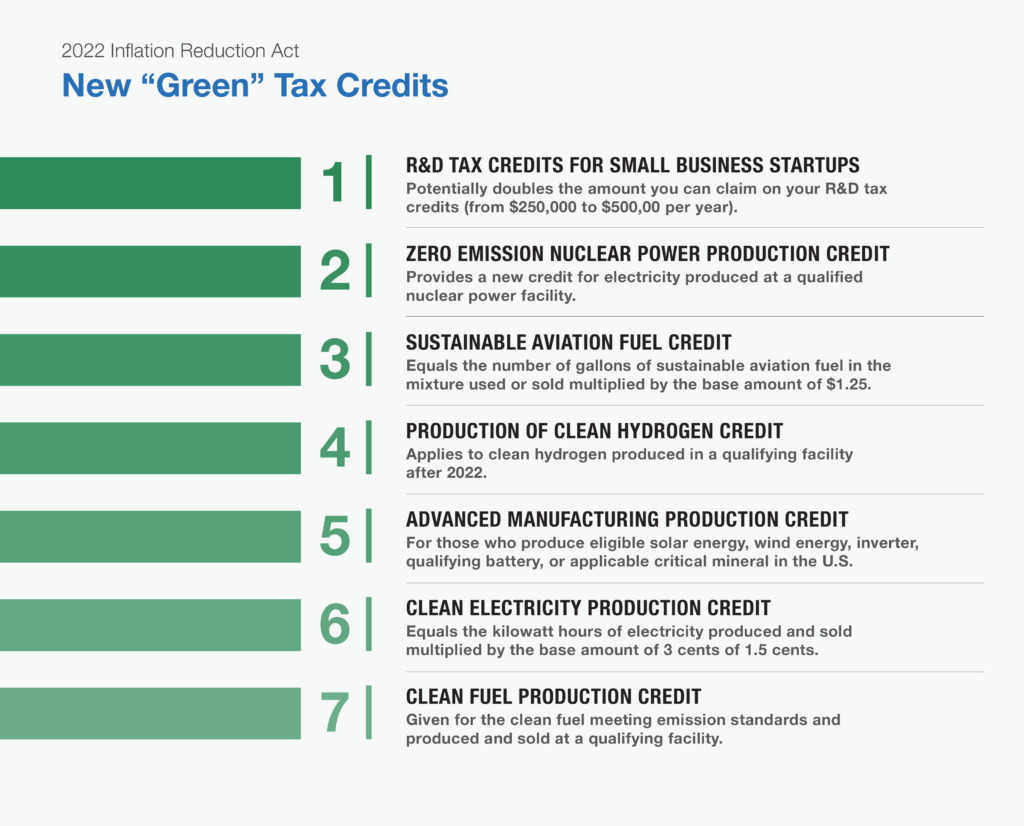

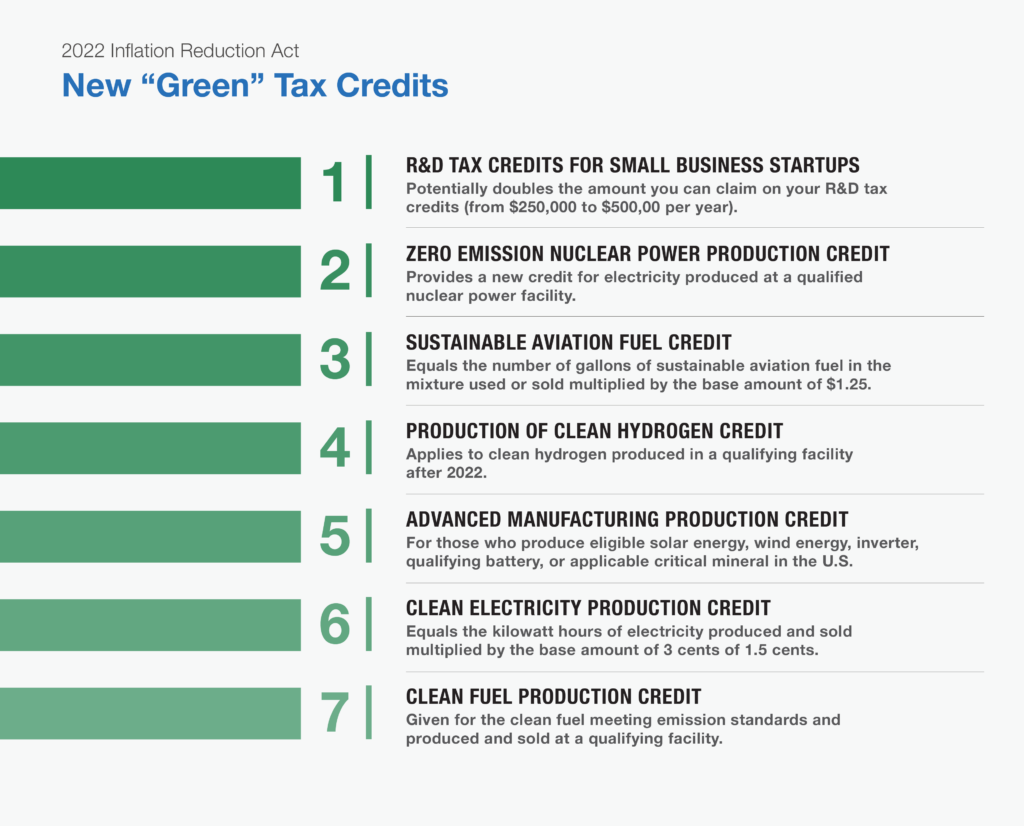

Doubling of R&D Tax Credits for Small Business Startups — Would potentially allow recipients to double the amount they can claim on any R&D tax credits (from $250,000 to $500,000 per year against payroll taxes).

Zero Emission Nuclear Power Production Credit — Provides a new business credit for electricity produced by a taxpayer at a qualified nuclear power facility before the date of enactment.

Sustainable Aviation Fuel Credit – Creates a new business credit for each gallon of sustainable aviation fuel sold or used as part of a qualified fuel mixture. The credit equals the number of gallons of sustainable aviation fuel in the mixture multiplied by the base amount of $1.25. There are increases available if the taxpayer meets certain greenhouse gas emissions reductions, and it applies to fuel sold or used in 2023 and 2024.

Production of Clean Hydrogen Credit — Given to producers of clean hydrogen during the ten-year period beginning on the date a qualifying facility is originally placed in service. It applies to clean hydrogen produced after 2022.

Advanced Manufacturing Production Credit — Provides a new production credit for each eligible solar energy component, wind energy component, eligible inverter, qualifying battery component, and applicable critical mineral produced by a taxpayer in the U.S. (or in U.S. possession and sold to an unrelated person). It applies to components and minerals produced and sold after 2022.

