If your business is contemplating a liquidity event, it is critical to prioritize sell-side tax due diligence well before entering the market.

It is especially important to focus on state and local tax (SALT) issues, as evidenced by South Dakota v. Wayfair, which widened the ability of states to tax out-of-state sales.

Seek guidance from a sell-side advisor — doing so can significantly impact the success of your transaction.

~

If your business is contemplating a liquidity event, prioritizing sell-side tax due diligence — with a special focus on state and local tax (SALT) issues — is crucial. Engaging in sell-side tax diligence well before hitting the market, under the guidance of a sell-side tax advisor, is a strategic move that can significantly affect the success of the transaction.

Why Focus on SALT?

The complexity of SALT liabilities can pose major hurdles during buy-side diligence. This is especially true in the wake of South Dakota v. Wayfair, which broadened states’ ability to tax out-of-state sales. Addressing these issues proactively allows sellers to navigate potential deal delays and negotiate more favorable terms, and helps ensure a smoother transaction process. This focused approach not only showcases the business as well-managed and compliant with intricate SALT complexities, but it also enhances the company’s appeal as an acquisition target.

The Benefits of a Wellness Check

Conducting a thorough wellness check on your company’s state tax posture can minimize the risk of surprises that could lead to renegotiations or even deal termination. This also can position the seller to potentially secure a higher sale price by demonstrating a comprehensive approach to SALT compliance and risk management.

Mitigating SALT Exposures

Using voluntary disclosure agreements (VDAs) and diligently collecting sales tax exemption certificates are effective strategies for mitigating SALT exposures. VDAs allow sellers to address historical sales tax liabilities under favorable terms, including the elimination of penalties. The VDA process not only remediates historical tax liabilities, but it also signals a commitment to compliance that can be reassuring to buyers. Further, maintaining sales tax exemption certificates helps ensure that exempt sales are properly classified, which can reduce the risk of future exposure.

The Risk of Noncompliance

Attempting to address past noncompliance through prospective filings, rather than by remediating historical exposures, leaves businesses vulnerable to exposure identified by state tax authorities and buy-side diligence teams. A VDA can limit this exposure by reducing the lookback period and eliminating penalties. Without a VDA, businesses risk historical liabilities that can significantly exceed those that could have been negotiated under a VDA.

Being Proactive

Ultimately, sell-side due diligence empowers sellers to be in a better position with all issues related to tax compliance. This proactive approach is far more efficient than reacting to a conservative exposure identified by buy-side advisors, which can take significant time and resources to address or refute.

Prioritization Is Key

Prioritizing sell-side tax diligence, especially for SALT issues, is a strategic move that can enhance a company’s attractiveness to potential buyers, minimize transaction delays, and potentially lead to amore favorable sale outcome.

How MGO Can Help

Preparing for a liquidity event can feel like a battlefield — dodging land mines and watching where you step. Strategic planning and meticulous attention to your tax compliance are crucial, and MGO is well-equipped to support your business in navigating the challenge of sell-side tax due diligence. With our thorough understanding of the intricate dynamics of SALT issues and the impact they can have on your organization, we provide tailored guidance to help position your business for the best sale possible.

Our team excels in a proactive approach: conducting thorough wellness checks, identifying potential SALT liabilities, and implementing effective strategies to mitigate historical tax exposures and minimize transaction delays — and enhance your company’s appeal to those looking to buy. For inquiries or support in prioritizing your sell-side tax due diligence, reach out to our team today.

The potential rescheduling of cannabis presents an opportunity to reevaluate your company’s tax structure and increase deductions, reduce income, and simplify accounting.

Rescheduling may open up access to previously unavailable tax credits, incentives, and deductions at various government levels.

With anticipated increased investment and cash flow after rescheduling, companies should prepare for potential mergers and acquisitions by seeking support in areas like financial due diligence and post-acquisition planning.

~

The rescheduling of cannabis from Schedule I to Schedule III will unlock new opportunities for cannabis businesses. Is your company positioned to capitalize?

Tax Restructuring

If your existing operating structure was optimized for Section 280E mitigation, now is the time to evaluate whether it will still be tax-efficient after rescheduling.

MGO’s dedicated cannabis tax team can analyze your current structure and identify opportunities to increase deductions, reduce income, simplify accounting, and eliminate unnecessary tax exposures. We will help you develop a strategy specific to your business needs that aligns with your operational goals and any regulatory considerations.

Tax Credits, Incentives, and Deductions

Rescheduling should open cannabis operators to a world of previously unavailable tax benefits.

Our tax professionals can comprehensively review your business operations to uncover tax credits, incentives, and deductions that you may qualify for at the federal, state, and local levels.

Financial and Internal Control Audits

While rescheduling will eliminate the Section 280E tax burden and attract new investors to the cannabis industry, it could also lead to a new regulatory framework.

Our audit services can provide assurance to investors that your company is effectively managing risks, complying with any regulatory changes, and maintaining transparency.

Mergers and Acquisitions (M&A)

The projected wave of investment and increased cash flow resulting from rescheduling means more M&A should be on the horizon.

If your company is considering an M&A deal (either as a buyer or seller), MGO can support your efforts with structuring, financial & tax due diligence, Quality of Earnings (QoE) assessments, accounting integration, strategic guidance, and post-acquisition planning.

