Key Takeaways:

- The CHIPS Act provides more than $50 billion to boost U.S. semiconductor manufacturing, including current funding opportunities for commercial fabrication facilities and advanced packaging research and development (R&D).

- The Advanced Manufacturing Tax Credit (Section 48D) offers a 25% credit for qualified investments into semiconductor manufacturing facilities placed in service from 2023-2026.

- Companies seeking CHIPS incentives or 48D credit should understand eligibility requirements, review application process details, and connect with specialized tax credits and incentives professionals to ensure maximum benefit.

~

On August 9, 2022, President Joe Biden signed into law the Creating Helpful Incentives to Produce Semiconductors Act of 2022 (commonly referred to as the CHIPS Act). The legislation provides $52.7 billion to increase semiconductor research and development in the United States. The CHIPS Act also established the Advanced Manufacturing Tax Credit (Section 48D), available to entities that manufacture semiconductors.

Recently, the government awarded its first major CHIPS Act grant – providing $1.5 billion to GlobalFoundries, one of the world’s leading semiconductor manufacturers, to expand its semiconductor production in New York and Vermont. That grant is expected to be the first of several announcements in the coming months as the government ramps up CHIPS Act funding.

What Is the Purpose of the CHIPS Act?

The intent of CHIPS is simple: the U.S. wants to incentivize domestic companies to manufacture semiconductors. The president called the CHIPS Act a “once-in-a-generation investment in America itself,” as the legislation aims to lower costs and create jobs in the production of these advanced chips.

The COVID-19 pandemic forced the semiconductor industry to operate at a reduced capacity, while lockdowns increased demand for products using semiconductors (computers, tablets, gaming systems, cars, etc.). This created a perfect storm, fueling a shortage of semiconductors. As a result, the U.S. recognized the need to increase its semiconductor output.

However, manufacturing semiconductors is not cheap and requires substantial investments. CHIPS, along with the available tax credit, encourages these investments.

The CHIPS Act includes provisions for:

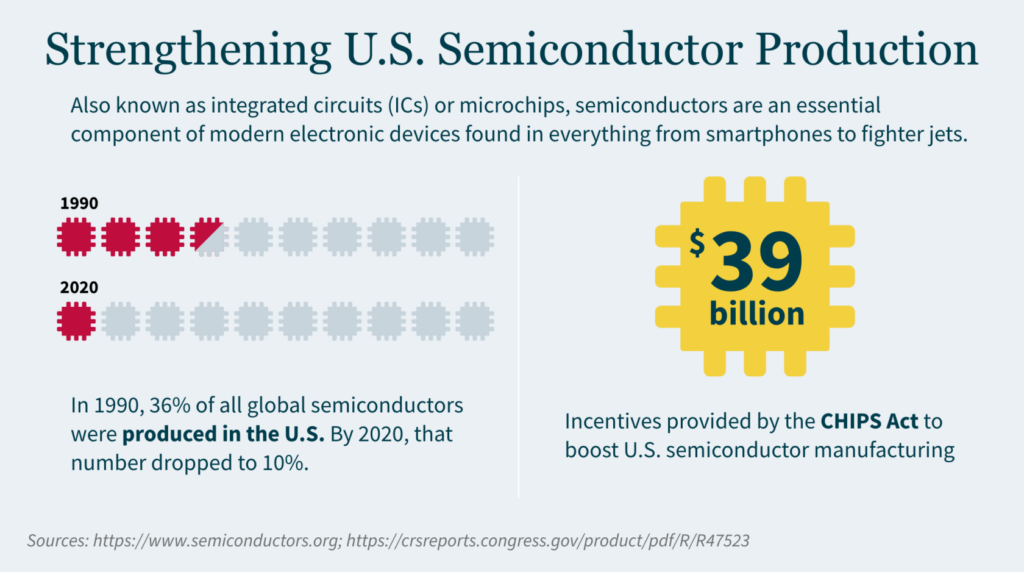

- $39 billion in incentives to build, expand, or modernize domestic facilities and equipment for semiconductor manufacturing, assembly, testing, advanced packaging, or research and development

- $13.2 billion in R&D and workforce development

- $500 million for international information communications technology security and semiconductor supply chain activities

Understanding the Advanced Manufacturing Tax Credit

With the addition of Section 48D to the Internal Revenue Code, CHIPS offers a new tax credit if your company invests in advanced manufacturing facilities or facilities whose primary purpose is manufacturing semiconductors or semiconductor manufacturing equipment.