Clean Electricity Production Credit — New business credit for clean electricity facilities placed in service after 2024 (where the greenhouse gas emissions rate is not greater than zero). The credit amount equals the kilowatt hours of electricity produced and sold multiplied by the base amount of 3 cents or 1.5 cents. The credit will phase out one year after the later of 2032 or the year when annual greenhouse gas emissions from U.S. production are equal to less than 25% of the 2022 emissions rate (whichever comes first).

Clean Electricity Investment Credit — New investment credit for clean electricity property investments in energy storage technology and qualified facilities placed in service after 2024 where the greenhouse gas emissions rate is not greater than zero. It phases out after the later of 2032 or when the annual greenhouse gas emissions from U.S. electricity production are equal to or less than 25% of the 2022 emission rate (whichever comes first).

Clean Fuel Production Credit — Creates a business credit for the clean fuel a taxpayer produces at a qualifying facility and sells for qualifying purposes. The fuel must meet certain emissions standards.

Extension and modification of “green” tax credits

Several tax credits already in existence were extended and modified in the Inflation Reduction Act. They include:

Renewable Electricity Production Tax Credit (PTC) — Extends the beginning of construction deadline for certain renewable electricity production facilities through the end of 2024, as well as reduces the base amount of credit with the potential to qualify for five times that amount. It applies to facilities placed in service after 2021, and increases the credit amounts for domestic content, energy communities, and hydropower.