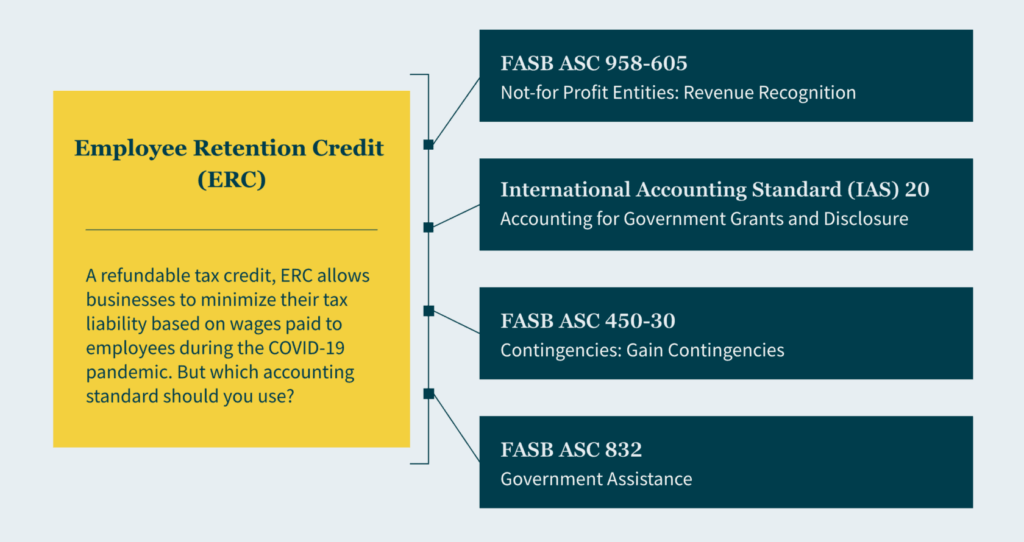

There is still uncertainty about how to account for the refundable Employee Retention Credit in your books, because you can’t account for it the same way you can account for the Paycheck Protection Program loan.

The standards you can choose from are FASB ASC 958-605, International Accounting Standard (IAS) 20, FASB ASC 450-30, and FASB ASC 832.

Depending on the standard you choose, you might have to consider the timing of recognition, the presentation of a grant income line, and financial ratios.

The Paycheck Protection Program (PPP) and the Employee Retention Credit (ERC) were powerful economic stimulus programs instituted during the COVID-19 pandemic to provide financial relief to struggling businesses. Both programs were the first initiatives of their kind, and as a result, there remains some uncertainty about what standards apply when accounting for them in your financial statements and records.

If you’re wondering how to distinguish the two, as well as determine the standard you should be utilizing, Angel Naval, a leader in our Client Accounting Solutions practice, breaks it down.

The PPP versus the ERC

Created to aid businesses facing financial challenges through the pandemic, there are several key differences between the PPP and the ERC.

The PPP is a loan and was created for small businesses with less than 500 employees in mind, giving them the funds needed to cover payroll and other eligible expenses. This includes hiring back employees who were laid off and covering applicable overhead. The loans are forgiven if the proper criteria are met (I.e., maintaining payroll and keeping consistent employee numbers).

A subset of the PPP loan, the ERC is a refundable tax credit that allows businesses to reduce their tax liability based on the qualified wages they’ve paid to their employees during the pandemic. It was created for businesses of all sizes to capitalize on in order to avoid layoffs. They can claim up to $5,000 per employee in 2020 and $7,000 per employee per quarter in 2021.

Determining the appropriate accounting standard for ERCs

If you took advantage of the ERC, currently, there is no straightforward way of accounting for it. Put simply, the ERC is a gray area because it’s so new, and there isn’t a straightforward way of accounting for it. Plus, ERCs are payroll credits, not income tax credits — and while FASB has extensive guidance for accounting for income taxes in ASC 740, it doesn’t for payroll taxes. Even the American Institute of Certified Public Accountants (AICPA) has suggested different standards, so it’s up to you to apply your best judgement based on the facts and circumstances of your business. Some things to consider:

The timing of recognition,

The financial ratios important to you, and

Whether you want to present a grant income line.

For income statement presentation, according to AICPA’s December 2022 report, more public entities are crediting the associated expense rather than recognizing the amounts on a separate line item.

For example, you may think you can account for the ERC the same way you can for the PPP, but you can’t. As we differentiated above, the PPP is a loan and the ERC is a payroll credit, therefore the PPP is subject to debt and liability standards and the ERC is not. While the PPP did come first, those companies that have paid payroll taxes but still qualified for the ERC are still able to retroactively claim the credit.

For prospective applications, for-profit entities can adhere to guidance in one of the following.

FASB ASC 958-605

If you’re applying the revenue recognition model under ASC 958-605, ERCs are treated as conditional contributions. In this case, companies must have met the program’s eligibility conditions to record revenue (and no amounts can be recorded until all criteria are evaluated and “substantially” met according to regulations). Given the conditions are met, a refund receivable and income should be recognized in the period the entity determines the conditions have been substantially met. This standard requires that gross revenue be recorded, and it doesn’t permit any netting of revenue against related expenses.

Some barriers to meeting ASC 958-605’s requirements include the eligibility requirements, like meeting the rules for a decline in gross receipts as well as incurring qualifying expenses (i.e., payroll costs). To file for the ERC, you’ll need to decide whether preparing the related ERC form and filing it with the government presents a barrier you’ll need to overcome. Note administrative and other small stipulations do not represent a barrier.