Eligible businesses can receive a 25% tax credit of “qualified investments”. You can elect to treat the credit as payment against tax (i.e., direct pay) if you do not have sufficient tax liability to utilize the credit, making this essentially a refundable tax credit.

Eligibility Criteria for 48D

To be eligible for 48D, you must have made a qualified investment for any taxable year integral to an “advanced manufacturing facility” for semiconductors placed in service during that year. Qualified properties must be:

- Buildings, structural components, or parts of a building (not including administrative services or other functions unrelated to manufacturing)

- Crucial to the operation of the advanced manufacturing facility

- Constructed or built by the taxpayer

- Qualified for amortization or depreciation

Taxpayers that use facilities and equipment outside the U.S. will not be eligible (similar to other investment credit requirements). Other taxpayers ineligible for the credit include:

- Foreign entities noted as “foreign entities of concern” (i.e., foreign terrorist organizations or organizations included on the Office of Foreign Assets Control list).

- Taxpayers that have engaged in significant transactions involving the material expansion of semiconductor manufacturing capacity in China or another foreign country of concern.

- If a taxpayer enters a transaction in a foreign country of concern within 10 years of claiming the credit, it will be recaptured.

48D Timing

The tax credit applies to any property placed in service after December 31, 2022, for which construction begins before January 1, 2027. It does not apply after December 31, 2026, nor can you use the tax credit for constructing a property after this date. If construction on a facility began before January 1, 2023, the credit applies only to the portion of the construction started after August 9, 2022.

Application Process

In March 2023, the IRS issued proposed regulations addressing direct payment of Section 48D credit. The proposed regulations also require taxpayers to register through an IRS electronic portal before treating Section 48D as a direct payment on a tax return.

The IRS will issue a registration number for each qualified investment for which your company is claiming a credit, and that number must be included on your tax return.

CHIPS Incentive Opportunities

To access CHIPS incentives, your company must first apply for open funding opportunities. To date, the U.S. Department of Commerce has issued three Notice of Funding Opportunities (NOFOs) through the CHIPS for America program:

- Commercial Fabrication Facilities – Currently accepting applicants

- Small-Scale Supplier Projects – No longer accepting applicants, in second phase of process

- National Advanced Packaging Manufacturing Program (NAPMP) Materials & Substrates – Just announced on February 28, 2024

How to Apply for Open NOFOs

Application forms and instructions are available on the CHIPS Incentives Program application portal. FAQs, guides, and templates can also be found in the “Resources” section of the portal.

The application process includes the following stages:

- Statement of interest

- Pre-application (optional, but recommended)

- Full application

- Due diligence

- Award preparation and issuance

Statement of interest – To submit a statement of interest, applicants need to register for an account on the CHIPS Incentives Portal. A statement of interest must be submitted at least 21 days prior to submitting a pre-application or full application.

Pre-application – The optional pre-application provides an opportunity to ensure your projects are consistent with program requirements. During this stage, you will receive feedback on strengths and weaknesses of your proposal and recommendations for improvement.

Full application – Both pre-applications and full applications are accepted on a rolling basis.

Due diligence – Your application will undergo review to ensure alignment with evaluation criteria specified in the Notice of Funding Opportunity (NOFO), with the possibility of requests for additional information.

Award preparation and issuance – Before receiving an award, you must have an active registration in the System for Award Management (SAM). It’s a good idea to begin the registration process for SAM.gov early as it may take anywhere from two weeks to six months (due to information verification requirements).

Maximizing Your Semiconductor Manufacturing Tax Credits and Incentives

Navigating CHIPS’s nuances can be challenging – especially when claiming the available tax credit and determining how it is refundable. Furthermore, companies seeking to increase their semiconductor manufacturing capacity in the U.S. should also assess application and opportunity for federal and state R&D tax credits and incentives.

With more than 30 years of experience, our dedicated Tax Credits and Incentives team can help you maximize your credit benefits, develop the appropriate documentation methodology, assist in calculating and claiming credits, and defend your claims. Our full-service firm, led by experienced CPAs and a