Energy Investment Tax (ITC) — Extends the beginning of construction deadline for some types of energy property, including qualified fuel cell property, for one year through the end of 2024. It extends the beginning of construction deadline for geothermal equipment through the end of 2034 and permits the credit for new types of energy property like energy storage technology, microgrid controller property, and qualified biogas.

Carbon Oxide Sequestration Credit — Extends and enhances carbon oxide sequestration credits for qualified industrial facilities and direct air capture facilities IF construction begins before 2033. It also lowers the minimum carbon capture requirement, and generally applies to those facilities and equipment placed in service post-2022.

Tax Credits for Biodiesel, Renewable Diesel, and Alternative Fuels — Extends these tax credits through 2024 and apply to fuel sold or used after 2021.

Second Generation Biofuel Credit — Extends tax credits to second generation biofuel through 2024 and applies to second generation biofuel production after 2021.

Nonbusiness Energy Property Credit — Extends this credit through 2023, as well as changes the credit rate to 30% for both qualified energy efficiency improvements and residential energy property expenditures. It replaces the $500 lifetime limit with a $1200 annual limit, modifies the limits for specific types of property, and modifies standards for qualified energy efficiency improvements on property placed in service after 2022.

Residential Energy Efficient Property Credit — Extends the residential energy-efficient property credit through 2034 and replaces the credit for biomass fuel property expenditures with a new credit for battery storage technology expenditures on those made after 2022.

New Energy Efficient Home Credit — Extends the business credit for contractors who manufacture or construct energy efficient homes through 2032. It applies to dwellings acquired by the contractor after 2022.

Alternative Fuel Vehicle Refueling Property Credit — Extends the tax credit through 2032 and increases the credit limit to $100,000 per item of depreciable refueling property and $1,000 per item of non-depreciable refueling property.

Advanced Energy Project Credit — Extends the competitively awarded investment tax credit for clean energy and energy efficiency manufacturing projects. It provides as much as $10 billion of new credit allocations effective in early 2023.

Increase in Energy Credit for Solar and Wind Facilities — In order to qualify, one must have a maximum net output of less than five megawatts and must be in a low-income community, on American Indian land, or part of a low-income residential building project (or low-income economic benefit project), effective in early 2023.

Reinstatement of Superfund Hazardous Substance Financing Rate — Reinstates a financing rate on crude oil and imported petroleum products at a rate of 16.4 cents per gallon through 2032.

Our perspective on the Inflation Reduction Act’s tax credits

Looking ahead, it is imperative that you are ready to capitalize on these tax credits. Getting into the weeds with some of the qualifications, however, could prove challenging, and working with a professional services firm could make all the difference in ensuring you take advantage of the credits you qualify for.

At MGO, our dedicated Tax Credits and Incentives team brings more than 30 years of experience in helping you structure your expenses in a way that will help you acquire appropriate documentation, assist in calculating and claiming credits, and maximize the amount you can receive. Our full-service firm, led by experienced CPAs and attorneys, provides a holistic approach to examining your organization and determining how you can best reach your goals.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

We can expect that ESG-related disclosures will shift from voluntary guidance to mandatory reporting at some point.

Reporting and disclosure of environmental, social, and governance (ESG)-related information has long been a priority in the private sector and is now emerging as a key area of focus for state and local governments (or “government entities”).

In response to interested parties seeking more ESG-related information (e.g., investors, credit rating agencies, preparers and auditors of financial statements, citizens, policymakers, etc.) from government entities, the Governmental Accounting Standards Board (GASB) has released a publication to clarify how ESG-related information intersects with their existing standards.

The bottom line: GASB’s stakeholders and interested parties are seeking to understand the impacts of ESG-related matters on a government entity’s cash flows, financial position, and overall responsibility for fiscal accountability — and the publication can be seen as a form of interpretive guidance to bridge the gap.