IAS 20

If you’re applying IAS 20, you can’t recognize the ERC until the “reasonable assurance” threshold is met in correlation with ERC’s conditions and receiving the credit. In this case, “reasonable assurance” translates to “probable” under GAAP standards and is easier to satisfy than “substantially met” in Subtopic 958-605. Once you’ve provided reasonable assurance that conditions will be met, the earnings impact of the government grants is recorded over the periods in which you recognize as expenses the related costs that the grants are intended to cover. So, you’ll need to estimate the amount of the credit you expect to keep.

IAS 20 allows you to record and present either the gross amount as other income or net the credit against other related payroll expenses. For every quarter that a company meets the recognition criteria, it records a receivable and either other income or net expense.

FASB ASC 450-30

If you’re interested in applying FASB ASC 450-30, please note amounts related to the ERC wouldn’t be recognized under this model until all uncertainties regarding the disposition of the credit are resolved — and there’s less detail on the disclosure, measurement, and recognition requirements as compared to the other standard models. For this reason, the AICPA doesn’t believe this model to be a preferred accounting policy for the ERC.

FASB ASC 832

If you’re applying this model, you must disclose several specifics about transactions with a government within its scope. These entail the nature of the transactions, which includes a description of the transactions as well as the form in which it has been received, whether it’s cash or other assets. You must also detail the accounting policies you used to account for the transactions. Any line items on the balance sheet and income statement that are affected by the transactions must be accounted for too — plus, the amounts applicable to each financial statement line item in the current reporting period.

How MGO can help

While there are clear accounting standards for the PPP, there is still some uncertainty surrounding the ERC. Depending on the standard you choose, you may have to consider the timing of recognition, financial ratios, and whether to present a grant income line. Therefore, businesses need to apply their best judgment based on the facts and circumstances of their business when accounting for ERCs. Our Client Accounting Solutions team has extensive experience helping clients navigate complex tax regulations post-pandemic. Contact us to learn more about which standard you should be using for federal relief programs.

About the author

Angel Naval oversees our West Coast Financial Advisory Services practice and provides value-added guidance for your corporate finance, financial planning, and business process needs.

The corporate fundraising environment has changed dramatically this year due to several factors, including a wide sell off in the equity markets, high interest rates, inflation, and a general tightening of the credit markets. Prior to the recent downturn, companies had the luxury of spending to develop their products and marketing ideas first, and then focusing on turning a profit later.

Because of these newly tightened conditions, companies may face challenges when raising capital, forcing them to adopt a more thoughtful approach to seek funding. Likewise, investors will want to ensure their priorities are protected and their returns met. The combination of a given borrower’s need for capital and a financer’s desire to seek favorable returns may lead to the creation of agreements that have characteristics of both debt and equity. As such, it is crucial for all parties involved to understand the resulting tax classification and the treatment of these arrangements, so all expectations are met.

The taxation of debt and equity

For borrowers, the difference between debt and equity can be critical because interest payments are generally tax deductible and subject to certain limitations. Dividends or other payments related to equity would not be deductible for U.S. federal income tax purposes.

Enacted as part of the Tax Cuts and Job Act (TCJA) of 2017, one main limit on interest deductibility is the IRC 163(j) limit on the amount of business interest that can be deducted each year. This limit is calculated as 30 percent of adjusted taxable income, which prior to the 2022 tax year closely resembled earnings before interest, taxes, depreciation, and amortization (EBITDA). However, starting with the 2022 tax year adjusted taxable income excludes depreciation and amortization, becoming EBIT. This should result in a lower limit on the amount of interest expense that can be deducted each year. Any interest expense exceeding this annual limit can be carried forward to future years.

Determining if an arrangement is debt or equity for federal income tax purposes

Classifying an arrangement as debt or equity is made on a case-by-case basis depending on the facts and circumstances of a given agreement. While there is currently little guidance in this area beyond case law, the Internal Revenue Service (IRS) has issued a list of factors to consider when questioning whether something is debt or equity. (Keep in mind, however, that the IRS states not one factor is conclusive.) The factors include whether:

An agreement contains an unconditional promise to pay a sum certain on demand or at maturity,

A lender can enforce the payment of principal and interest by the borrower, and

A borrower is thinly capitalized.

The courts have also established a broader — but similar — list of factors to consider when determining whether an instrument should be treated as debt or equity. Both the IRS and the courts have generally placed more weight on whether an instrument provides for the rights and remedies of a creditor, whether the parties intend to establish a debtor-creditor relationship, and if the intent is economically feasible. Some factors include:

Participation in management (as a result of advances),

Identity of interest between creditor and stockholder,

Thinness of capital structure in relation to debt, and

Ability of a corporation to obtain credit from outside sources.

For international companies, the characterization of debt or equity when considered in a cross-border funding arrangement is important, as withholding tax rates may apply to interest payments and may differ from tax rates applied to dividends. Further, withholding tax obligations occurs when a cash payment is made. If you have a cross-border arrangement, it is crucial to know if you have debt or equity on your hands.

Special rules related to payment-in-kind

Once it is determined that an agreement should be classified as debt for U.S. federal income tax purposes, some borrowers may prefer to set aside interest payments or pay interest with securities, which is often referred to as payment-in-kind (PIK). This is generally done to preserve cash flow for operations and growth of the business. When a borrower chooses this route, U.S. federal income tax rules will impute an interest payment to the lender.

