Key Takeaways:

- Thorough documentation is essential for maximizing R&D tax credit claims by linking innovative projects to the required criteria set by authorities.

- Critical documentation methods include maintaining project plans, reports, communications, time sheets, expense logs, and categorizing all records by project with clear dates.

- To substantiate experimentation, continuously update digital records like lab notes and version-controlled documents to detail hypotheses, trials, iterations, findings, and modifications.

~

For companies in industries like manufacturing, biotech and life sciences, and technology, navigating the complex world of research and development (R&D) tax credits can be challenging. Thorough documentation is the key to maximizing your claim. Effective R&D tax credit claims hinge on robust documentation. Establishing the link between your innovative projects and the tax credit criteria set by authorities is non-negotiable.

Maximizing R&D Tax Credits: A Checklist for Robust Documentation

From ideation to execution, every step of your R&D project must be documented with precision. Follow these guidelines to assist your efforts:

1. Foundation and Focus of Documentation

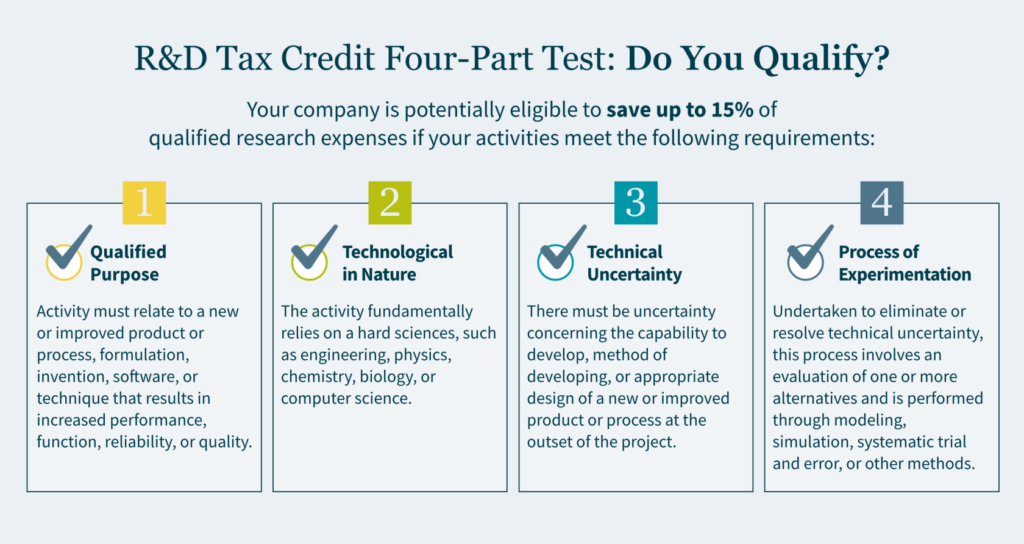

Lay the foundation for your R&D tax credit claim by aligning your innovative endeavors with the IRS’s qualifications. It is critical to consistently document every aspect of your projects, from initial goals and research stages to the hurdles you overcome and the novel outcomes you achieve. Your documentation needs to center on and address how your activities relate to the required four-part test: developing a business component, relying on science or technology, aiming to eliminate uncertainty, and involving a process of experimentation.

2. Documentation Methods and Best Practices

Incorporate a variety of records into your R&D documentation system — such as project plans, reports, and communications. For optimal organization, make sure each document is clear, concise, and bears a date stamp. Then categorize all documents by project, which aids in retrieval and review. Keep detailed records of project developments, discussions, and decisions to facilitate a straightforward audit process.

3. Tracking and Proving Your R&D Work

Maintain a log of your qualifying R&D activities and concurrent developments, clearly articulating how these relate to expenses. Accurate and up-to-date records like time sheets and expense logs are essential. Organize and categorize all R&D costs — from personnel and materials to outsourcing and cloud computing — employing accounting software for uniform expense coding. This methodical record-keeping is essential for connecting R&D endeavors with their associated costs, ensuring this support is available and complete in the event of an IRS audit.

4. Showcasing Experimentation

Substantiate technological progress with thorough records of your experimental activities. Continuously update digital records to reflect the evolving nature of your R&D projects, capturing each hypothesis, trial, and iteration. Make certain these digital records, like lab notes and version-controlled documents, comprehensively detail the experiments, findings, and any modifications to procedures or products.

Unlock R&D Tax Credits to Drive Your Business Forward

Navigating the intricacies of R&D tax credits is a continuous process that demands thorough documentation and strategic planning. By adhering to the four guidelines above and meeting the four-part test, businesses can not only ensure compliance but also maximize their potential benefits. As you embark on this journey, remember each detail documented is a step towards fostering innovation and technological advancement within your company.

MGO offers a comprehensive suite of strategic financial services to support your R&D endeavors. Reach out to us today to find out how we can help you.