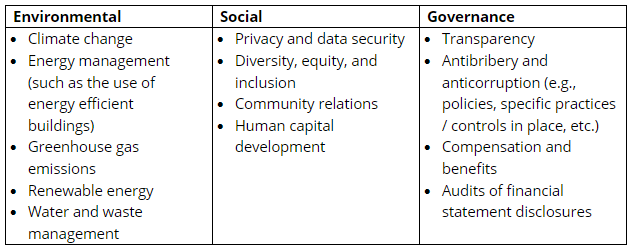

Up front, the publication acknowledges that “a single consistent definition of ESG is not prevalent in practice today.” However, broad examples are included in the publication for each pillar (note, the below list has been shortened for purposes of this article):

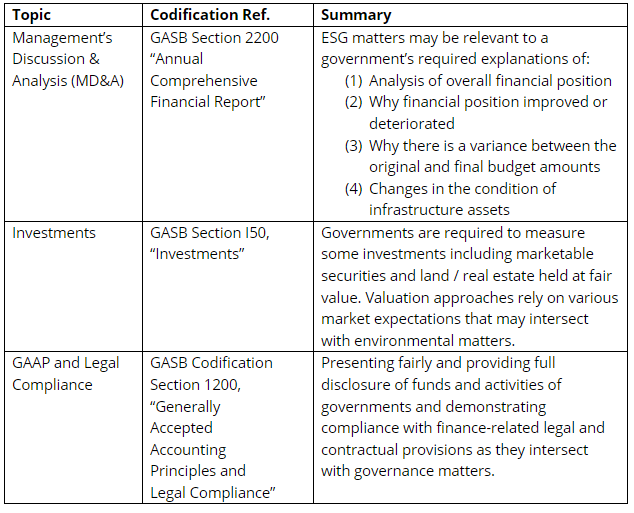

The interpretive portion of the publication goes on to assist government entities with detailed examples of how ESG-related information coincides with the current GASB standards (note, the below are 3 of 25 total examples from the publication):

Why this GASB release matters

In publishing this document, GASB is taking a traditional first step to introduce concepts and guidelines that set a foundation ahead for new reporting and disclosure rules in the future (also referred to as “interpretive guidance”).

This is not the first time a regulator or standard setter has issued interpretive guidance specific to ESG. In 2010, the Securities and Exchange Commission (SEC) released their own interpretive guidance to provide clarity to the private sector on how to leverage existing financial reports to make disclosures related to climate change. While it was uncertain how many companies would incorporate climate-related information in their financial reports, many chose to do so (at last count by the SEC in 2020, 33% of the 6,644 filings submitted to the regulator contained some form of climate-related disclosure). The interpretive guidance, therefore, laid the groundwork for a new climate-related proposal issued by the SEC in March 2022.

Essentially, interpretive guidance has historically preceded the release of new, formal guidance and the creation of new standards. If this proves true in the public sector, then we will first see an increase from state and local governments enhancing their existing financial reports and disclosures by incorporating ESG-related information. Subsequently, and after further analysis by GASB of those enhanced disclosures, we will likely see the release of a new ESG-specific standard from GASB.

Increasing the pressure

As demand for ESG-related disclosures increases, pressure will also increase on governments to begin providing or enhancing the disclosures in their financial reports. Further, if your entity issues securities (e.g., municipal bonds), you may encounter pressure from credit rating agencies depending on your approach (or lack thereof) to disclose and address ESG-related risks.

At present, ESG-related disclosures are contingent on a variety of factors (including but not limited to the government entity’s location, the historical or anticipated impacts of climate change, the level of ambition to become a leader in ESG-related reporting, etc.), but at some point these disclosures will shift from voluntary to mandatory.

How MGO can help

Many state and local governments have proactively disclosed ESG-related information on their websites or in standalone ESG / sustainability reports; however, GASB’s interpretive guidance demonstrates that ESG-information also needs to be considered when preparing your annual financial reports.

To stay ahead, MGO is helping the public sector as well as the private sector, develop and enhance their ESG disclosure strategies.

If you are interested in learning more, schedule a conversation with our ESG team today.