While using a PIK mechanism will not automatically result in the debt being recharacterized as equity for federal income tax purposes, it can support viewing the instrument as equity.

Limits to deductible debt interest

There are limitations that can apply to interest deductibility. As noted above, IRC 163(j) limits deductibility of business interest; for a corporation, this is deemed to be all interest regardless of use. Another provision that can result in interest deductibility limitation is IRC 163(l), which applies to certain convertible notes and similar instruments held by corporations.

For cannabis operators, it is important to consider that IRC 280E disallows interest deductions. Hence, it is highly detrimental for cannabis operators to issue debt from entities that are cannabis plant-touching.

How we can help

Due to the nature of the debt versus equity analysis, companies thinking about fundraising should plan on how they intend to perform the raise and whether to have the raise treated as equity or debt. If debt classification is desired, a borrower should take the steps needed to strengthen the facts of the transaction to support the arrangement as a debt instrument.

MGO’s dedicated tax team has extensive experience advising companies across industries on capital-raising, debt refinancing and restructuring, recapitalizations, and other tax transactions. If you are planning to fundraise, or you are currently in the process of conducting a debt versus equity analysis, contact us today.

Recent events in the media have shone a spotlight on issues surrounding bad practices when it comes to tax credits and incentives. This increased attention is likely to result in an influx of audits by the Internal Revenue Service (IRS) as they crack down on the Research and Development (R&D) tax and the Employee Retention Tax Credit (ERTC) in the coming years.

We recently released an article detailing the red flags to look out when dealing with tax credits and incentives providers. If you think you could be at risk for future IRS issues, there is much you can do now to take a proactive approach and mitigate future negative impact. In the following, we break down steps you can take now to better understand and manage your exposure.

An overview of tax credits and incentives

Designed to encourage investment and development, job creation, growth, and certain business activities, tax credits and incentives provide an opportunity to reduce the amount of tax owed for performing certain activities. Credits and incentives are categorically different than tax deductions, which reduce the amount of taxable income.

These incentives often target desirable industries or activities like research and development, job creation for at-risk populations, and expanded growth in underdeveloped areas. When leveraged correctly, credits and incentives can be a powerful tool to funnel back resources into your organization to fuel activities you are already doing. Even more enticing, these credits can often apply retroactively if you determine you qualify for certain credits or incentives after the fact.

There are three basic types of tax credits: nonrefundable, refundable, and partially refundable. A few of the different types of tax credits pertaining to businesses in different classifications, industries, or activities performed include R&D tax credits, the employee retention tax credits, IRC Section 179D, and the work opportunity tax credit. To learn more about their eligibility rules, visit our previous article.

Understanding the risk of IRS tax audits

There is a three-year statute of limitations from the due date of the tax return or the filing date (whatever is later) for the IRS to assess your filings. That means if you think you may be exposed but escaped the IRS’ notice, you could still receive an audit notice for previous years’ returns. And if you do get audited, and the IRS determines you owe back taxes, you will get charged penalties and interest dating back to the infraction itself.

This is even more risky when considering the IRS’s extreme backlog. These IRS tax audits can sometimes take years to complete and if your credit and incentive calculations are the topic of interest, you’ll need to halt any future credit analysis until the situation is resolved. Meanwhile, you’ll be devoting crucial resources, time, and effort working with the IRS for something that yields no financial value and distracts from more conducive business activities.

Reasons to get a head-start and address issues now

Even though there is no guarantee you will get audited, you are still taking a risk if you do not address potential tax credit and incentive exposures in your organization. It may seem easy to “roll the dice” and hope the issue will remain uncovered, but it could come at a cost — especially if you are planning to make some big moves, like engaging in transaction of your business (M&A), going public, or embarking on another major transaction.

During the due diligence period of these transactions, it is almost certain any uncovered tax issues will emerge. You will likely not recover the value of these credits or remain on the hook for potential liability. Even worse, the exposure of these issues reflects negatively on your accounting and control system, potentially lowering the purchase value of your organization or undermining whatever deal you had in place prior to the due diligence. Often your transaction partners will start to question your organization’s trustworthiness, and reputation … due to something that may be no fault of your own.

So, you’ve been exposed … but haven’t received an IRS audit notice

Here is the deal: you know for certain you have been exposed, but you have not been notified by the IRS yet. You probably have a lot of questions — will you get an audit notice? Have you escaped unscathed? Do you need to address the issues preemptively, just in case? It may be overwhelming to decide how to proceed once you realize the exposure.

We suggest working with a qualified CPA firm to review your tax filings. A full-service accounting firm will review your organization holistically at a minimum rate, uncover any exposures, and deliver valuable peace of mind. If the firm does find issues, you have two options:

Update your credit and incentive filings moving forward.

While this will likely decrease the amount you can deduct, it exemplifies transparency.

Issue a Voluntary Disclosure (VA) if the exposure is significant and you do not have a lot of time to fix the issue.

Essentially, you are volunteering to correct your mistakes by recalculating the credits claimed and paying back the difference.

While this may sting a little, the IRS looks favorably upon organizations who are proactive to fix the issue by filing a VA and they are likely to waive any penalties or interest you would have had to pay.

You’ve received an IRS audit notice. Now what?

Well, it happened. You received an audit note from the IRS. Before you panic, here is what you need to do:

Start preparing your documentation right away. The sooner you have your ducks in a row, the sooner you are prepared to handle the audit.

Check the contract you signed with your original provider and verify if they provide controversy support services for situations like these.

If they do, reexamine the quality of their work. Do they have any of the red flags mentioned in this article? Could something they have done have caused the audit?

Consider engaging a qualified CPA firm as your new provider to handle the subsequent controversy support. Someone you trust can get you ready for any available credits and incentives moving forward, too.

If you used a provider that displays any red flags, you could have some leverage for a reasonable cause defense. Because the “professional” firm handled it for you and made a mistake, you could utilize a first-time penalty abatement, which means you can get relief from a penalty if you:

Did not previously have to file a return or if you do not have any penalties for the three years before the tax year you received a penalty;

Filed all currently required returns or an extension of time to file; and

Paid or have arranged to pay any tax due.

Verify your contract with the original provider to determine if you have any recourse to seek compensation from them. If the IRS does issue any penalties, you will want to ensure you do not have to pay.

Standalone firms vs. full-service accounting firms

Let’s say you haven’t received an IRS notice, and you do not think you are in danger of receiving one. How can you ensure you will not in the future? It comes down to choosing a firm to help you maximize the potential of these tax credits and incentives.

The bottom line: it is imperative you work with a certified public accounting (CPA) firm instead of a standalone firm. Because standalone firms often use lower-cost, less-experienced recent graduates who are not certified public accountants, there is a distinct lack of knowledge and background in the accounting fundamentals, causing you to be misled by those unequipped to help with complex tax matters. You also run the risk of being oversold benefits by aggressive firms that not only exaggerate the amount you are receiving from the tax credits and incentives, but also behave in a way that attracts IRS attention and jeopardizes your firm.

A full-service accounting firm, on the other hand, knows how to look at an organization holistically — and it has many more capabilities and professionals with experience. It looks at things through various lenses and can advise how certain positions will impact current and future tax positions. Full-service firms also likely have an in-house controversy team that has handled hundreds of audits successfully—so you will be in good hands.

Our perspective

Tax credits and incentives provide plenty of benefits you do not want to miss out on, and their often-complex application and qualification processes are reason enough to hire a professional accountant to help you maximize your returns. Unfortunately, we often see organizations placing their trust in the wrong providers and they end up suffering the consequences of an IRS audit. For many, it is simply easier and safer to cut off the relationship with the initial provider and start fresh with a professional firm you know you can trust.

At MGO, our dedicated Tax Credits and Incentives team brings more than 30 years of experience fixing these types of issues and working with the IRS to limit the damage. We provide cleanup in the event you are being audited by the IRS (or could be audited in the future), and help you identify areas where you can claim tax credits and incentives for next time. If you are concerned, our best advice is to get ahead of it with an opinion you can trust — before the IRS decides to investigate themselves.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

Welcome to the Cannabis M&A Field Guide from MGO. In this series, our practice leaders and service providers provide guidance for navigating M&A deals in this new phase of the quickly expanding industries of cannabis, hemp, and related products and services. Reporting from the front-lines, our team members are structuring deals, implementing best practices, and magnifying synergies to protect investments and accrete value during post-deal integration. Our guidance on market realities takes into consideration sound accounting principles and financial responsibility to help operators and investors navigate the M&A process, facilitate successful transactions, and maximize value.

In the cannabis and hemp industries, capturing the true value of real estate holdings in an M&A deal can be both elusive and central to the overall success of the transaction. Difficult-to-acquire licenses and permits are essential for operating, which often drives up the “ticket price” of property, ignoring operational and market realities that suppress value in the long run. On the flip side, real estate holdings are sometimes considered “throw-ins” during a large M&A deal. These properties can hold risks and exposures, or, in many cases, are under-utilized and present an opportunity to uncover hidden value.

Both Acquirers and Target companies must take specific steps toward understanding the varied layers of risk and opportunity presented by real estate holdings. In the following, we will address some common scenarios and provide guidance on the best way to ensure fair value throughout an M&A deal.

Real estate as a starting point for enterprise value

Leaders of cannabis and hemp enterprises must understand that real estate should be a focus of the M&A process from the very beginning. All too often, c-suite executives are well-acquainted with detailed financial analyses for other parts of the business, but have a limited or out-of-date idea of their enterprise’s square footage, details of lease agreements, or comparable values in shifting real estate markets. Oftentimes it takes a major business event, like an M&A deal, to spur leadership to reexamine and understand real estate holdings and strategy. Regrettably, and all too often, principals come to that realization post-closing and realize they may have left money on the table.

In an M&A deal, the party that takes a proactive approach to real estate considerations gains an upper-hand in negotiations and calculating value. Real estate holdings can provide immediate opportunities for liquidity, cost-reduction, or revenue generation. At the same time, detailed due diligence can reveal redundant properties, costly debt obligations, unbreakable leases, and other red flags that would undermine value post-closing.

For both sides of the M&A transaction, real estate strategy and valuation should be a core consideration of the overall goals and value drivers of the deal. A direct path to this mindset is to place real estate holdings on the same level of importance as other assets that drive value – human capital, technology, intellectual property, etc. Ensuring that real estate strategy aligns with business goals and objectives will save considerable headaches and potential liabilities in the later stages of negotiating and closing the deal. Qualify and confirm all real estate data

One of the harmful side-effects of a laissez-faire attitude toward real estate in M&A is that the entire deal can be structured around data that is simply inaccurate or incomplete. This inconsistency is not necessarily the result of an overt deception, but too often it is simply an oversight. Valuations can also be based upon pride and ego, without supporting market data.

Let’s visit a very common M&A scenario: The Target company has real estate data on file from when they purchased or leased the property (which may have been years ago), and that data says headquarters is 20,000 sq. ft. of office space. Perhaps they invested heavily into improvements like custom interiors that did nothing to add value to the real estate. The Target includes that number in the valuation process and the Acquirer assumes it is accurate. Following the deal, the Acquirer moves in and, in the worst case, realizes there is actually only 15,000 sq. ft. of useable space. Or it is equally common that the Acquirer learns the space is actually 25,000 sq. ft. Either way, value has been misrepresented or underreported. M&A deals involve a multitude of figures and calculations, and sometimes things are simply missed. But those small things can have a major impact on value and performance in the long run.

The only solution to this problem is to dedicate resources to qualifying and quantifying data related to real estate holdings. When preparing to sell, Target companies should review all assumptions – square footage, usage percentage, useful life, etc. – and conduct field measurements and physical condition assessments (“PCA’s”). This will help your team understand the value of your holdings and set realistic expectations, and perhaps just as importantly, it saves you from the embarrassment of providing inaccurate numbers exposed during Acquirer’s due diligence—and getting re-traded on price and terms. That reputation will ripple through the marketplace.

From the Acquirer’s side, the details of real estate holdings should come under the same level of scrutiny as financials, control environment, etc. Your due diligence team should commission its own field measurements and PCA, and also seek out market comparables to confirm appraisals. It is simply unsafe and unwise to assume the accuracy of any of these details. Performing your own assessments could reveal a solid basis to re-negotiate the M&A, and will help shape post-merger integration planning.

Tax analysis will reveal risks and opportunities

The maze of tax regimes and regulatory requirements cannabis and hemp operators navigate naturally creates opportunities to maximize efficiencies. This is particularly the case when it comes to enterprise restructuring to navigate the tax burden of 280E.

For example, it may be possible to establish a real estate holding company that is a distinct entity from any “plant-touching” operations. By restructuring the real estate holdings and contributing those assets to this new entity it may be possible to take advantage of additional tax benefits not afforded to the group if owned directly by the “plant-touching” entity. This all assumes a fair market rent is charged between the entities.

Recently, operators have looked to sale/leaseback transactions to help with cash flow needs and thus these types of transactions have gained prominence for cannabis and hemp operators. It is important that these transactions be carefully reviewed prior to execution to ensure they can maintain their tax status as a true sale and subsequent lease, instead of being considered a deferred financing transaction. If a Target company has a sale/leaseback deal established but under audit the facts and circumstances do not hold up, this could open up major tax liabilities for the Acquirer.

When entering into an M&A transaction, it is important that the Acquirer look at the historical and future aspects of the Target’s assets, including the real estate, to maximize efficiencies of these potentially separate operations. It is also equally important to review pre-established agreements/transactions to ensure the appropriate tax classification has been made and that the appropriate facts and circumstances that gave rise to the agreements/transactions have been documented and followed to limit any potential negative exposure in the future.

Contract small print could make or break a deal

An area of particular focus during due diligence should be a review, and close read, of the Target company’s existing property leases and other contracts. There are any number of clauses and agreements that seem harmless and inconsequential on the surface, but can have disastrous effects in difficult situations. In many cases the lease/contract of a property is more important than the details of the property itself. For example, if the non-negotiable rent on a retail location is too high (and scheduled to go higher), there may be no way to ever turn a profit.

The financial distress resulting from the COVID-19 pandemic has brought these issues to the forefront in the real estate industry. Rent payment and occupancy issues are shifting the fundamental economics of many property deals and contracts. If, for example, you are acquiring a commercial location that is under-utilized because of market demand or governmental mandate, you must confirm whether sub-leases or assignments are allowed at below the contract price. If not, you could be stuck with a costly, underperforming asset amid quickly shifting commercial real estate demand.

In many leases and contracts there are Tenant Improvement Allowance conditions that require the landlord to fund certain property improvement projects. If utilizing these terms is part of the Acquirer’s plans, you may need to have frank and open conversations with landlords about whether the funds for these projects are still available, and if those contract obligations will be met. Details like these are often penned during times of financial comfort without consequences to the non-performing party, but a landlord struggling with cash flow may not have the capability to meet contract standards.

These are just a few examples from a multitude of potential real estate contract issues that can emerge. It is recommended to not only examine these contracts very closely, but have dedicated real estate industry experts perform independent assessments that account for broader social, economic, and market realities. That independent analysis will help your executive team formulate a real estate strategy that better aligns with core business objectives.

Dig deep to uncover real value

There are countless scenarios where issues related to real estate make or break an otherwise solid M&A transaction, whether before or after closing the deal. The only path forward is to treat real estate holdings with the same care and attention paid to the other asset classes driving the deal. The cannabis and hemp industries have recently endured micro-boom-and-bust cycles that have left many assets under-performing. As Target companies offload these assets, and Acquirers seek out good deals, both parties must undertake focused efforts to establish the fair value of complex real estate assets and obligations.

Often viewed as a “public company problem,” private organizations may want to consider implementing internal controls similar to Sarbanes-Oxley (SOX) Section 404 requirements. The inherent benefits of a strong control environment may be of significant value to a private company by providing: enhanced accountability throughout the organization, reduced risk of fraud, improved processes and financial reporting, and more effective inclusion of the Board of Directors.

Private organizations, while not always smaller, often have limited resources in specialty areas, including accounting for income tax. This resource constraint —the work being done outside the core accounting team — combined with the complexity of the issues, means private companies are ideal candidates for, and can achieve significant benefit from, internal controls enhancements. Thinking beyond the present, the following are five reasons private companies may want to adopt public-company-level controls:

1. Future Initial Public Offering (IPO) – Walk before you run! If the company believes an IPO may be in its future, it’s better to “practice” before the company is required to be SOX compliant. A phased approach to implementation can drive important changes in company culture as it prepares to become a public organization. Recently published reports analyzing IPO activity reveal that material weaknesses reported by public companies were disproportionately attributable to recent IPO companies. Making a rapid change to SOX compliance can place a heavy burden on a newly public company.

2. Merger and Acquisition Deals – If the possibility of the company being sold to an M&A deal exists, enhanced financial reporting controls can provide the potential buyer with an added layer of security or comfort regarding the financial position of the company. Further, if the acquiring firm has an exit strategy that involves an IPO, the requirement for strong internal controls may be on the horizon.

3. Rapid Growth – Private companies that are growing rapidly, either organically or through acquisition, are susceptible to errors and fraud. The sophistication of these organizations often outpaces the skills and capacity of their support functions, including accounting, finance, and tax. Standard processes with preventive and detective controls can mitigate the risk that comes with rapid growth.

4. Assurance for Private Investors and Banks – Many users other than public shareholders may rely on financial information. The added security and accountability of having controls in place is a benefit to these users, as the enhanced credibility may impact the cost of borrowing for the organization.

5. Peer-Focused Industries – While not all industries are peer-focused, some place significant weight on the leading practices of their peers. Further, some industries require enhanced levels of security and control. For example, cannabis companies with a heavy regulatory burden, industries with sensitive customer data like lifesciences, and tech companies that handle customer data, often look to their peer group for leading practices, including their control environment. When the peer group is a mix of public and private companies, the private company can benefit from keeping pace with the leading practices of their public peers.

Private companies are not immune from the intense scrutiny of numerous stakeholders over accountability and risk. Companies with a clear understanding of the inherent risks that come from negligible accounting practices demonstrate their ability to think beyond the present, and to be better prepared for future growth or change in ownership.

Welcome to the Cannabis M&A Field Guide from MGO. In this series, our practice leaders and service providers provide guidance for navigating M&A deals in this new phase of the quickly expanding industries of cannabis, hemp, and related products and services. Reporting from the front-lines, our team members are structuring deals, implementing best practices, and magnifying synergies to protect investments and accrete value during post-deal integration. Our guidance on market realities takes into consideration sound accounting principles and financial responsibility to help operators and investors navigate the M&A process, facilitate successful transactions, and maximize value.

Deal structure can be viewed as the “Terms and Conditions” of an M&A deal. It lays out the rights and obligations of both parties, and provides a roadmap for completing the deal successfully. While deal structures are necessarily complex, they typically fall within three overall strategies, each with distinct advantages and disadvantages: Merger, Asset Acquisition and Stock Purchase. In the following we will address these options, and common alternatives within each category, and provide guidance on their effectiveness in the cannabis and hemp markets.

Key considerations of an M&A structure

Before we get to the actual M&A structure options, it is worth addressing a couple essential factors that play a role in the value of an M&A deal for both sides. Each transaction structure has a unique relationship to these factors and may be advantageous or disadvantageous to both parties.

Transfer of Liabilities: Any company in the legally complex and highly-regulated cannabis and hemp industries bears a certain number of liabilities. When a company is acquired in a stock deal or is merged with, in most cases, the resulting entity takes on those liabilities. The one exception being asset deals, where a buyer purchases all or select assets instead of the equity of the target. In asset deals, liabilities are not required to be transferred.

Shareholder/Third-Party Consent: A layer of complexity for all transaction structures is presented by the need to get consent from related parties. Some degree of shareholder consent is a requirement for mergers and stock/share purchase agreements, and depending on the Target company, getting consent may be smooth, or so difficult it derails negotiations.

Beyond that initial line of consent, deals are likely to require “third party” consent from the Target company’s existing contract holders – which can include suppliers, landlords, employee unions, etc. This is a particularly important consideration in deals where a “change of control” occurs. When the Target company is dissolved as part of the transaction process, the Acquirer is typically required to re-negotiate or enter into new contracts with third parties. Non-tangible assets, including intellectual property, trademarks and patents, and operating licenses, present a further layer of complexity where the Acquirer is often required to have the ownership of those assets formally transferred to the new entity.

Tax Impact: The structure of a deal will ultimately determine which aspects are taxed and which are tax-free. For example, asset acquisitions and stock/share purchases have tax consequences for both the Acquirer and Target companies. However, some merger types can be structured so that at least a part of the sale proceeds can be tax-deferred.

As this can have a significant impact on the ROI of any deal, a deep dive into tax implications (and liabilities) is a must. In the following, we will address the tax implications of each structure in broad strokes, but for more detail please see our article on M&A Tax Implications (COMING SOON).

Asset acquisitions

In this structure, the Acquirer identifies specific or all assets held by the Target company, which can include equipment, real estate, leases, inventory, equipment and patents, and pays an agreed-upon value, in cash and/or stock, for those assets. The Target company may continue operation after the deal. This is one of the most common transaction structures, as the Acquirer can identify the specific assets that match their business plan and avoid burdensome or undesirable aspects of the Target company. From the Target company’s perspective, they can offload under-performing/non-core assets or streamline operations, and either continue operating, pivot, or unwind their company. For the cannabis industry, asset sales are often preferred as many companies are still working out their operational specifics and the exchange of assets can be mutually beneficial.

Advantages/Disadvantages

Transfer of Liabilities: One of the strongest advantages of an asset deal structure is that the process of negotiating the assets for sale will include discussion of related liabilities. In many cases, the Acquirer can avoid taking on certain liabilities, depending on the types of assets discussed. This gives the Acquirer an added line of defense for protecting itself against inherited liabilities.

Shareholder/Third-Party Consent: Asset acquisitions are unique among the M&A transaction structures in that they do not necessarily require a stockholder majority agreement to conduct the deal.

However, because the entire Target company entity is not transferred in the deal, consent of third-parties can be a major roadblock. Unfortunately, as stated in our M&A Strategy article, many cannabis markets licenses are inextricably linked to the organization/ownership group that applied for and received the license. This means that acquiring an asset, for example a cultivation facility, does not necessarily mean the license to operate the facility can be included in the deal, and would likely require re-application or negotiation with regulatory authorities.

Tax Impact: A major consideration is the potential tax implications of an asset deal. Both the Acquirer and Target company will face immediate tax consequences following the deal. The Acquirer has a slight advantage in that a “step-up” in basis typically occurs, allowing the acquirer to depreciate the assets following the deal. Whereas the Target company is liable for the corporate tax of the sale and will also pay taxes on dividends from the sale.

Stock/share purchase

In some ways, a stock/share purchase is a more efficient version of a merger. In this structure, the acquiring company simply purchases the ownership shares of the Target business. The companies do not necessarily merge and the Target company retains its name, structure, operations and business contracts. The Target business simply has a new ownership group.

Advantages/Disadvantages

Transfer of Liabilities: Since the entirety of the company comes under new ownership, all related liabilities are also transferred.

Shareholder/Third Party Consent: To complete a stock deal, the Acquirer needs shareholder approval, which is not problematic in many circumstances. But if the deal is for 100% of a company and/or the Target company has a plenitude of minority shareholders, getting shareholder approval can be difficult, and in some cases, make a deal impossible.

Because assets and contracts remain in the name of the Target company, third party consent is typically not required unless the relevant contracts contain specific prohibitions against assignment when there is a change of control.

Tax Impact: The primary concern for this deal is the unequal tax burdens for the Acquirer vs the Shareholders of the Target company. This structure is ideal for Target company shareholders because it avoids the double taxation that typically occurs with asset sales. Whereas Acquirers face several potentially unfavorable tax outcomes. Firstly, the Target company’s assets do not get adjusted to fair market value, and instead, continue with their historical tax basis. This denies the Acquirer any benefits from depreciation or amortization of the assets (although admittedly not as important in the cannabis industry due to 280E). Additionally, the Acquirer inherits any tax liabilities and uncertain tax positions from the Target company, raising the risk profile of the transaction.

Three types of mergers

1: Direct merger

In the most straight-forward option, the Acquiring company simply acquires the entirety of the target company, including all assets and liabilities. Target company shareholders are either bought out of their shares with cash, promissory notes, or given compensatory shares of the Acquiring company. The Target company is then considered dissolved upon completion of the deal.

2: Forward indirect merger

Also known as a forward triangular merger, the Acquiring company merges the Target company into a subsidiary of the Acquirer. The Target company is dissolved upon completion of the deal.

3: Reverse indirect merger

The third merger option is called the reverse triangular merger. In this deal the Acquirer uses a wholly-owned subsidiary to merge with the Target company. In this instance, the Target company is the surviving entity.

This is one of the most common merger types because not only is the Acquirer protected from certain liabilities due to the use of the subsidiary, but the Target company’s assets and contracts are preserved. In the cannabis industry, this is particularly advantageous because Acquirers can avoid a lot of red tape when entering a new market by simply taking up the licenses and business deals of the Target company.

Advantages/Disadvantages

Transfer of Liabilities: In option #1, the acquirer assumes all liabilities from the Target company. Options #2 and #3, provide some protection as the use of the subsidiary helps shield the Acquirer from certain liabilities.

Shareholder/Third Party Consent: Mergers can be performed without 100% shareholder approval. Typically, the Acquirer and Target company leadership will determine a mutually acceptable stockholder approval threshold.

Options #1 and #2, where the Target company is ultimately dissolved, will require re-negotiation of certain contracts and licenses. Whereas in option #3, as long as the Target company remains in operation, the contracts and licenses will likely remain intact, barring any “change of control” conditions.

Tax Impact: Ultimately, the tax implications of the merger options are complex and depend on whether cash or shares are used. Some mergers and reorganizations can be structured so that at least a part of the sale proceeds, in the form of acquirer’s stock, can receive tax-deferred treatment.

In conclusion

Each deal structure comes with its own tax advantages (or disadvantages), business continuity implications, and legal requirements. All of these factors must be considered and balanced during the negotiating process.